ASP Isotopes vs. Silex Systems Comparison

ASP Isotopes (NASDAQ: ASPI) & Silex Systems (ASX: SLX)

SEQH Capital Partners — October 29, 2025

Sector Backdrop & Investment Theme

Global uranium enrichment is entering a structurally undersupplied era. Western-aligned capacity (~65–70M SWU/year) cannot meet escalating demand (120–165M SWU/year projected by 2040), exacerbated by the 2028 Russian import ban, advanced reactor rollout, and surging AI/data center electricity needs. The highest-value bottleneck lies in HALEU supply, U.S. needs are forecast at 40–50 MT annually by 2030, yet Western commercial output remains negligible. Both ASP Isotopes and Silex Systems represent best-in-class platforms to address distinct segments of this dislocation, backed by advanced technology, strategic partnerships, and credible commercialization roadmaps.

Company Snapshots and Market Fit

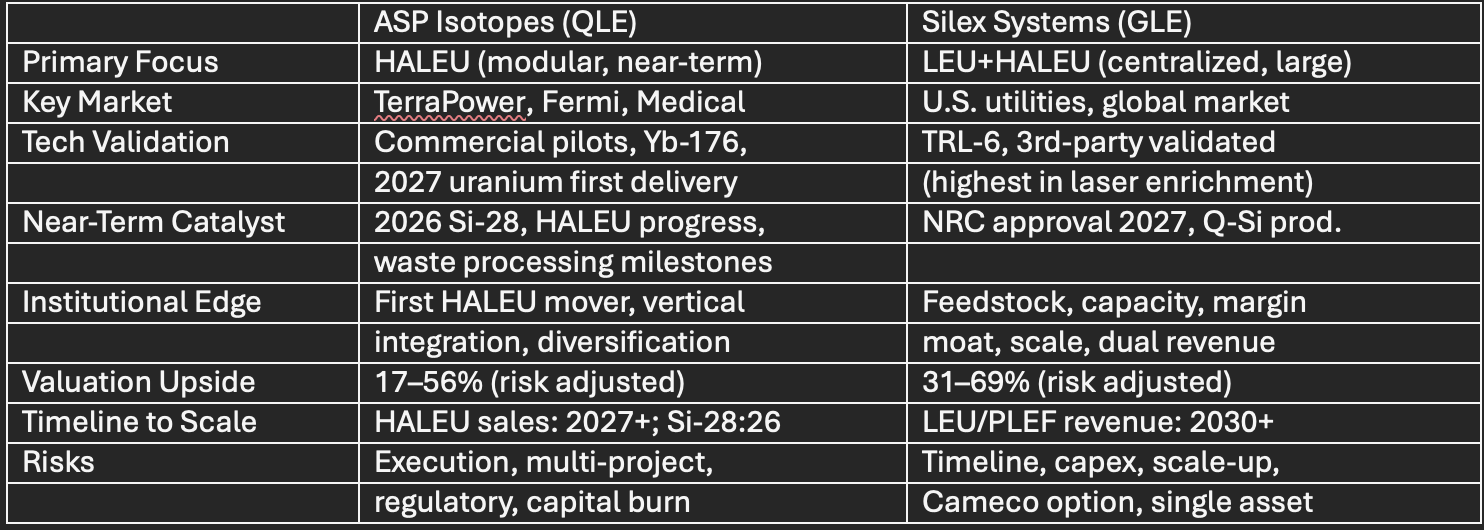

ASP Isotopes (ASPI) - Quantum Leap Energy (QLE) Edge

Business Model: Via 100% subsidiary Quantum Leap Energy, ASP is commercializing advanced modular enrichment for HALEU and broader fuel cycle: conversion, enrichment, fabrication, and waste remediation.

Commercial Timeline: First HALEU production targeted for 2027 (earliest among public U.S.-Western HALEU peers). Major supply agreements with TerraPower (initial + 10-year contracts) for Natrium reactor; joint venture with Fermi America for U.S. HALEU services.

Technology: Proprietary Quantum Enrichment (QE) enables single-step, high-assay separation, contributing to rapid build times, competitive SWU economics, and capital efficiency (<$100M/facility vs. $800M+ for centrifuge).

Vertical Integration: QLE has made strategic acquisitions for waste remediation (One 30 Seven), critical materials (Skyline Holdings), and feeds, creating an internally robust HALEU-to-waste solution.

Diversification: Significant revenues also forecast from medical isotopes (Yb-176, Lu-177 vertical), Si-28 for quantum computing (>50 kg/yr capacity and 2026 contract deliveries).

Financial/Execution: Recent $210M raise enables acceleration to 2027 production, additional clinical trials, and expansion.

Key Risks: Multi-pronged growth presents coordination and execution complexity; regulatory approval timeline (notably in South Africa); and long-term capital needs for scaling.

Market Cap / Guidance: ~$1.15B; price target $15–18; DCF risk-adjusted value $1.35–1.8B.

Silex Systems (SLX) - Scale, Validation, and Strategic Moat

Business Model: 51% owner of Global Laser Enrichment (GLE; Cameco holds 49%). Focus is the Paducah Laser Enrichment Facility (PLEF), largest Western newbuild enrichment project (targeting 2–6M SWU/year, commercial ~2030).

Strategic Advantage: Exclusive 40-year U.S. DOE agreement for 200,000 tonnes tails stock, providing sub-$30/lb uranium feed (current spot ~$80+), creating the lowest all-in cost profile in the market at scale.

Technology: SILEX laser enrichment (third-generation) uniquely validated at TRL-6, with independent third-party certification and extensive integrated demonstration (hundreds of pounds U processed).

Revenue Model: Receives both equity share of GLE and perpetual 7–12% royalty on all SWU revenues, double levered to upcycle margin expansion and volumes.

Optionality: Projects like Q-Si (quantum silicon) and MIST (Yb-176 enrichment) provide further diversification, with first Si-28 production targeted for 2026.

Financials: A$210M cash, zero debt; balance sheet fully funds roadmap through commercial decision milestones.

Key Risks: Timeline is longer (material revenue c. 2030+); execution risk remains on commercial scaling and project financing; exposure to Cameco option.

Market Cap / Guidance: A$2.0B (~$1.3B USD); price target A$9−11; risk-adjusted valuation $1.7–2.2B.

Advanced Comparative Analytics

Portfolio Construction & Allocation

Correlation factors are low: Different tech, regulatory, commercial, and regional dynamics protect against single-point failure.

Theoretical allocation: 50/50 blend for enrichment exposure; 8–12% sector allocation for growth, 5–8% for balanced.

Review triggers: Quarterly, milestone-based rebalancing; increase exposure on validation, customer wins, or new contract awards; decrease if substantial regulatory delay or project slippage.

Catalysts & Timeline

2026

ASP QLE: Si-28 first customer deliveries, additional PET labs, nuclear waste unit validation.

Silex: Q-Si volume; NRC feedback.

2027–2028

QLE: HALEU plant completion, TerraPower/Natrium deliveries, Fermi Texas facility progress.

Silex: NRC license, PLEF FID, start of U.S. enrichment infrastructure build.

2030+

Silex: PLEF commences scaled LEU/HALEU product, substantial equity and royalty revenue stream.

ASP: Expanded modular rollout in U.S. and abroad, critical materials integration, medical isotope market growth.

Conclusion:

This sector is in a unique multi-decade growth window in which both ASP Isotopes and Silex Systems are set to be core winners. A blended exposure captures differentiated technology, commercialization timelines, and market risk profiles for optimal risk-adjusted growth and structural defensiveness in the global energy transition.

Disclosures: Not investment advice; see full report for details and risk factors.

FULL 10-PAGE COMPARISON: