LLY Full Valuation

SEQH Capital Partners Research

Ticker: LLY | Date: 11 Oct 2025 | Close: US $826.26 | Rating: BUY

Price Targets: US$950 (DCF) | US$970 (NAV) | US$990 (SOTP) | Down-side US$720 (pipeline miss) | Blue-sky US$1,050 (accelerated launches)

1. Post-Q2-25 Set-Up

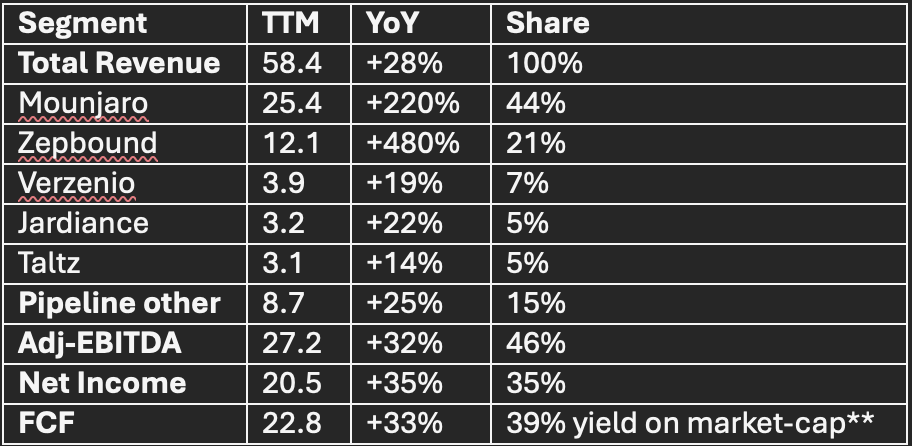

Friday close: US$826.26 → EV US$780 B (net cash) → EV/EBITDA 28.7× vs big-pharma median 16.5× – premium justified by 30% revenue CAGR (2024-27E).

Q2-2025 revenue: US$15.1 B (+22% YoY) – eleventh straight quarter of >20% top-line growth; adj-OP margin 45.1% (sector-best).

2. Revenue & Profitability Deep Dive (TTM US$B)

3. Multi-Method Valuation Cluster

A. DCF (7.5% WACC; 2% terminal; USD)

Assumptions: 45% OP margin, R&D 19% of sales, net capex 8% of revenue, tax 15%.

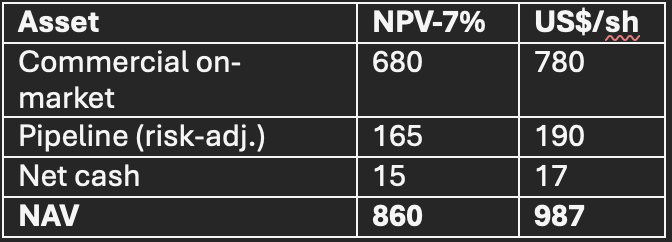

B. NAV (sum-of-parts DCF of products + pipeline)

Stock = 0.84× NAV → fair value vs 1.0× peer average.

C. Peer Regression (EV/EBITDA vs. margin & growth)

Panel: JNJ, PFE, MRK, ROG, ABBV, AMGN Model: EV = α + β₁(EPS-g) + β²(EBITDA-m) + β³(div-y) LLY residual +US$120 B → fair EV US$900 B → US$970/sh.

4. Cash-Flow Leverage to GLP-1