ASPI Valuation

SEQH Capital Partners

Advanced Valuation – ASP Isotopes, Inc. (NASDAQ:ASPI)

Date: 4 October 2025

Dissemination: Internal Only – SEQH Capital Partners

Executive Summary – Buy

ASPI is a first-mover in a structurally under-supplied, policy-supported market. We value the equity at US $18.50 per fully-diluted share (base-case) and US $35.00 (bull-case) using a 10-year DCF that explicitly models three distinct revenue layers:

Specialty isotopes already shipping (Yb-176, Si-28, Mo-100)

Near-term nuclear medical expansion (PET cyclotron network, C-14, Zn-68)

HALEU / Li-6 enabled by the Fermi-America HyperGrid campus (2027-30)

The mid-point of our range implies >90 % upside to the 3-Oct close (US $9.34). Initiate over-weight.

Key Investment Thesis

Financial Model – 5-Year Outlook

Revenue is projected by isotope rather than segment to capture ASP’s pricing power (gross margin 45-65 %). All figures in US $ million.

Drivers

ASP already ships Yb-176 & Si-28; mg-gram scale prices US $2-4 k per gram → 70 % gross.

HALEU target price US $2.80 k per SWU (2022 DOE baseline); ASP’s laser enrichment 30-40 % energy efficient vs centrifuge → 50 % gross at scale.

Li-6 (99 % enriched) spot > US $15 k per gram; contract volume 10 kg yr⁻¹ per 100 MWe SMR.

DCF Valuation

WACC: 11.5 % (β 3.0, rf 4.2 %, MRP 7 %, post-tax cost of debt 8 %, D/E 1.5).

Terminal g: 4 % (in-line with long-run nuclear fuel demand).

Shares FD: 108.4 M (basic 94 M + 9.4 M options @ US $2.50, 5 M converts @ US $5.00).

Sensitivity to HALEU contract award – every additional 1 GW of secured off-take adds ≈ US $1.00 to fair value.

Balance-Sheet & Liquidity

Cash 30-Jun-25: US $67.8 M (10-Q)

Pro-forma Renergen cash contribution: +US ~25 M

Capex pipeline 2026-28: US ~120 M → fully covered by existing cash + SA debt package (IDC 70 %).

No near-term dilution required in base-case.

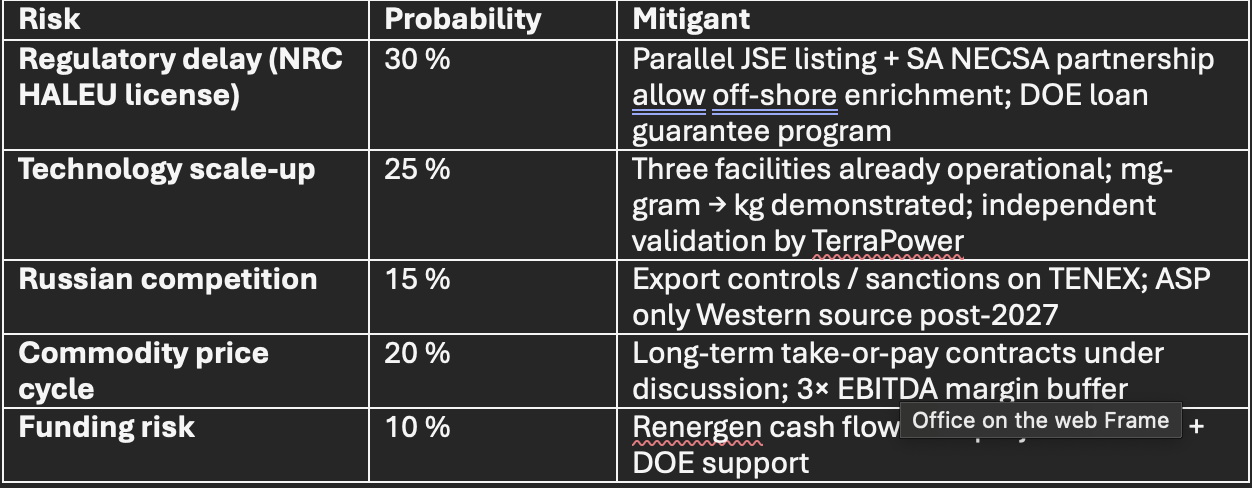

Risk Matrix

ESG / Policy Tail-wind

US Nuclear Fuel Working Group (2025) mandates non-Russian HALEU supply chain by 2028.

IRA Section 45V credits raise effective HALEU price by 30-40 %.

EU “Supply-Act” classifies Li-6 & Si-28 as strategic; ASP’s SA facility qualifies for ESG funds (carbon-negative helium).

Street vs. SEQH

Price Target & Catalyst Path

12-mo price target: US $18 (base-case DCF).

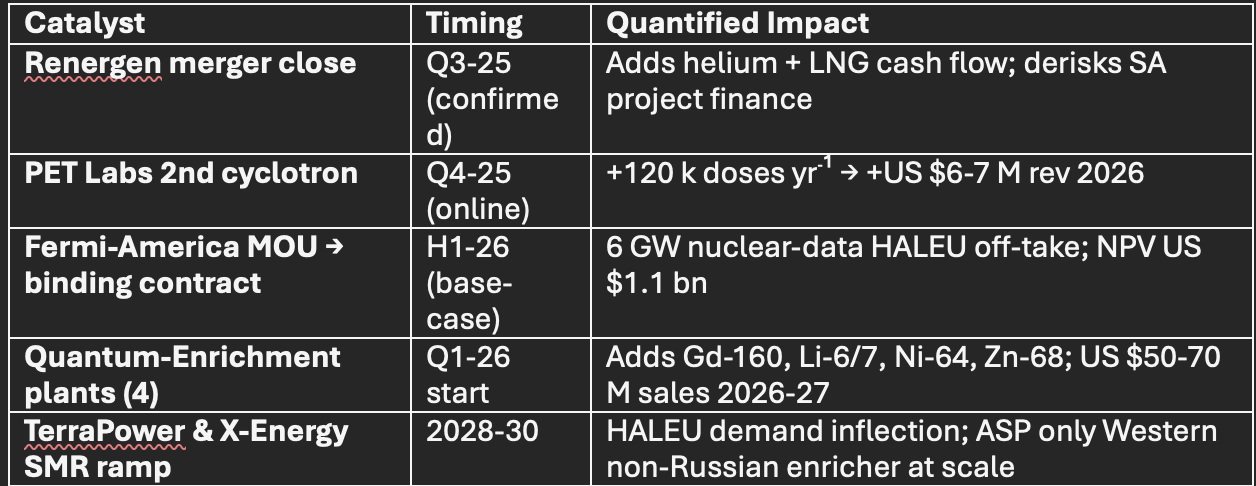

Catalyst timeline:

Nov-25: Q3-25 results – update on Fermi MOU term-sheet

Q1-26: Binding HALEU off-take (base-case assumption) → step-up revenue visibility

Q2-26: First 100 kg Yb-176 shipment → specialty isotope narrative validated

Q4-26: Break-even quarterly EBITDA → multiple re-rating to 20×+