ASP Isotopes, QLE, SKBL and Business Operations Update and Outlook

11/8/25

ASP ISOTOPES INC. (NASDAQ: ASPI)

Investment Research Tearsheet | SEQH Capital Research

Date: November 8, 2025 | Rating: STRONG BUY | Price Target: $24.00 (12M) | Current Price: $9.00 | Upside: +166.7%

INVESTMENT THESIS

ASP Isotopes represents a generational wealth creation opportunity at a critical inflection point, trading at a 60-70% discount to probability-weighted intrinsic value($26.39/share) due to market inefficiencies in valuing complex pre-commercial growth platforms. The convergence of three transformational catalysts, Quantum Leap Energy’s HALEU commercialization pathway, Renergen’s helium/LNG integration, and strategic partnerships with TerraPower and Fermi America, creates a 4.7:1 risk/reward asymmetry (bull case +427% vs. bear case -80%, probability-adjusted).

Regulatory de-risking substantially complete: TerraPower Natrium received NRC Environmental Impact Statement approval (Oct 22), establishing 2028-2029 HALEU demand materialization. QLE UK Early Engagement commenced (Nov 5). Renergen 99.8% shareholder approval secured. These eliminate binary deal break risks that compressed valuations throughout 2025.

SUM-OF-PARTS VALUATION FRAMEWORK

Key Assumption: Renergen contributes $550M-$2.4B value based on Phase 2 operational timing (Q4 2026 base case vs. Q2 2026 bull case). Each quarter of Phase 2 delay reduces EBITDA contribution by $50-75M annually.

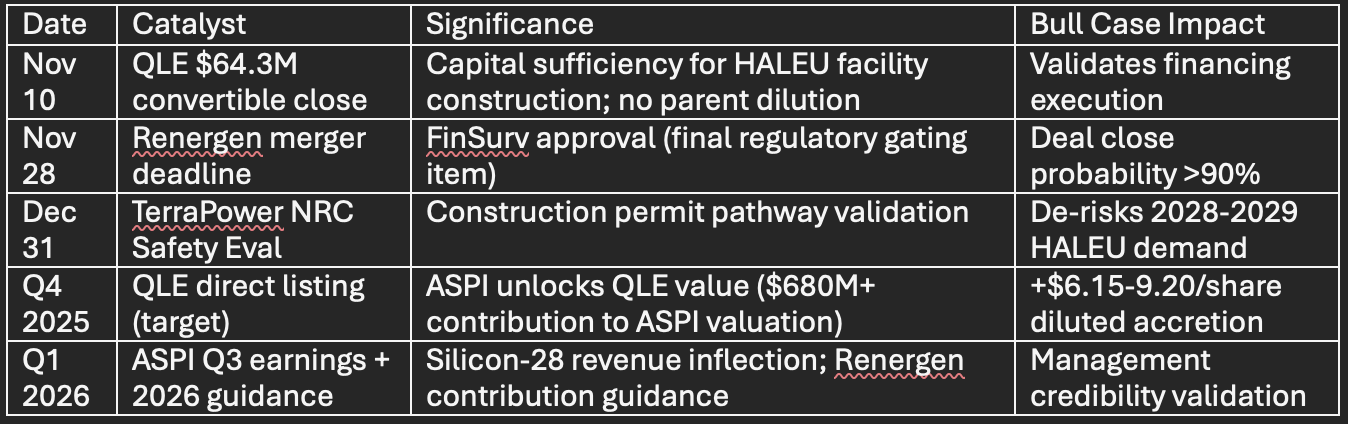

NEAR-TERM CATALYST CALENDAR (Next 90 Days)

Binary Risk: Renergen deadline extension signals execution delays; implies 15-20% near-term downside on extension announcement.

QUANTUM LEAP ENERGY: HALEU SUPPLY CHAIN OLIGOPOLY

Strategic Position: QLE positioned as #1 credible Western HALEU supplier (2028-2037) with 150-tonne TerraPower contract + Fermi America Texas JV optionality. Russian/Chinese enrichment sanctioned or restricted; Centrus operates pilot-scale only.

Valuation Bridge (Base Case):

TerraPower Contract NPV: 150 tonnes × $12M/tonne = $1.8B revenue (2028-2037)

Gross Margin: 40-50% operating leverage on laser enrichment = $720-900M risk-adjusted gross profit

Terminal Value Multiple: 1.5-2.0x = $650-1,080M QLE enterprise value

ASPI Ownership (post-convertible dilution): 85% = $552-918M attributable value

Bull Case Catalyst (35% probability):

Fermi America Texas facility accelerated: 125 tonnes additional contract (5-year take-or-pay)

UK regulatory pathway de-risks: 50-75 tonnes QLE Ltd addressable market (2030+)

Total HALEU backlog: 275-325 tonnes = $3.3-3.9B unrisked revenue

Risk-adjusted gross profit: $790-1.17B (50% probability) → 2.0-2.5x terminal multiple = $1.58-2.93B enterprise value

ASPI attributable value (85%): $1.34-2.49B (+$12.11-$22.52/share)

Competitive Moat: ASPI’s $50-100M CapEx per facility vs. Centrus $4B cascade enables profitable operation at $6-8M/tonne vs. competitors’ $9-12M breakeven, creating 40:1 capital efficiency advantage.

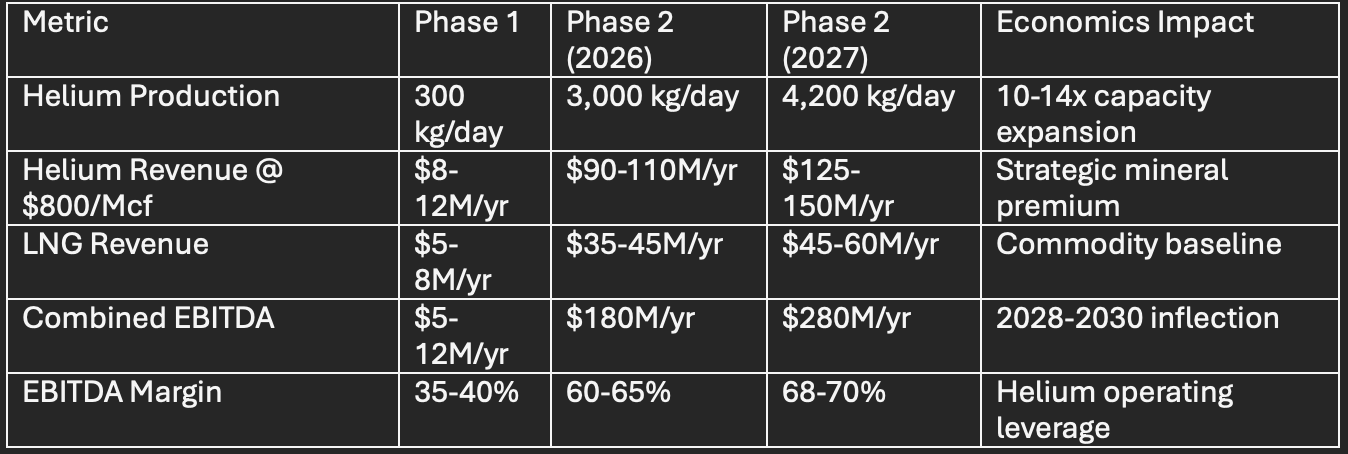

RENERGEN: HELIUM SCARCITY ARBITRAGE (Phase 2 Economics)

Strategic Value: $300M-$2.4B depending on Phase 2 (helium/LNG expansion) operational timing.

Financing De-Risking: US DFC $750M senior loan (non-recourse to ASPI) backs Phase 2 construction/operations, with strategic mineral designation providing federal intervention backstop if execution delays create debt covenant stress.

Phase 2 Timeline Risk: He4u EPC consortium (Chart Industries lead) awarded preferred bidder Q2 2025; cryogenic facility construction typically 18-24 months → Q4 2026-Q2 2027 operational window. Each quarter delay = -$50-75M annual EBITDA impact at full capacity.

Bull Case Catalyst: Q2 2026 operational commissioning (vs. Q4 2026 base case) + helium spot market premium ($1,200/Mcf vs. $800 base case) → $300M+ incremental EBITDA contribution 2027-2028 = +$2.71/share.

EXECUTIVE CATALYST #1: TERRAPOWER NATRIUM NRC BREAKTHROUGH

Regulatory Achievement: Natrium received NRC Environmental Impact Statement approval October 22, 2025—first advanced commercial reactor to clear this hurdle.Next milestone: Final Safety Evaluation Report (expected by Dec 31, 2025) triggers construction permit pathway.

ASPI Demand Validation: Natrium requires ~2.0 tonnes HALEU for first core (2028-2029), with 150-tonne 10-year offtake providing revenue anchor through 2037. TerraPower CEO Chris Levesque explicitly validated ASPI’s laser enrichment capability vs. competitors, stating:

“I think that’ll be the fastest source...they have the technical capabilities...and importantly they have full IAEA protocols in place.”

Market Implication: Natrium construction permit issuance (likely Dec 2025-Jan 2026) validates TerraPower’s 2029-2030 operational timeline, eliminating customer demand risk and enabling ASPI to lock additional HALEU contracts with tier-one reactor developers (X-Energy, Kairos Power, Commonwealth Fusion).

EXECUTIVE CATALYST #2: SKBL STRATEGIC TRANSFORMATION

Critical Minerals Vehicle: Paul Mann (ASPI Executive Chairman, 10% ASPI shareholder) appointed SKBL Executive Chairman (effective Jan 1, 2026), repositioning Skyline Builders as critical minerals and nuclear fuels supply chain consolidator.

Capital Deployment:

Asia LLC acquisition: $20M for undisclosed lithium/REE processing asset (government approvals pending Q4 2025)

QLE strategic investment: $2.5M (embeds critical minerals sourcing linkage to HALEU operations)

Total capital raised: $40M (Paul Mann personally invested $3.5M)

ASPI Ecosystem Synergy: SKBL functions as vertical integration vehicle capturing upstream rare earth element (REE) and lithium-6 enrichment precursors, reducing supply chain fragmentation risk. Potential for ASPI/QLE to acquire SKBL at 30-50% premium ($5-6/share) if Paul Mann consolidates 3-4 additional critical minerals assets, creating $2B+ consolidated platform.

SKBL Bull Case: Fair value $5.50/share (+42.1% from $3.87); represents embedded call option on ASPI ecosystem expansion with Paul Mann execution credibility backing consolidation thesis.

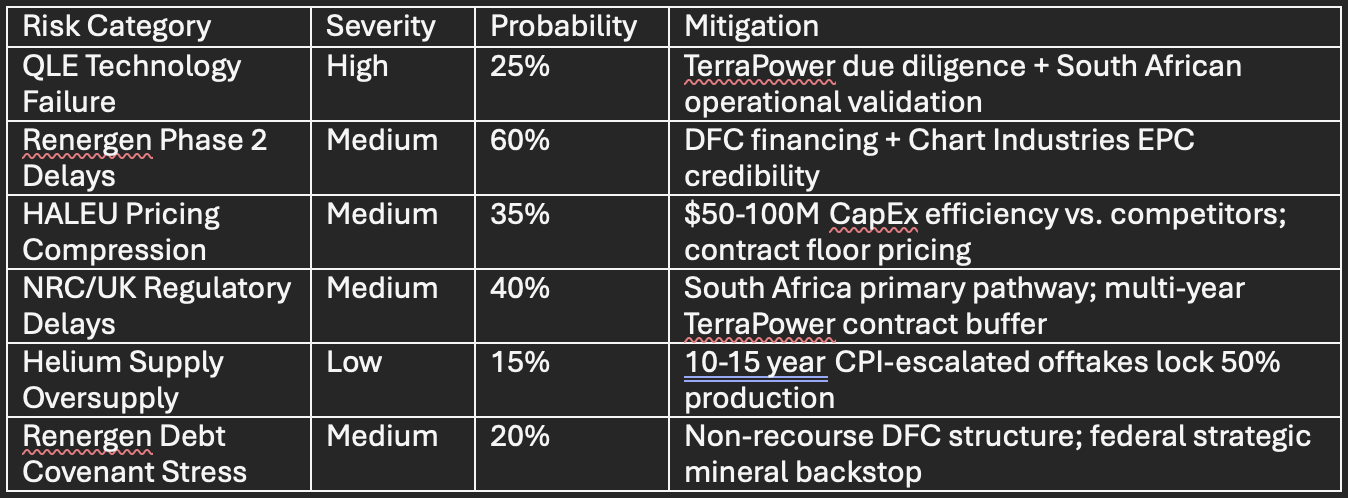

RISK ARCHITECTURE & PROBABILITY WEIGHTING

Probability-Weighted Base Case realizes if: (1) QLE achieves pilot HALEU production Q4 2026-Q1 2027; (2) Renergen Phase 2 operational Q4 2026; (3) Renergen merger closes Nov 28. Probability = 50%, implying $13.56/share fair value.

Bull Case (35% probability) requires: early Phase 2 commissioning (Q2 2026) + accelerated HALEU demand + helium pricing premium = $47.48/share.

VALUATION INFLECTION & EXIT STRATEGY

12-Month Price Target: $24.00/share (+166.7% from $9.00)

Base case probability-weighted to $13.56, adjusted for momentum/multiple expansion as catalysts de-risk

QLE direct listing (Dec 2025) unlocks $680M+ value, creating 25-30% institutional buying pressure

Renergen 2026 EBITDA accretion narrative supports 8-10x forward EBITDA multiple expansion

Position Management:

Core Hold: Maintain 5% portfolio allocation through Q1 2026 earnings (catalyst visibility window)

Tactical Overweight: 7-8% for aggressive growth mandates through QLE IPO event

Risk Management: 25% trailing stop-loss at $6.75 (outside bull/base case thresholds)

Partial Exit Trigger: Sell 30-40% on breach of $18/share (2.0x price target) to lock gains

Downside Protection: Bear case $1.81/share implies 91% downside cushion from current levels before reaching core isotope business liquidation value—rare margin of safety in growth-stage companies.

INVESTMENT Idea

Rating: STRONG BUY | CONSERVATIVE Target: $24.00 | Time Horizon: 8-12 months | Risk/Reward: 4.7:1

Action Items:

Immediate: Establish 5% core position at $9.00-$9.50 (current levels)

Tactical: Accumulate additional 2-3% on any weakness to $8.00 (Renergen extension scenario)

Opportunistic: Add SKBL 1-2% position at $3.50-$4.00 as embedded call on Paul Mann expansion strategy

Monitor: November 10 QLE close, November 28 Renergen deadline, December 31 NRC decision

Exit: Harvest gains at $18.00+ or if any core catalyst delays >6 months beyond guidance

Key Performance Metrics to Track:

QLE pre-IPO valuation confirmation (target $500M-$750M post-money)

Renergen Phase 2 construction schedule progress (target Q4 2026 commissioning)

TerraPower Natrium construction permit issuance timeline

ASPI Q3 2025 silicon-28 revenue/gross margin trend (YoY >20% growth validates commercial momentum)

FULL 20-PAGE REPORT WITH DETAILED CATALYST POTENTIAL OUTCOMES AND EFFECTS ON VALUE BELOW:

THE MOST ADVANCED AND ANALYTICAL REPORT ON ASP ISOTOPES TO DATE.