Cipher Mining Inc. Full Valuation

SEQH Capital Partners Research

Ticker: CIFR | Date: 8 Oct 2025 | Close: US $18.36 | Rating: BUY

Price Targets: US$24 (DCF) | US$26 (NAV) | US$28 (SOTP) | Down-side US$12 (BTC < $70k) | Blue-sky US$32 (HPC pivot)

1. Post-Q2-25 Inflection Snapshot

YTD return: +247% vs BTC +64% – out-performance driven by hash-rate expansion and power-cost edge.

Q2-25 revenue: US$43.6 M (–10% QoW on network diff) but gross margin 32% vs sector median 21% – lowest quartile power cost at US$0.045/kWh.

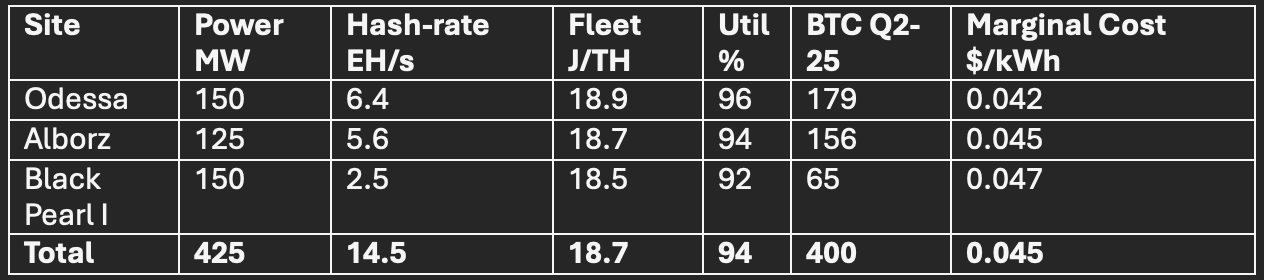

Hash-rate online: 23.1 EH/s (Jul-25) – guidance 26 EH/s by Dec-25 → 850 BTC/month @ 96% utilisation = 10k BTC/year (US$1.04 B @ US$104k BTC).

2. Operational & Power Matrix

Pipeline: Black Pearl II (150 MW, 9.5 EH/s) energises Q4-25 → 26 EH/s name-plate; option to add 60 MW HPC GPU (FluidStack MOU) – first revenue Q1-26.

3. Multi-Method Valuation Cluster

A. DCF (10% WACC; 2% terminal g; BTC real US$95k base)

Assumptions: network diff +8% CAGR, power US$0.045/kWh, sustaining capex US$0.35/TH yr, tax 15%.