Market Brief 10/8/25

Market Digest

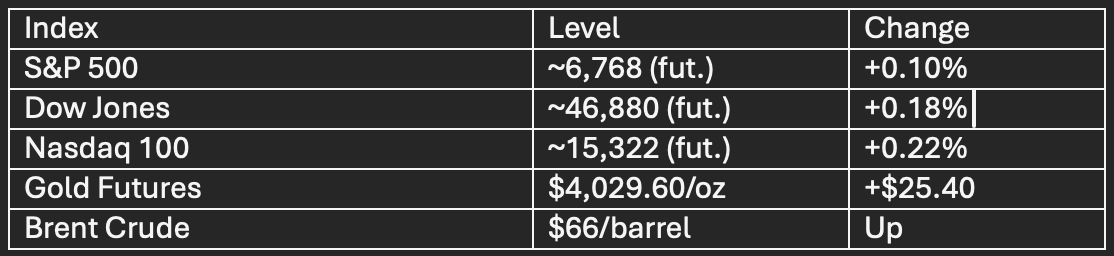

U.S. equity markets are navigating mixed signals amid ongoing government shutdown and anticipation for the Federal Reserve’s September meeting minutes, now due later today. Overnight, futures inched higher after Tuesday’s declines, with the S&P 500, Dow, and Nasdaq futures each up about 0.2% in early pre-market action, maintaining proximity to record highs despite volatility tied to tech sector profit warnings and AI bubble concerns, notably Oracle’s cloud margin disappointment.

Gold surged to a new all-time high above $4,000/oz, driven by flight-to-safety responses in light of protracted political uncertainty and softening economic data. Oil also saw upward movement after reports revealed a decline in U.S. stockpiles at key storage hubs and OPEC+ maintained tight supply quotas, with Brent crude trading above $66/barrel.

The government shutdown, now in its eighth day, has delayed important economic releases, including the September jobs report. However, labor-market resilience and corporate travel demand remain supportive for cyclical sectors entering Q4, with market focus shifting toward upcoming results from Delta Air Lines and PepsiCo this week.

Market Watch

Indices Snapshot (Pre-Market, 10/8/25)

Economic Calendar Highlights

MBA 30-Yr Mortgage Rate: 6.46% (rising rate sensitivity)

Core PPI YoY: 2.8%; PPI YoY: 2.6% (muted pricing pressures, slightly below prior period)

Retail Sales ex-Gas/Autos MoM: +0.7% (consumer spending outpaces expectations)

Jobless Claims: 1,940,000 (steady labor market)

Fed commentary expected from Presidents Musalem, Barr, Kashkari

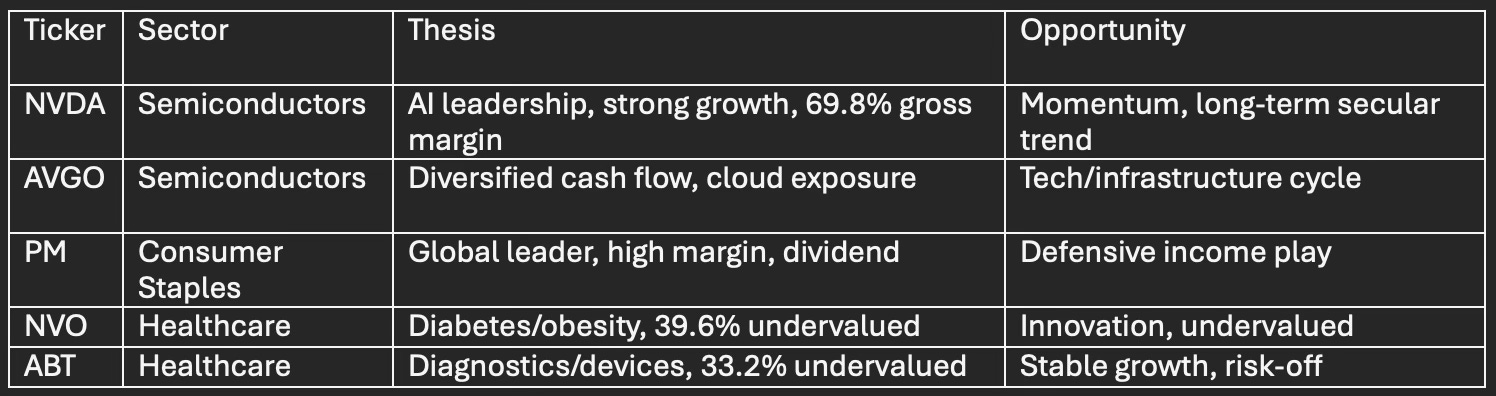

Stock Idea: Abbott Laboratories (ABT)

Diversified healthcare leader, 33.2% undervalued, with 19.6% one-year return and robust free cash flow

Catalysts: Expansion in diagnostics/devices, emerging markets growth, product innovation

Defensive positioning ideal for uncertain macro outlook, targeting stable cash flows during volatility

Market Movers

Technical Analysis: S&P 500 & Sector Highlights

S&P 500 remains in a bullish uptrend supported above the 20-day moving average (~6,650) and all major daily/weekly moving averages.

Momentum signals (RSI: 69.5; MACD, ADX, CCI: all “Buy”) point to sustained trend, but Williams %R (-14.5) shows nearing overbought territory, cautioning for a short-term pullback or consolidation toward 6,500, with significant support at 6,350 and 6,200 below.

Utilities sector outperforms as flight-to-safety; traders rotate away from Consumer Discretionary toward Staples; Insurance favored over Banks as volatility builds.

Curated Stock Picks & Opportunity

For value-oriented ideas: AMCX, AVO, PGR (Insurance), and CDE (Miners) appear among top Zacks “Strong Buy” picks for the session.

High-yield dividend: MO, CVX, EPD, VZ offer >4% yields, attractive for income-focused positioning amid uncertainty.

Short-Term Technical Watch

S&P 500 support: 6,500, 6,350, 6,200.

Momentum still favors upside, but vigilance warranted for near-term volatility spikes in AI stocks (NVDA, AVGO) post-Oracle warning.

Consider gradual rotation into defensive names and accumulate medical device/healthcare stocks like Abbott during sector volatility.

Recommendation: Maintain balanced exposure with overweight positions in semiconductors, healthcare innovation, and select consumer staples. Consider short-term hedging for elevated tech volatility and scale into defensive sectors ahead of anticipated Q4 seasonally strong cycle.