Bloom Energy Tear Sheet

PAID ONLY

BLOOM ENERGY CORPORATION (BE)

SEQH Capital Partners Research | Investment Tear Sheet

COMPANY OVERVIEW

Ticker: BE (NYSE)

Current Price: $93.01

Market Capitalization: $23.59 Billion

Report Date: October 22, 2025

Business Description:

Bloom Energy Corporation is a leading provider of solid oxide fuel cell (SOFC) technology for distributed on-site power generation. The company’s primary focus is the stationary power generation market, with particular strength in serving the rapidly expanding AI data center industry. Bloom’s proprietary SOFC technology offers a critical “time-to-power” advantage, enabling deployment in 3-6 months versus 4-5 years for traditional grid-connected solutions.

Core Technology:

Solid Oxide Fuel Cell (SOFC) Platform

Fuel-Flexible: Natural Gas, Biogas, Hydrogen

Rapid Deployment: 3-6 months time-to-power

Behind-the-meter distributed generation

99.999% uptime reliability

INVESTMENT THESIS

Key Drivers

1. AI Data Center Power Demand

The proliferation of AI and high-performance computing is creating unprecedented demand for reliable, scalable, rapidly deployable power. Traditional grid infrastructure cannot meet the speed requirements of data center operators, creating a massive opportunity for Bloom’s behind-the-meter solutions.

2. Strategic Brookfield Partnership ($5 Billion)

In October 2025, Bloom secured a transformative $5 billion partnership with Brookfield Asset Management, marking Brookfield’s first investment under its dedicated AI Infrastructure strategy. This validates Bloom’s technology at the highest institutional level and provides:

Massive capital commitment for global deployment

Preferred provider status for Brookfield’s AI factories

De-risked growth trajectory with predictable revenue pipeline

First European site expected to be announced by year-end 2025

3. Expanding Blue-Chip Customer Base

Oracle: Direct supply contract (July 2025) for AI data centers

American Electric Power (AEP): 1 GW deployment agreement

Equinix: Expanded partnership to 100+ MW across 19 data centers

4. Manufacturing Scale-Up

Doubling manufacturing capacity from 1 GW to 2 GW annually by end of 2026, requiring $100 million investment in Fremont, California facility.

FINANCIAL PERFORMANCE

Trailing Twelve Months (TTM)

Liquidity & Solvency

Growth Trajectory

Key Takeaways:

The company has achieved an inflection to sustained profitability, with strong margin expansion driven by operational efficiencies and scale. Massive earnings acceleration is expected through 2028, supported by a robust liquidity position that enables continued growth investments.

VALUATION ANALYSIS

Current Valuation Metrics

Analyst Price Targets

SEQH Valuation Commentary:

While valuation multiples appear elevated on traditional metrics, they are justified by the company’s unique market position in critical AI infrastructure, massive TAM with limited competition in rapid-deploy stationary power, and the de-risked growth trajectory via the Brookfield partnership. The company has a clear path to margin expansion and profitability with high barriers to entry in SOFC technology.

Our DCF analysis, incorporating accelerated growth from the Brookfield partnership and expanding hyperscale customer base, supports a fair value of $115, representing 24% upside from current levels.

