(ASPI) Quantum Leap Energy Acquisition of One30Seven

ASP Isotopes One30Seven Acquisition: Investment Tear Sheet

SEQH Capital Partners Research | October 23, 2025

Transaction Overview

Acquirer: Quantum Leap Energy LLC (QLE), wholly-owned subsidiary of ASP Isotopes Inc. (NASDAQ: ASPI)

Target: One30Seven Inc. (Canadian nuclear waste technology developer)

Transaction Date: October 21, 2025

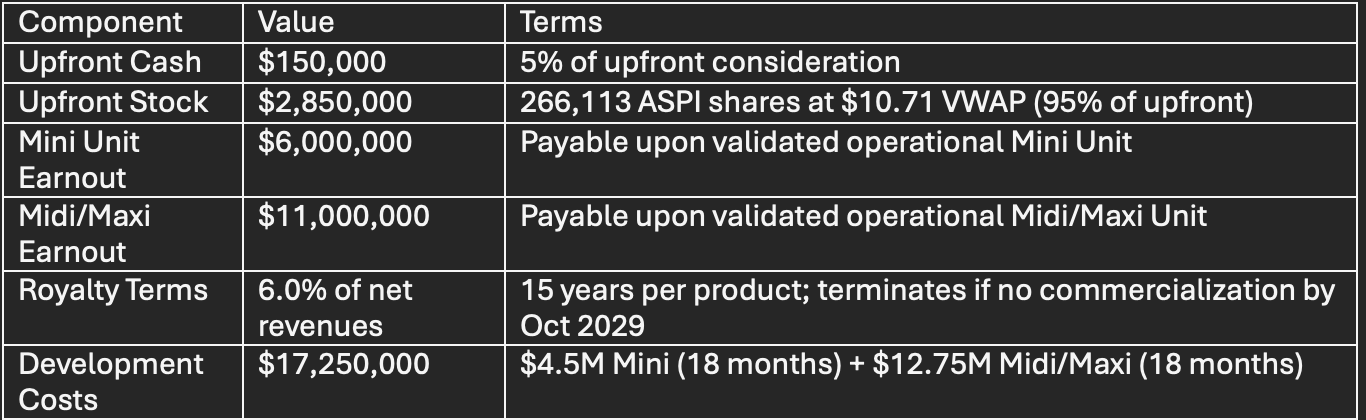

Total Deal Value: $20.0 million (15% upfront, 85% performance-based earnouts)

Deal Structure

Shareholder Impact: Minimal 0.3% dilution; stock issued at $10.71 vs. current $8.91 (this morning)

Strategic Rationale

Vertical Integration in Nuclear Fuel Cycle

QLE now operates across four critical segments:

Conversion - Uranium compound processing

Enrichment - HALEU production (TerraPower: 150 MT over 10 years starting 2028)

Deconversion - Enriched fuel preparation

Nuclear Waste Processing - NEW - Creber Units for water-soluble waste remediation

Market Opportunity

U.S. DOE Liability: $44.5 billion for commercial spent fuel disposal (2024)

Global Nuclear Waste: 390,000 metric tons (90,000 MT in U.S.)

High-Level Waste (HLW): 3% of volume, 95% of radioactivity, primary Creber Unit target

Nuclear Waste Management Market: $5.1B (2025) → $6.0-7.1B (2032-2033)

Technology and Business Model

Creber Units: Accelerated Beta Decay Technology

Target Isotopes: Cesium-137 and Strontium-90 (30-year half-lives)

Claimed Mechanism: Accelerate beta decay to rapidly convert long-lived isotopes to stable forms

Product Tiers: Micro, Mini, Midi, Maxi, modular deployment strategy enabling scalable capital deployment and mobile emergency response capability

Dual Revenue Model

1. Nuclear Waste Remediation Services

Target customers: Commercial utilities, DOE facilities, international operators

Value proposition: Reduce storage liability, accelerate waste volume reduction

2. Barium-137 Byproduct for Quantum Computing

Cs-137 decay produces stable Ba-137, critical for ion-trap quantum computing

ASPI announced Ba-137 purchase order (Sept 2025) for Q1 2026 delivery

Quantum computing market: $3.52B (2025) → $20.20B (2030) at 41.8% CAGR

Ion-trap quantum market: $370M (2024) → $3.4B (2033) at 28.7% CAGR

Competitive advantage: Waste-to-value circular economy model, extracting high-value material from paid waste processing

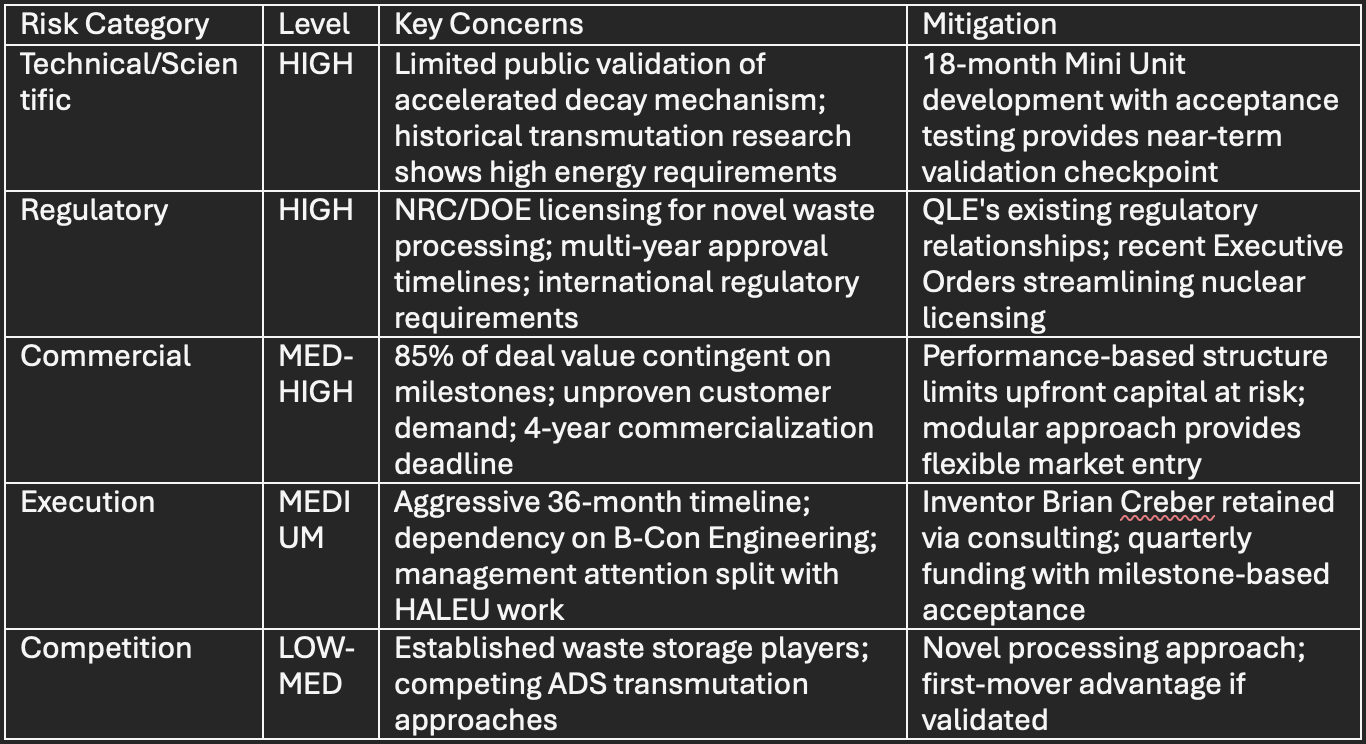

Risk Assessment

Investment Implications

Bull Case: Multi-Billion Dollar Opportunity

Technology validates with demonstrated accelerated decay rates

Clear regulatory pathway due to waste remediation benefits

DOE strategic engagement given $44.5B liability reduction potential

Profitable dual-revenue model (waste services + Ba-137 quantum computing materials)

QLE emerges as unique vertically-integrated nuclear services provider

Base Case: Niche Market Contribution

Technology demonstrates efficacy but economics challenged by energy/processing costs

Regulatory approval achieved but 3-5+ year timeline

Modest revenue contribution in specialized waste stream applications

Hundreds of millions in value creation within broader QLE portfolio

Bear Case: Value Destruction

Technology fails to demonstrate claimed capabilities

Regulatory barriers insurmountable or prohibitively lengthy

Processing economics cost-prohibitive vs. traditional storage

Earnout milestones not achieved; $3M+ development costs sunk

Key Monitoring Metrics

Immediate (0-6 months)

B-Con Engineering monthly milestone reports

Mini Unit budget adherence vs. $4.5M target

NRC/DOE preliminary regulatory discussions

QLE spin-out progress (planned 2H 2025)

Near-term (6-18 months)

Mini Unit acceptance testing and validation data

Publication of technical mechanism/peer review

$6M earnout decision and payment structure

First customer engagement or pilot program announcements

Medium-term (18-36 months)

Midi/Maxi Unit development progress

Regulatory approval pathway clarification

Commercial deployment announcements

Barium-137 production and quantum computing customer engagement

SEQH Capital Partners Investment View

Position: The One30Seven acquisition represents a high-risk, high-reward strategic option within ASPI’s portfolio, not a core near-term value driver.

Primary ASPI Value Drivers Remain:

Silicon-28/Ytterbium-176 commercial production (validated, ramping to 80kg annually)

HALEU enrichment for TerraPower (contracted 150 MT revenue starting 2028)

QLE spin-out creating separate public company valuation

Nuclear Waste Processing Adds:

Upside optionality if technology validates (18-month Mini Unit checkpoint critical)

Strategic positioning completing vertical integration across nuclear fuel cycle

Innovative waste-to-value model through quantum computing materials byproduct

Limited downside given modest $3M upfront and performance-based earnout structure

Recommendation: Monitor Mini Unit development closely over next 18 months as key determinant of acquisition value. The intersection of nuclear waste remediation and quantum computing materials represents a genuinely novel business model that could differentiate QLE if successfully executed. However, significant technical, regulatory, and commercial validation required before material revenue contribution.

SEQH Capital Partners Research

Independent Investment Research for Nuclear Energy Sector

October 23, 2025

FULL 12-PAGE REPORT BELOW: