Bitcoin-Related Equity Report

SEQH Capital Research | Bitcoin Equities Sector, Institutional Tear Sheet

October 30, 2025

Sector Overview

Q4 2025: Bitcoin mining firms aggressively pivot to AI data center and HPC hosting, chasing contracted, margin-rich revenue to offset post-halving profit squeeze.

Institutional capital flows dominate via BlackRock’s IBIT ($89.4B AUM, 60% U.S. ETF market), providing a price floor and accelerating sector maturation.

Halving effect: Network difficulty at all-time high (155.97T, 1,033 EH/s), compressing margins and driving consolidation, even among scaled operators.

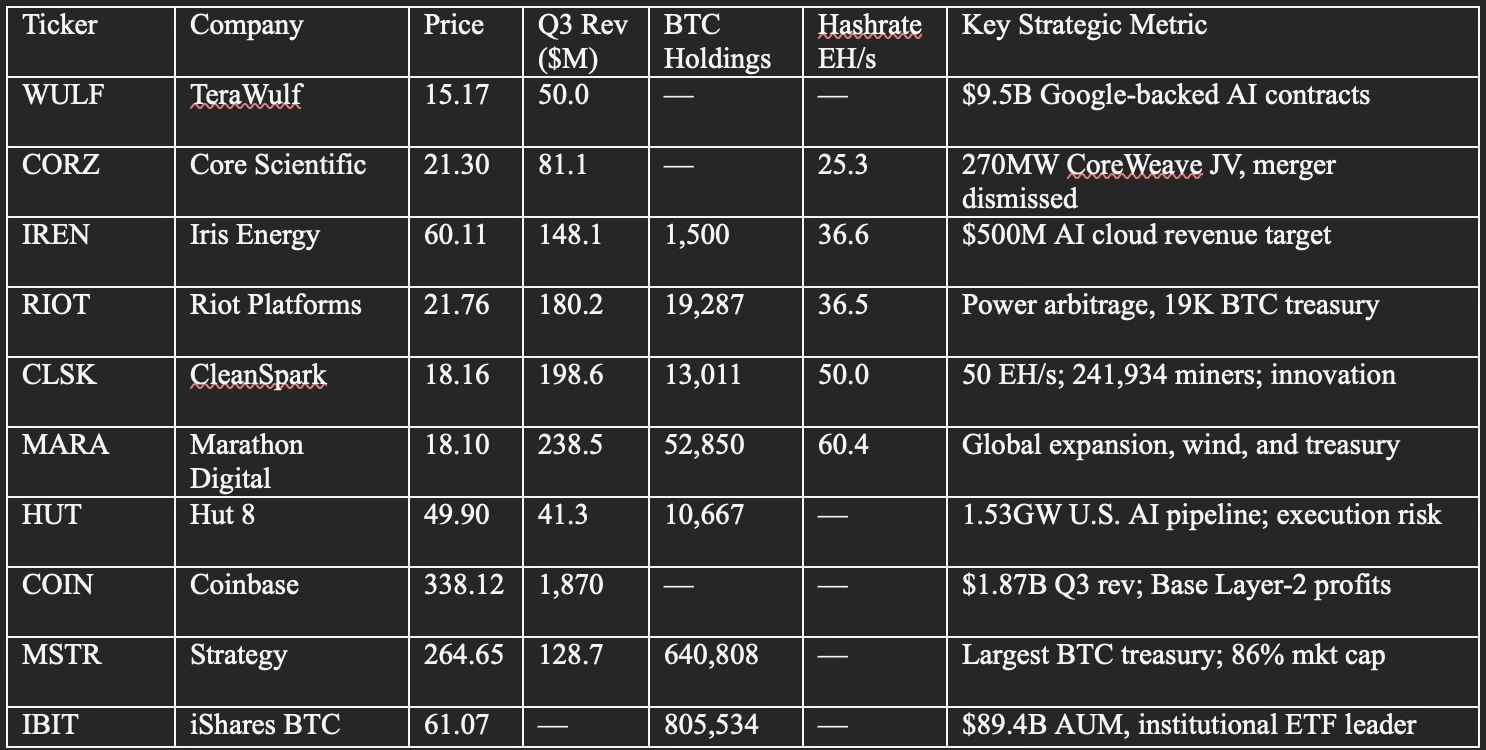

Top Companies & Strategic Themes

Macro Drivers and Catalysts

AI Pivot: Miners with large data center footprints (WULF, IREN, HUT) secure multi-billion dollar compute contracts, achieving revenue/margin transformation and infrastructure re-pricing.

ETF Flows: IBIT commands the ETF sector, compressing legacy GBTC (legacy outflows, high fees). ETF inflows stabilize trading, provide institutional access.

Treasury Accumulation: Strategy (640,808 BTC), Marathon, CleanSpark, equities trade increasingly as direct BTC proxies.

Risk/Return Profiles

Current Catalysts

AI campus construction (WULF, IREN, Bitfarms, HUT)

ETF flows, Q4 earnings launches (Cipher, Bitfarms, Hut 8)

Margin resilience testing as BTC volatility persists; margin squeeze may force additional consolidation.

Summary

Investors should overweight miners with AI pivots and contracted revenue (WULF, IREN), ETF leaders (IBIT), and disciplined treasury accumulators (CLSK, MSTR) for Q4 2025.

Avoid legacy products with persistent outflows/high fees (GBTC, BITO); tactical exposure only for aggressive traders.

Primary risks: Execution on infrastructure buildouts, equity dilution, regulatory environment, and extreme BTC drawdowns.

FULL EQUITY REPORT: