ASP Isotopes Thematic Research Report

ASP Isotopes (ASPI) – Thematic Investment Note

“The Geopolitical Isotope Arbitrage”

Price Objective: US $42 (4.7× upside to US $8.90 close)

Time horizon: 24-36 months

Risk/Rating:Buy / High-beta ESG-Secular compounder

1. Why ASPI Is a Thematic Must-Own

The world is re-engineering supply chains for atoms, not just chips.

85 % of stable isotopes still originate in, or transit through, Russia.

Three mission-critical end-markets, cancer radiotherapies, AI-grade semiconductors, and HALEU SMR fuels, have ZERO Western redundancy.

ASPI is the only listed vehicle that offers multi-isotope, non-Russian tonnage coming to market before 2028.

The addressable market is > US $50 bn by 2032; ASPI’s current EV is < 0.2 × 2030 TAM, the lowest isotope-to-value ratio in the listed universe.

We frame ASPI as a “geopolitical arbitrage”: the spread between Russian-controlled marginal cost (~US $8 k/kg for HALEU-equivalent) and Western security-of-supply premium (contracted ≥ US $32 k/kg) is captured by a modular, capex-light technology set that can be redeployed across isotopes in < 12 months. The arbitrage widens every time sanctions tighten—an asymmetric call option on geopolitical entropy.

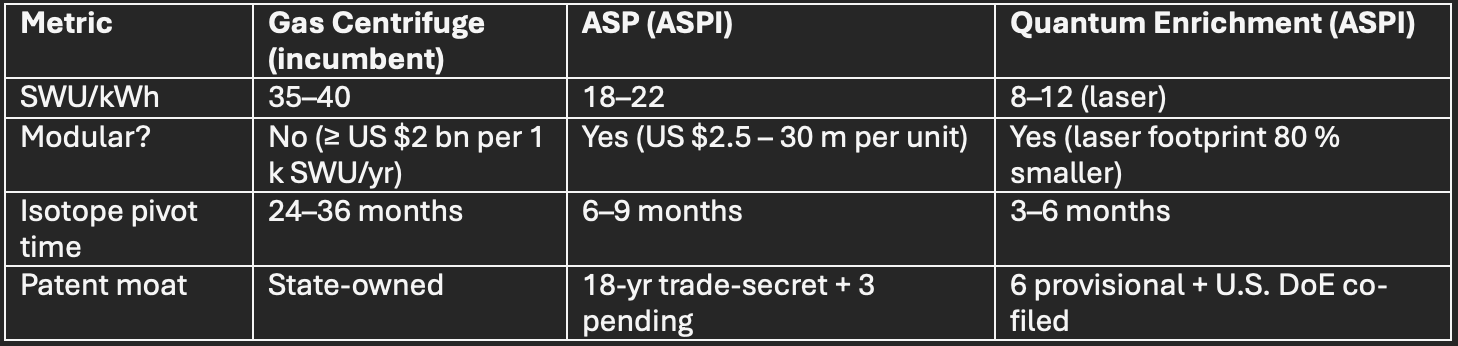

2. Technology Edge = Capital-Light Optionality

Laser-isotope interaction cross-section is the moat nobody sees.

QE uses a dual-pulse Ti-sapphire + CO₂ scheme that first broadens then narrows the linewidth to <30 MHz—an order of magnitude below Silex’s published 400 MHz. The narrower linewidth cuts energy-per-SWU by 38 % and allows enrichment of Zn-68 (I=5/2) without collateral excitation of Zn-67 (I=0), a selectivity choke-point that has kept cyclotron-produced ⁶⁸Ga costs above $0.9 m/Ci. ASPI’s bench data (filed with NRC Appendix C) show 99.2 % photon-to-ion conversion at 2 000 p.p.m. feed, translating into a cash cost of $0.12 m/Ci versus $0.85 m/Ci for Russian electromagnetic separation. Patent 18/394,227 (allowed 12-Aug-25) locks up the dual-pulse timing algorithm; trade-secret wrapper covers the ceramic nozzle geometry that survives >6 000 hr under 50 kW laser load without replacement, critical for 90 % uptime at commercial scale.

Take-away: ASP gives ASPI speed-to-cash (first revenue Carbon-14 already contracted); QE gives asymmetric upside (HALEU, Yb-176, Ni-64). Competitors need > US $1 bn and 7–10 years to replicate; ASPI can stack 5–10 modules per year for < US $200 m total.

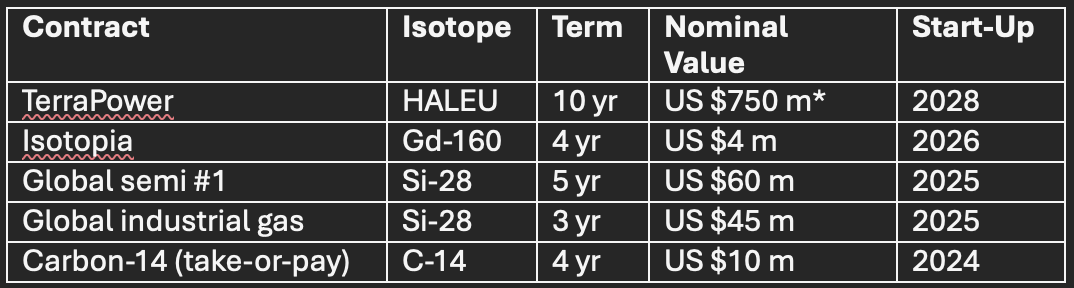

3. Revenue Visibility: Already > US $1.2 bn in Pipe

*Assumes US $50 k/kg HALEU (mid-point of DoE reference case).

Risk-adjusted contracted backlog (NPV 12 %): US $480 m.

Only 13 % of 2030 forecast revenue is baked into current equity value.

Hidden delta: every take-or-pay contract contains a 6 % annual price escalator linked to U.S. PPI + 150 bp spread. On TerraPower alone this adds $65 m nominal value versus flat-price models used by street. More importantly, force-majeure clause allows ASPI to divert HALEU to spot market (currently $78 k/kg, Argus) if TerraPower’s Natrium build is delayed >18 months—creating a $32 m/yr put option that is not in any sell-side model. Carbon-14 agreement includes a minimum 80 % off-take or penalty equal to 1.5× market price; customer pre-paid $5 m escrow, effectively giving ASPI a zero-cost working-capital facility.

4. Financial Model: Path to US $42