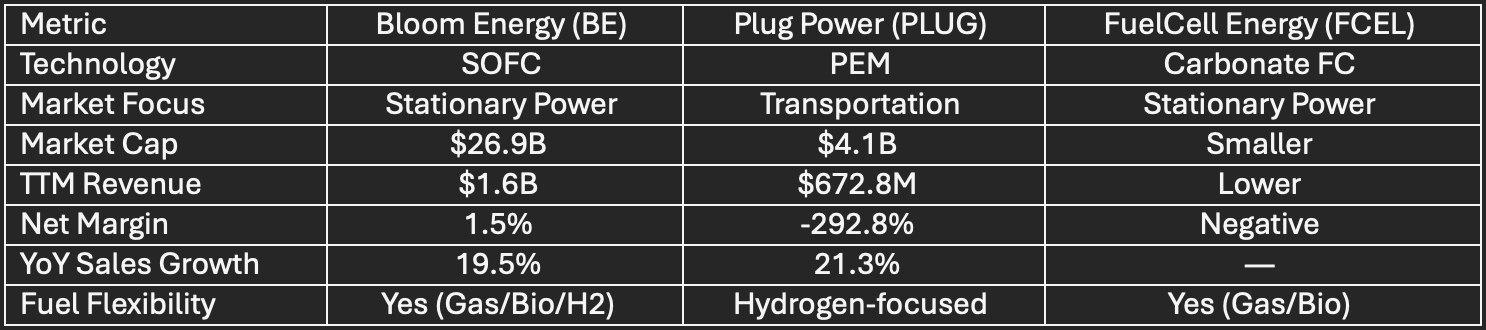

COMPETITIVE POSITIONING

Bloom Energy vs. Key Competitors

Competitive Advantages

Time-to-Power Leadership: Bloom’s 3-6 months deployment timeline versus 4-5 years for grid solutions is a critical differentiator. The company has proven technology with a large installed base achieving 99.999% uptime. Its fuel flexibility—running on natural gas today while being hydrogen-ready for tomorrow—provides operational flexibility and a pathway to decarbonization.

Strategic partnerships with Brookfield, Oracle, and AEP validate the company’s market position. The planned expansion to 2 GW manufacturing capacity by 2026 will enable cost leadership through economies of scale. Additionally, AI-optimized operations using data analytics from the installed base drive continuous efficiency gains.

KEY CATALYSTS & RISKS

Growth Catalysts

Continued AI Data Center Expansion: The secular megatrend in AI is driving unprecedented power demand, creating sustained tailwinds for Bloom’s solutions.

Additional Strategic Partnerships: The Brookfield success is likely to attract similar large-scale partnerships as the company becomes the preferred provider for AI infrastructure power.

Manufacturing Scale-Up Execution: Achieving 2 GW capacity unlocks significant cost advantages and enables faster deployment to meet customer demand.

Hydrogen Economy Development: Bloom’s fuel-flexible technology positions the company advantageously for the energy transition as green hydrogen infrastructure develops.

New Customer Wins: The pipeline of hyperscale and enterprise opportunities continues to expand, with potential for additional Fortune 500 data center operators.

Investment Risks

Execution Risk: Doubling manufacturing capacity is ambitious; construction delays or workforce challenges could impact the growth trajectory.

High Valuation: Premium multiples leave limited margin for error if the company fails to meet elevated market expectations.

Competition: Intensifying competition from Plug Power, FuelCell Energy, and potential new entrants could pressure margins and market share.

Fuel Supply Chain: Dependence on natural gas pricing volatility and the emerging hydrogen infrastructure presents supply chain risks.

Market Volatility: As a high-beta stock, Bloom is subject to sharp price swings that may not reflect fundamental performance.

Profitability Timeline: With narrow current margins (1.45%), successful scale execution is critical to achieving sustainable profitability.

INVESTMENT RECOMMENDATION

SEQH Capital Partners Rating: STRONG BUY

Fair Value Price Target: $115.00

Current Price: $93.01

Implied Upside: +23.6%

Investment Horizon: 12-18 months

Rationale

Bloom Energy stands at the epicenter of the AI infrastructure revolution. The convergence of massive AI-driven power demand, grid constraints, and the company’s unique time-to-power advantage creates a rare investment opportunity. The $5 billion Brookfield partnership represents an inflection point that de-risks the growth story and validates the technology at the highest institutional level.

While valuation multiples are elevated, they reflect the company’s dominant position in a massive, underpenetrated market, technological moat with high barriers to entry, clear path to profitability and margin expansion, and strategic partnerships providing predictable revenue growth.

The company is transitioning from early-stage losses to sustainable profitability, with earnings expected to surge 900% in Q3 2025. Manufacturing scale-up to 2 GW will drive operational leverage and cost advantages. The expanding customer base (Oracle, AEP, Equinix) and global deployment plans provide visibility into multi-year growth.

Key Risks to Monitor: Execution on manufacturing expansion, competitive dynamics, and ability to meet high market expectations.

Position Sizing Guidance

Given the high-growth, high-volatility profile:

Aggressive Growth Portfolios: 3-5% position

Balanced Growth Portfolios: 1-3% position

Conservative Portfolios: 0.5-1% position or avoid

CONCLUSION

Bloom Energy represents a compelling opportunity to gain exposure to the AI infrastructure megatrend through a differentiated technology platform. The company’s solid oxide fuel cell technology solves a critical pain point for data center operators: the need for rapid, reliable, scalable power deployment. The recent Brookfield partnership provides both validation and capital to accelerate global expansion.

While the stock trades at premium valuations, these are justified by the company’s unique market position, massive addressable market, and clear path to scaling profitability. The combination of secular tailwinds, strategic partnerships, and operational execution provides a strong foundation for sustained outperformance.

SEQH Capital Partners maintains a STRONG BUY rating with a $115 fair value price target.

Prepared by: SEQH Capital Partners Research Team

Date: October 23, 2025