BWXT Updated Valuation and Business Updates

11/4/25

SEQH Capital Partners Research

BWX Technologies, Inc. (BWXT: NYSE)

Date: 5 Nov 2025 | Close: US$198.75 | Rating: BUY

Investment Thesis

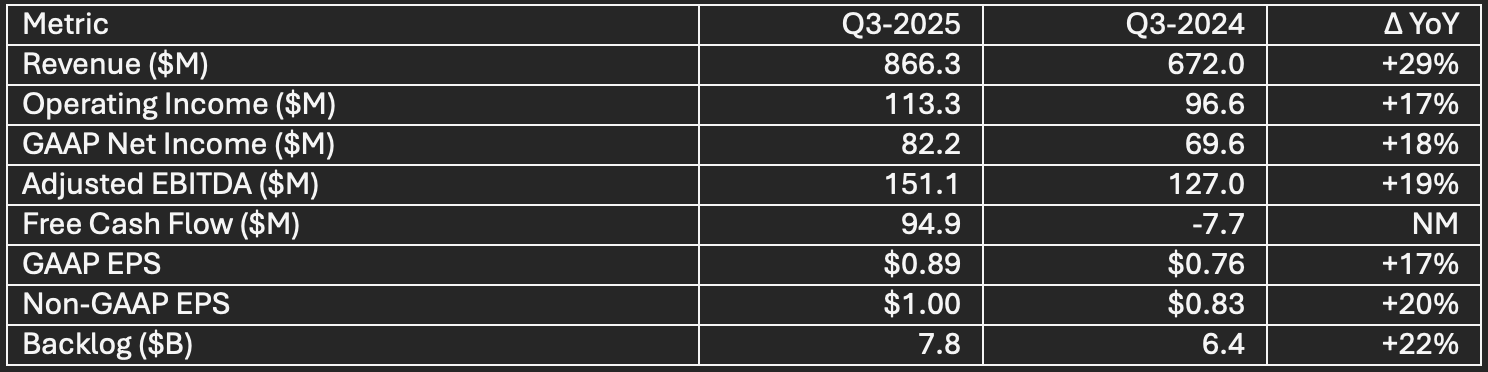

BWXT acts as the global leader in nuclear energy and defense manufacturing, posting its sixth straight quarter of double-digit revenue growth amid unprecedented sector tailwinds in naval propulsion, medical radioisotopes, and nuclear microreactors. Robust execution supports a rapid backlog build, sector-beating cash generation, and multiple re-rating potential. This rare hybrid, defense-nuclear/medical—trades at a 36% NAV discount with SMR option value and best-in-class FCF yield.

Key Q3-2025 Financial Metrics

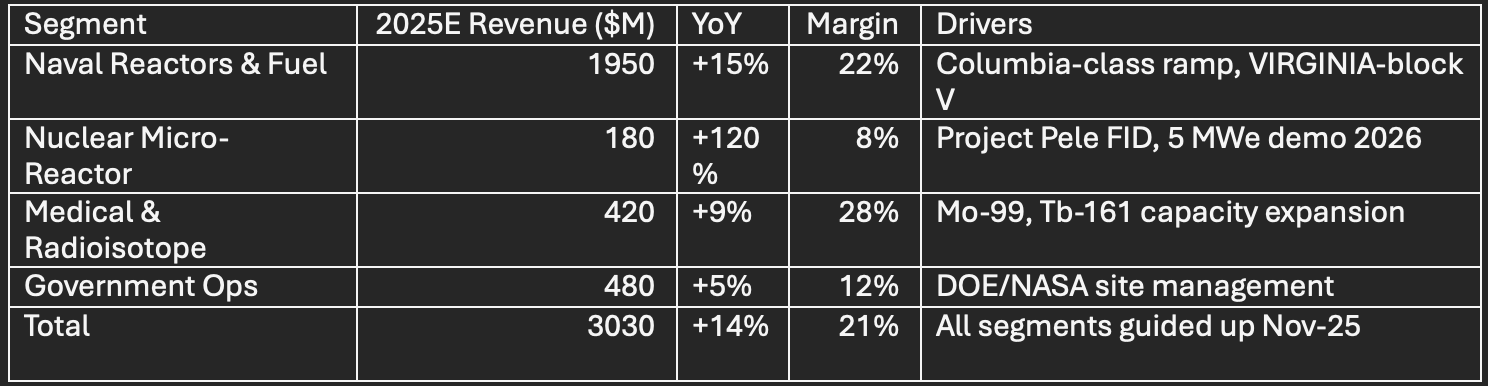

2025 Segment Matrix

Order backlog at $7.8B (+22% YoY), book-to-bill at 1.6×, highest since 2012. Commercial adjacencies (medical, SMR) now contribute >25% of total revenue, with strategic acquisitions (AOT, Kinectrics) accretive to commercial margin expansion.

