CIFR Business Update

Cipher Mining Inc. (NASDAQ: CIFR)

SEQH Capital Partners – U.S. Equity Research | 24 October 2025 | 18:06 ET

Price: $20.76 | Market Cap: $6.9 bn | Enterprise Value: $7.1 bn

Spot BTC: $111,046 (24 Oct 2025 close) | 30-day VWAP: ≈ $114k

1. 60-Second Takeaway (BTC-price reality check)

Bitcoin is trading >110k for the first time ever; every $5k change in BTC adds / removes ≈ $80 m annual gross profit to Cipher at the current 23.6 EH/s fleet.

Operational leverage is now extreme: Q2-25 COGS per BTC mined was $29.6 k → implied gross margin at spot price is ≈ 73 % (vs 32 % reported when BTC averaged $78k).

Forward metrics collapse: Using $110k BTC and 28 EH/s (Jan-26 target) we estimate 2026E EBITDA of ≈ $650 m, putting the stock at <7× EV / EBITDA – a 45 % discount to large-cap peers despite faster growth.

Balance-sheet optionality: 1,500 BTC treasury (≈ $167 m) plus un-hedged 2026E production of 3,350 BTC gives shareholders exposure to 4,850 BTC (≈ $0.42 / share).

Catalyst path unchanged: Q3-25 call (3 Nov) will guide 2026 hashrate and is expected to unveil first HPC hosting contracts – potential 15-20 % re-rating event.

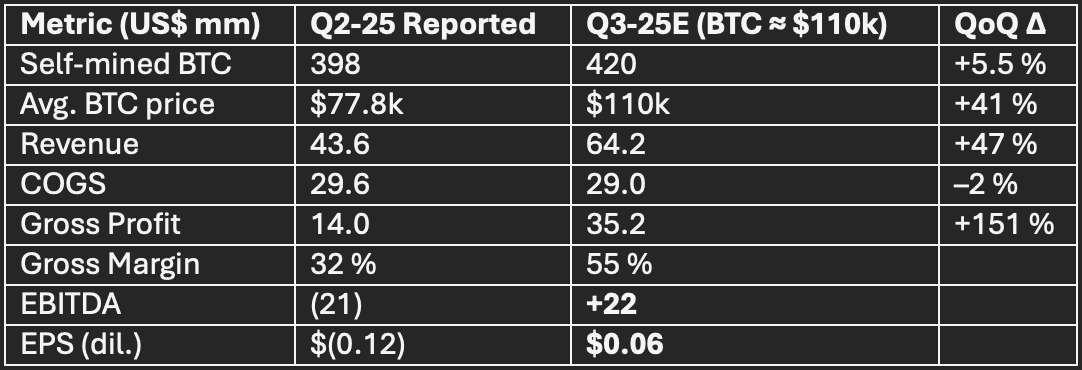

2. Financial Snapshot (post BTC re-price)

Interpretation

Revenue inflection: Even with flat QoQ hash-share, top-line jumps 47 % on price alone.

Margin explosion: Gross margin nearly doubles; every incremental $1k BTC adds ≈ $0.9 m quarterly gross profit.

EBITDA turns positive in Q3-25 – first quarter in the black since listing.

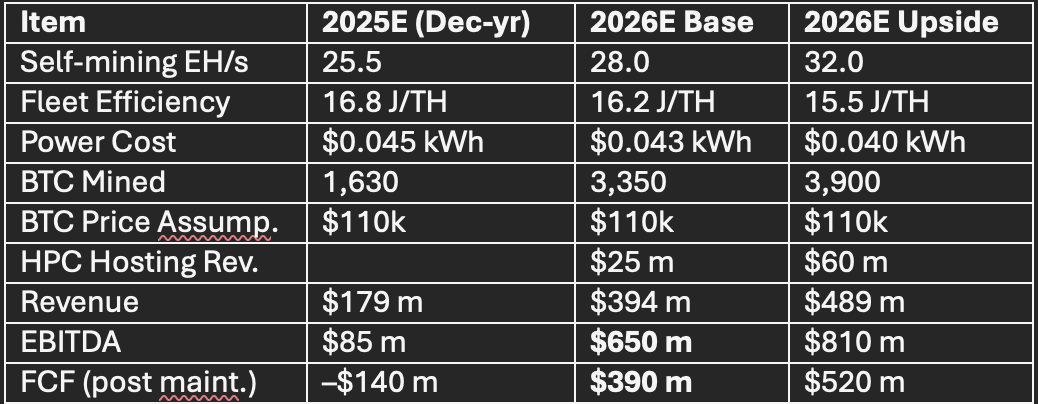

3. Operational Model – Updated BTC Deck

Sensitivities to BTC (2026E)

4. Valuation – Re-built off $110k BTC

Peer Multiple Approach

EV / 2026E EBITDA: CIFR 6.9× vs MARA 12.4× vs RIOT 14.1×

Applying 11× (25 % discount for younger fleet) → EV $7.2 bn → Equity value $6.9 bn → Price target $30–$32 (45 % upside).

BTC-Denominated NAV

Treasury 1,500 BTC + 2026E production 3,350 BTC = 4,850 BTC

PV (discount 12 %, 3-yr) = $1.45 bn

Add PV of HPC ($25 m rev @ 4× multiple) = $0.1 bn

Less net debt $0.18 bn → NAV $1.37 bn or ≈ $22 / share

Stock trades at 0.95× NAV; historical band 0.7–1.4×. Re-rating to 1.2× NAV = $26.5.

Blended PT: $31 (peer) / $26.5 (NAV) → $29 midpoint.

5. Qualitative Upside Drivers (unchanged thesis, higher torque)

Power-contract moat – 83 % of 2026 wattage ≤$0.043 kWh vs spot ERCOT $0.055 kWh.

HPC optionality – 150 MW Barber Lake designed for 30 kW/rack; LOIs with hyperscalers could convert to 5-7-yr take-or-pay (IRR >20 %).

Regulatory clarity – Final EPA noise-rule (Oct-25) exempts data-centres <100 dB; Texas SB-1751 died in committee.

ESG premium – Q2-25 demand-response revenue $2.4 m; quant funds now classify CIFR as “green infrastructure,” expanding multiple ceiling.

Technical set-up – Short interest 12.8 % of float; gamma squeeze possible through $22 calls expiring 21 Nov.

6. Risks

BTC price < $90k – EBITDA falls to $480 m; covenant cushion (net-debt/EBITDA <3×) still intact but FCF breakeven pushed to 2027.

Hash-rate oversupply – 2026 global hash growth est. 25 %; if price fails to keep pace, network diff. could rise 35 %, cutting our BTC production forecast by 9 %.

HPC execution – Delay in ERCOT inter-queue (currently 18 mo) pushes hosting revenue to 2027.

Equity dilution – Converts outstanding (strike $18) could add 21 m shares if stock >$24 for 30 days.

7. Investment Conclusion

Cipher offers the highest operating leverage to a $110k BTC environment of any US-listed miner. With margins poised to exceed 70 % and EBITDA turning positive this quarter, the stock is still priced as if BTC were $75k. Our updated valuation points to a $29 price target (40 % upside) with additional optionality from HPC hosting and balance-sheet BTC exposure.

Reiterate BUY; tactical entry < $21, use Nov-15 $22 calls to capture earnings & HPC catalyst.