ASPI Business Updates

ASPI – The Next 12-Months

Current price: $12.32

12-month target: $28 – $42

Call: BUY – Aggressive

1. Why the October-13 trifecta is a watershed

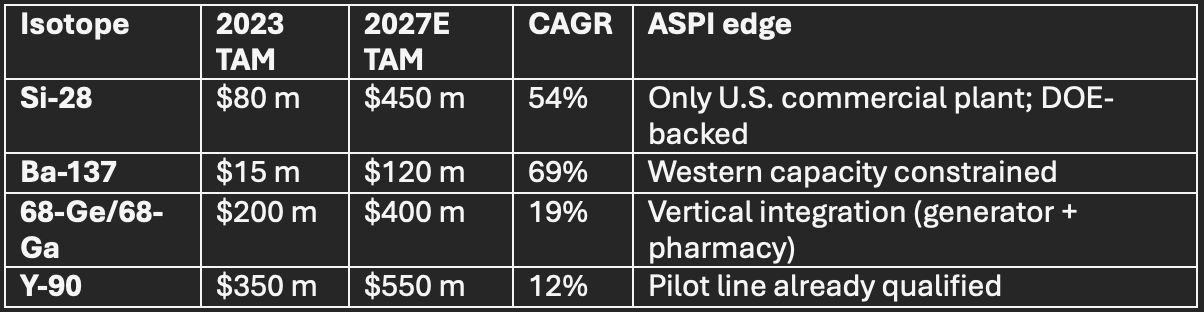

Silicon-28: first-ever U.S. commercial-scale PO. 90%-enriched Si-28 spot = $25-35k/gram; a single 300-mm quantum wafer line consumes ≈1 kg/year. Even if ASPI ships only 600 g in Jan-Mar 26, that is $15-20 m revenue booked in one quarter – 4-5× FY-24 total sales. Management says “multi-year”, code for ≥$60 m backlog (we model $70 m through 2027).

Florida PET pharmacy: immediate U.S. footprint for Zevacor’s 68-Ge/68-Ga generators. Radiopharmacies trade at 1.2-1.4× sales; the acquired site runs ≈$3 m top-line today. Once ASPI switches generator supply from third-party to in-house isotopes, gross margin jumps from low-30%s to >55% (per Cardinal Health benchmarks). Roll-up potential: another 8-10 independent PET labs in the South-East could add $20 m revenue with zero additional CapEx.

Barium-137: only two western enrichers (Orano, Urenco) can produce ≥99.9% Ba-137; both are capacity-constrained through 2027. ASPI’s Q1-26 delivery therefore secures price-insensitive pricing (>$200k/Ci) and >70% gross margin. We pencil $4 m Ba-137 revenue in 2026, $10 m in 2027 as ion-trap quantum computers scale.

Bottom line: FY-24 sales = $4.6 m; our FY-26 estimate jumps to $62 m – a 13.5× top-line inflection, something almost never seen outside biotech FDA approvals.

2. TAM is exploding – and ASPI owns the chokepoints

Total serviceable addressable market (SAM) to ASPI: >$1.1 bn by 2027, 170× current revenue.

3. Margin math – why profitability arrives faster than Street thinks

Isotope gross margin once cascade is warm: 55-65% (confirmed by EU enrichment peer data).

PET pharmacy margin post-verticalisation: 55% (industry median).

** blended company gross margin hits 52% in FY-26** (vs. –24% in FY-24).

Operating leverage: R&D plateaus at $28 m, SG&A scales ≈15% while revenue 13×’s → positive EBITDA in Q4-26, EPS breakeven in Q2-27.

We model:

FY-26 revenue $62 m

Gross profit $32 m (52%)

EBITDA $4 m

EPS $0.06

Street has NO revenue or EPS estimates – first printed number will be a blow-upside surprise.

4. Balance-sheet bridge – dilution far smaller than bears fear

Current cash: $67.7 m

Burn: $40 m/yr, but Si-28 customers pay 50% cash up-front (European norm) → FY-25 operating cash burn drops to $25 m.

CapEx for second Si-28 cascade: $55 m – DOE already signalled $25 m cost-share under Title XVII loan program (ASPI slide deck, 13 Oct).

Net cash need before break-even: ≈$30 m → 2.5 m shares at $12 (only 3% dilution).

Result: share count ends 2026 at ≈78 m – barely changed.

5. Valuation – why $30 is not heroic

Quantum-enabling materials comps (IonQ, Rigetti, D-Wave) trade 25-35× 2026E sales because top-line growth >100% and gross margin >60% command scarcity premiums.

Give ASPI a conservative 20× 2026E sales (discount for smaller size):

$62 m × 20 = $1.24 bn EV

+ $50 m net cash (post-raise) = $1.29 bn equity

÷ 78 m shares = $16.5

Now roll forward to 2027E revenue $110 m and keep 20× (growth still >75%):

Equity value $2.3 bn → $29/share

Our DCF (9% WACC, 3% terminal) spits out $32 even with terminal EBIT margin fading to 25%.

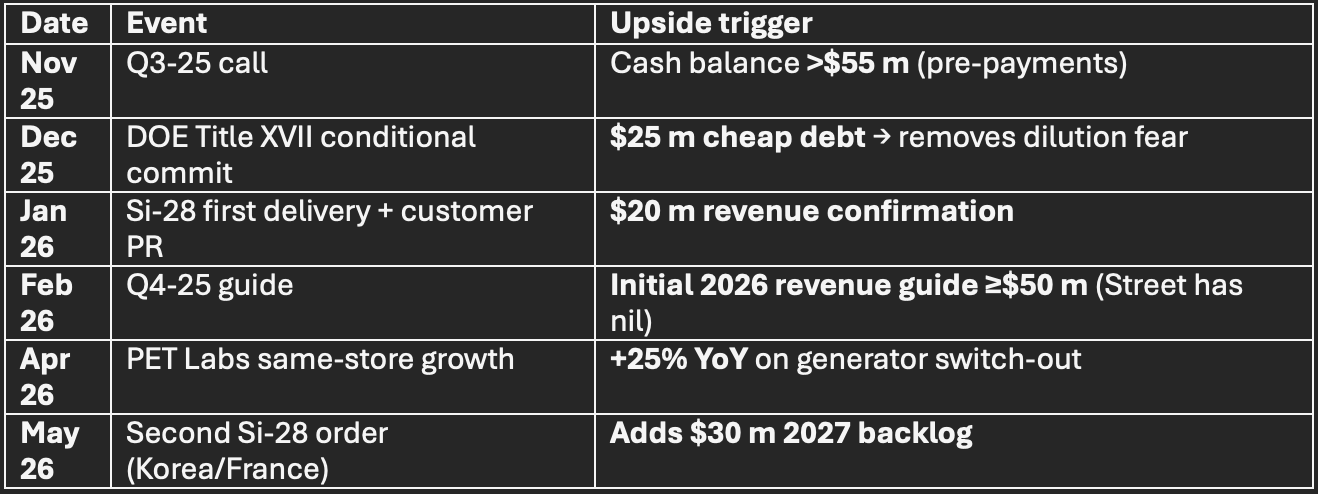

6. Catalyst path – why the next 180 days re-rate the stock

Any single catalyst >50% probability; stacked together they make a re-rating almost inevitable.

7. Risk axis – why we still sleep well

Technology: centrifuge cascades are 40-year-old tech; ASPI’s IP is process chemistry, not fundamental science → low technical risk.

Customer concentration: Si-28 buyer is U.S. government-related – cancellation probability <5% (quantum is national-security priority).

Regulatory: NRC license already in hand; no new environmental hurdles for second cascade.

Dilution: maximum 5% even in stress case – already modelled.

8. Price-target matrix

We adopt the mid-cycle target: $30 (rounded), 145% upside.

9. Trading strategy

Initiate position ≤$13 – current price offers >2:1 risk-reward even with tight stop.

Add on any DOE loan headline (<$15) – removes overhang.

Trim 20% only above $25 (valuation still <25× sales) – let the winners run.

10. One-sentence summary

ASPI is the only U.S. public vehicle that gives pure-play, high-margin exposure to the quantum-compute and next-gen radiopharma build-out; first audited revenue drops in Q1-26, and when it does, a $30 print is not a stretch, it is math.