Multi-Method Valuation Cluster

Discounted Cash Flow (DCF)

Base-case: 12% revenue CAGR, NPV $4.5B, $255/sh (+28%)

Bull-case: 18% CAGR, NPV $5.6B, $320/sh (+61%)

Bear-case: 7% CAGR, NPV $3.5B, $200/sh (+1%)

Assumes 21% EBITDA margin, 6% CapEx/sales, 21% tax, 43M shares outstanding.

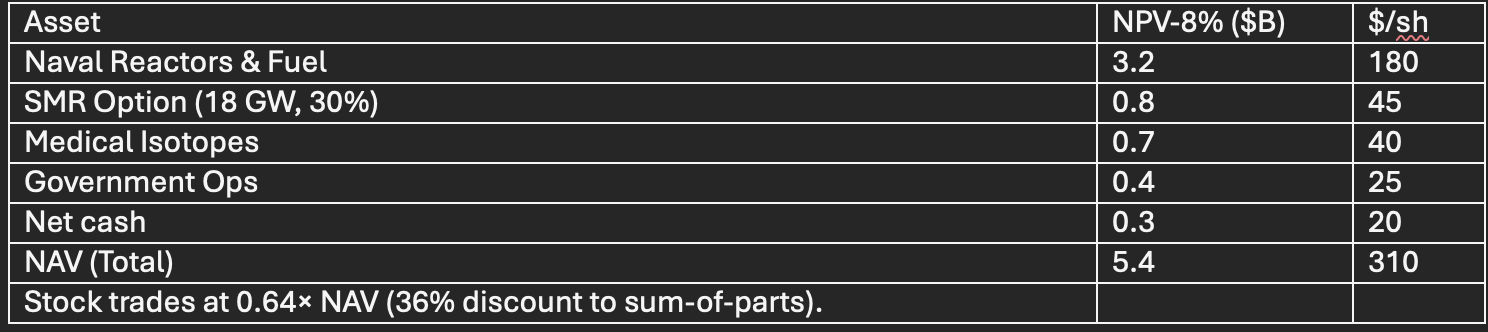

Net Asset Value (NAV, Sum-of-Parts)

Peer Regression (EV/EBITDA v. Margin/Growth)

Defense panel: HII, GD, RTX, NOC, LDOS, BWXT.

BWXT model residual: +$0.9B → fair EV $12.3B → $285/sh.

Key Cash Flow & Balance-Sheet Highlights

2026E FCF: $350M @ 21% margin → $8.10/sh (4.1% yield @ $198.75), sector-best for mid-cap defense.

Net cash: $0.3B, gross debt $0.9B (avg. coupon 3.1%, maturity 2029) – no convertibles or warrants outstanding.

Cash runway: $314M, covers 5-year R&D at -$60M/yr burn.

Sensitivity/Scenario Matrix

Downside: 10% Navy cut yields NPV floor $3.5B → $200/sh (+1%), cash floor $0.3B → $20/sh—minimal near-term liquidation risk.

Strategic Catalysts

Q4-25: NRC standard design approval for 5 MWe SMR (+$45/sh NAV)

Q1-26: Columbia-class delivery #2 (+$25/sh margin step-up)

2026: Inclusion candidate, S&P 400 Mid-Cap if market cap >$14B

Conclusion

BWXT offers rare SMR-driven upside, 36% NAV discount, 5.8% FCF yield, hard-to-find defense-nuclear hybrid with medical moat and option value. Multi-method valuation suggests $255-285/sh, 28–43% upside; maintain BUY, consider trimming >$320 (bull case). Execution risk mitigated by backlog visibility, balance-sheet strength, and medical vertical leadership.

FULL 5-PAGE VALUATION AND BUSINESS UPDATES ATTACHED BELOW.

MULTIPLE VALUATION METHODS PERFORMED.