ASP Isotopes Quantitative Analysis and Outlook

October 21, 2025

ASP Isotopes Inc. (ASPI) - Quantitative Investment Tear-Sheet

NASDAQ: ASPI | Report Date: October 21, 2025

Executive Summary & Investment Thesis

ASP Isotopes Inc. represents a transformative opportunity at the intersection of advanced materials, nuclear energy, quantum computing, and precision medicine. The company has successfully transitioned from R&D to commercial-stage production, with three enrichment facilities fully operational in South Africa and first commercial shipments of Ytterbium-176 (Yb-176) and Silicon-28 (Si-28) already underway. Management’s proprietary Aerodynamic Separation Process (ASP) technology has been validated through operational outperformance, including Si-28 production capacity exceeding guidance by 60% (now >80kg annually, 8x original expectations) and Yb-176 enrichment factors of 52 (target: >50).

The investment case is anchored by: (1) near-term revenue inflection with $50-70M projected from just two isotopes by 2026-27; (2) strategic vertical integration via the Renergen acquisition, unlocking helium/LNG revenue and up to 96% cost reduction in isotope enrichment; (3) partnerships with tier-1 industry leaders (NECSA, TerraPower, Fermi America) validating technology and securing demand for advanced nuclear fuel (HALEU); and (4) management’s credible roadmap to $300M+ EBITDA by 2030. Recent capital raise of $210.3M extends runway and funds aggressive expansion, including four new laser enrichment plants starting construction in Q1 2026.

Recommendation: STRONG BUY

Price Targets & Valuation Framework

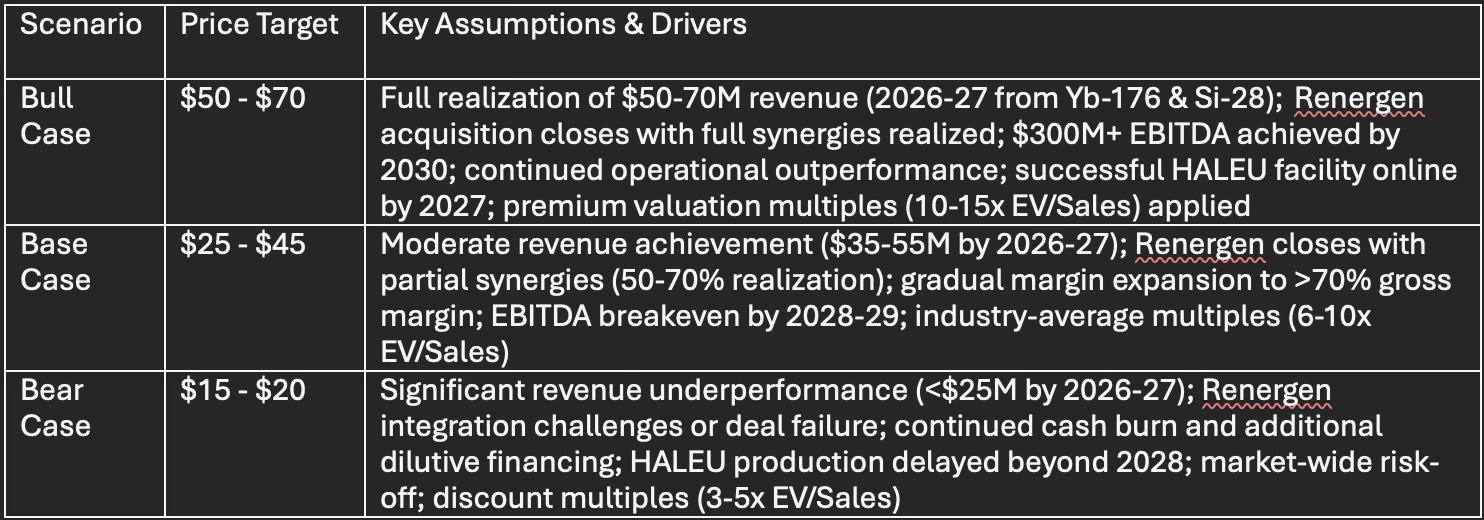

12-Month Price Target Summary

Valuation Methodologies

1. Discounted Cash Flow (DCF) Analysis

Bull Case DCF: Projects rapid revenue ramp with 63.9% CAGR through 2027, margin expansion to >70% gross margins by 2028, and terminal EBITDA of $300M+ by 2030. Discount rate: 8-10% (reflecting reduced execution risk post-commercialization). Terminal growth rate: 3-4% (reflecting long-term positioning in high-growth isotope markets). Bull Case NPV supports $50-70/share valuation.

Base Case DCF: Moderate revenue growth (40-50% CAGR), gross margins reach 60-65% by 2029, EBITDA positive by 2029. Discount rate: 10-12% (reflecting scaling and integration risks). Terminal growth: 2-3%. Supports $25-45/share.

Bear Case DCF: Conservative revenue growth (15-25% CAGR), margins remain compressed (<50%), negative EBITDA through 2028. Discount rate: 12-15% (elevated execution and financing risk). Terminal growth: 1-2%. Downside to $15-20/share.

2. Comparable Company Analysis

Peer group includes advanced materials, specialty chemicals, and nuclear fuel cycle companies. While no direct comparables exist (ASPI’s product portfolio and ASP technology are unique), premium multiples are justified by sole-source positioning in several isotope markets, strategic importance to national security (HALEU, advanced nuclear), and participation in exponential growth markets (quantum computing, targeted alpha therapy).

Bull Case Multiples: 10-15x forward EV/Sales, 25-35x forward EV/EBITDA (2027-28E)

Base Case Multiples: 6-10x forward EV/Sales, 18-25x forward EV/EBITDA

Bear Case Multiples: 3-5x forward EV/Sales

3. Risk-Adjusted Net Present Value (rNPV)

Probability-weighted NPV of key product launches and M&A synergies. Bull Case assigns 70-80% probability of success to Yb-176/Si-28 ramps, 60-70% to Renergen synergies, 50-60% to HALEU production by 2027.

Financial Metrics, Projections & Profitability Path

Current Financial Position (TTM)

Revenue: $4.58M (pre-commercial; transformative growth imminent)

Operating Margin: -799.9% (typical for pre-revenue development stage)

Free Cash Flow Yield: -10.3%

Recent Capital Raise: $210.3M (extends runway through commercial ramp and plant construction)

Debt: Moderate levels; balance sheet strengthened post-raise but requires monitoring as company scales

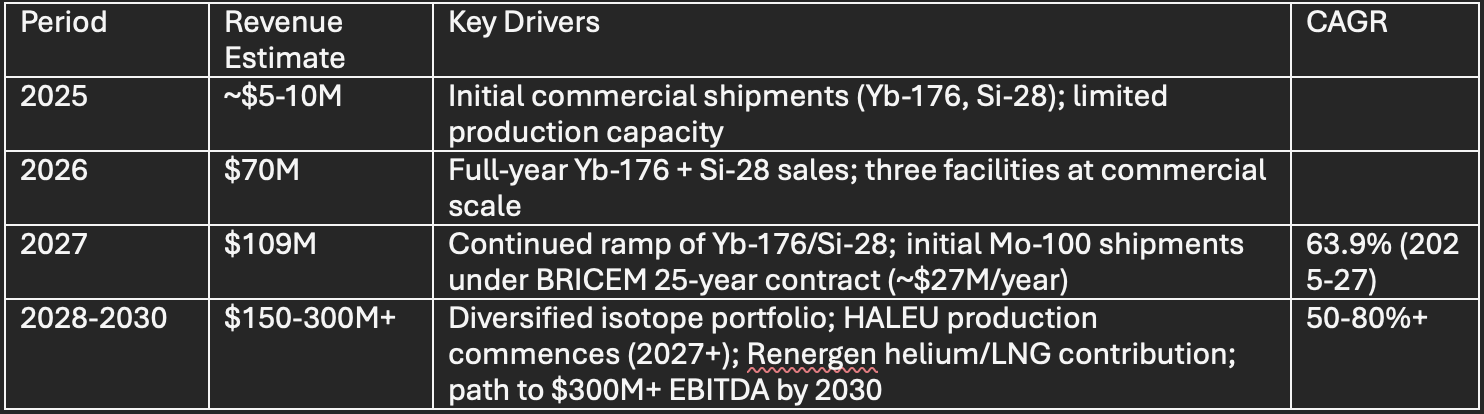

Revenue Projections & Growth Trajectory

Revenue by Product Line (2026-27 Estimates):

Ytterbium-176: $25-35M - Targeted alpha therapy (radiopharmaceuticals); existing customer orders and partnerships with pharma companies

Silicon-28: $25-35M - Quantum computing (qubit fabrication), advanced semiconductors; >80kg annual capacity

Molybdenum-100: $27M+/year - 25-year supply agreement with BRICEM (for Technetium-99m medical isotope production); highly stable, contracted revenue stream

HALEU (2027+): TBD - Advanced nuclear reactors (TerraPower, Fermi America MOU for 11 GW nuclear data centers); potentially transformative revenue contribution

Profitability & Margin Expansion Roadmap

Target Gross Margins: >70% for high-value isotopes (Yb-176, Si-28, Mo-100) - reflects specialized nature, low marginal cost of ASP technology, and high barriers to entry

Cost Structure Transformation: Renergen acquisition integrates low-cost helium supply (Virginia gas field), reducing ASPI’s isotope enrichment operating costs by up to 96%, a powerful competitive moat

EBITDA Trajectory:

2025-26: Negative EBITDA (investment phase, facility ramp)

2027-28: EBITDA positive (as revenue scales and fixed costs are absorbed)

2030: $300M+ EBITDA target (management guidance) - driven by diversified high-margin isotope portfolio, Renergen synergies, and HALEU production at scale

Products, Markets & Commercial Strategy

Core Product Portfolio

1. Ytterbium-176 (Yb-176) - Targeted Alpha Therapy (Cancer Treatment)

Application: Precursor for Lutetium-177, used in precision radiopharmaceuticals for prostate cancer, neuroendocrine tumors

Market Opportunity: Global radiopharmaceuticals market growing at 10-12% CAGR; Yb-176 is supply-constrained with limited global producers

Production Status: Commercial shipments commenced; enrichment factor of 52 achieved (exceeding target of >50)

Revenue Potential: $25-35M annually (2026-27)

2. Silicon-28 (Si-28) - Quantum Computing & Semiconductors

Application: Ultra-pure Si-28 enables longer qubit coherence times (quantum computers), high-performance semiconductors

Market Opportunity: Quantum computing market projected to reach $65B+ by 2030; Si-28 is critical enabler for silicon spin qubits

Production Status: Facility operational at >80kg/year capacity (60% above initial guidance, 8x original expectations); strong customer demand

Revenue Potential: $25-35M annually (2026-27)

3. Molybdenum-100 (Mo-100) - Medical Isotope Production

Application: Feedstock for Technetium-99m (Tc-99m), the most widely used medical isotope globally (80% of nuclear medicine procedures)

Market Opportunity: Global Tc-99m market valued at $3.5B+; Mo-100 is a strategic bottleneck in supply chain

Production Status: 25-year supply agreement with BRICEM; production ramp expected 2026-27

Revenue Potential: ~$27M+/year (contracted, high-visibility revenue)

4. High-Assay Low-Enriched Uranium (HALEU) - Advanced Nuclear Reactors

Application: Fuel for next-generation small modular reactors (SMRs) and advanced reactors (TerraPower Natrium, X-energy Xe-100, others)

Market Opportunity: U.S. and global advanced nuclear buildout; HALEU is supply-constrained with limited domestic (U.S./allied) production capacity

Production Status: Partnerships with NECSA (South Africa), TerraPower (Bill Gates-backed), Fermi America (MOU for 11 GW nuclear data center capacity); target first production by 2027

Revenue Potential: Potentially transformative; multi-decade revenue opportunity tied to advanced nuclear deployment

Strategic Importance: National security priority (U.S. seeks to reduce reliance on Russian HALEU); ASPI positioned as key Western supplier

5. Future Pipeline: Molybdenum-98, Zinc-67/68, Nickel-64, Xenon-129/136, Lithium-7, Chlorine-37, Germanium-70/72/74 - diversified revenue streams across nuclear medicine, energy, semiconductors, and specialty applications

Strategic Initiatives & Catalysts

Renergen Acquisition - Vertical Integration & Cost Leadership

Strategic Rationale: Renergen owns the Virginia gas field (South Africa) with helium and LNG reserves. Helium is critical input for ASPI’s cryogenic isotope enrichment processes

Financial Impact: Expected to be highly accretive to EBITDA starting 2026; adds helium and LNG revenue streams (diversification); combined entity targets $300M+ EBITDA by 2030

Cost Synergies: Integration of low-cost helium supply reduces ASPI’s isotope enrichment costs by up to 96% - transformative margin expansion and competitive moat

Timeline: Deal completion expected 2025-26 (subject to regulatory approval)

Expansion: Four New Laser Enrichment Plants

Scope: Construction of four additional laser-based enrichment facilities to expand capacity across isotope portfolio

Timeline: Procurement underway; construction start Q1 2026; phased commissioning 2026-28

Technology: Next-generation Quantum Enrichment (QE) technology expected in future plants (higher efficiency, lower cost vs. current ASP)

Capacity Impact: Significant expansion of Yb-176, Si-28, Mo-100, and other isotope production; supports multi-hundred-million revenue target by 2030

JSE Dual Listing - Capital Markets Strategy

Rationale: Listing on Johannesburg Stock Exchange (JSE) provides access to South African capital markets, enhances liquidity, and diversifies shareholder base

Benefits: Improved capital formation capabilities; de-risks reliance on U.S. markets; aligns with South African operational base and Renergen integration

Industry Partnerships - Validation & Demand Visibility

1. NECSA (South African Nuclear Energy Corporation)

Significance: Government-backed nuclear agency; partnership validates ASPI technology and provides regulatory/operational support for HALEU production

Timeline: Ongoing collaboration; critical to 2027 HALEU production target

2. TerraPower (Bill Gates-backed Advanced Nuclear)

Significance: TerraPower is developing next-gen Natrium reactors requiring HALEU; partnership positions ASPI as potential primary fuel supplier

Market Opportunity: TerraPower has multiple reactor projects in development; multi-decade HALEU demand

3. Fermi America — Nuclear Data Centers

Significance: MOU for HALEU supply to HyperGrid Campus (11 GW nuclear generation capacity, 6 GW for AI infrastructure)

Market Opportunity: Convergence of AI compute demand and clean baseload power; nuclear data centers represent massive new HALEU demand vector

Timeline: Early-stage discussions; reflects long-term secular tailwind for ASPI’s HALEU ambitions

Investment Catalysts & Timeline

Near-Term Catalysts (2025-2026)

Q4 2025 / Q1 2026: Renergen acquisition completion and integration plan announcement

Q1 2026: Four new laser plant construction commencement; updated production capacity guidance

2026: First full year of commercial revenue from Yb-176 and Si-28; analyst estimates of $70M revenue

2026: Initial Mo-100 shipments under BRICEM contract; ~$27M/year contracted revenue stream begins

Medium-Term Catalysts (2027-2028)

2027: Revenue target of $109M (analyst consensus); continued Yb-176/Si-28 ramp + Mo-100 contribution

2027: HALEU first production - major strategic milestone; partnerships with TerraPower and Fermi America validated

2027-28: New laser enrichment plants commissioned; significant capacity expansion across isotope portfolio

2028: EBITDA positive (expected); margin expansion driven by scale and Renergen cost synergies

Long-Term Catalysts (2029-2030+)

2030: $300M+ EBITDA target - driven by diversified isotope revenue, HALEU at scale, Renergen synergies, and >70% gross margins

2030+: Potential M&A activity (ASPI as acquirer or acquisition target); ongoing advanced nuclear buildout sustains HALEU demand

Key Risks & Mitigants

Execution & Operational Risks

Risk: Scaling proprietary ASP technology; meeting production targets; plant commissioning delays

Mitigant: Demonstrated operational success (Si-28 capacity 60% above guidance, Yb-176 enrichment factor exceeds target); experienced management team; $210M capital raise provides financial cushion

Financing & Dilution Risk

Risk: High cash burn; potential need for additional capital raises (dilution to existing shareholders)

Mitigant: Recent $210M raise extends runway; revenue inflection in 2026-27 reduces reliance on external financing; Renergen acquisition adds cash-generative assets (helium/LNG)

Integration Risk (Renergen)

Risk: M&A integration challenges; failure to realize projected 96% cost synergies; deal closure delays or failure

Mitigant: Management has articulated clear integration plan; Renergen assets are cash-flow positive (helium/LNG); synergies are structural (helium supply for cryogenic processes)

Regulatory & Geopolitical Risk

Risk: Nuclear material export controls; U.S./South African regulatory approvals for HALEU production; geopolitical instability in South Africa

Mitigant: Partnerships with government-backed entities (NECSA); South Africa has established nuclear industry and regulatory framework; HALEU is strategic priority for Western governments (supportive policy environment)

Market & Competition Risk

Risk: Emerging competitors in isotope production; demand shortfalls in quantum computing or radiopharmaceuticals; volatility in nuclear sector sentiment

Mitigant: ASPI’s proprietary ASP technology provides cost and efficiency advantages (barriers to entry); diversified product portfolio reduces single-market risk; long-term contracted revenue (Mo-100, HALEU partnerships) provides visibility

Stock-Specific Risk

Risk: High short interest; elevated price volatility; relatively low float and liquidity

Mitigant: Operational execution and revenue delivery will de-risk investment thesis and drive short covering; JSE dual listing improves liquidity

Conclusion & Investment Rationale

ASP Isotopes represents a high-conviction, high-reward opportunity for investors seeking exposure to critical materials, advanced nuclear energy, quantum computing, and precision medicine. The company’s transition to commercial-stage production, validated by operational outperformance and first shipments, de-risks the investment case and establishes a clear path to substantial revenue generation. The $50-70M revenue target by 2026-27 from just two isotopes, combined with the $300M+ EBITDA goal by 2030, reflects management’s credible and ambitious growth roadmap.

The Renergen acquisition is a strategic masterstroke, delivering vertical integration, diversification (helium/LNG revenue), and up to 96% cost reduction in isotope enrichment-creating a durable competitive moat. Partnerships with tier-1 players (NECSA, TerraPower, Fermi America) validate ASPI’s technology and position the company as a critical supplier in the advanced nuclear fuel cycle (HALEU), a multi-decade secular growth opportunity tied to global decarbonization and energy security.

While execution risks remain (scaling production, M&A integration, regulatory approvals), the company’s demonstrated operational excellence, strong balance sheet post-$210M raise, and diversified product portfolio mitigate downside and support an asymmetric risk/reward profile.

Recommendation: STRONG BUY | Bull Case Price Target: $50-70 | Base Case: $25-45

FULL 19-PAGE QUANTITATIVE REPORT BELOW: