Market Brief

11/21/25

MARKET TEARSHEET

Friday, November 21, 2025 | 6:27 AM EST

MARKET SNAPSHOT

Index Performance (as of Nov 20 close)

S&P 500: 6,538.76 (-1.56% day | -2.9% week | +15.8% YTD)

Nasdaq Composite: 22,078.05 (-2.15% day | -3.6% week | +19.2% YTD)

Dow Jones: 45,752.26 (-0.84% day | -3.0% week | +12.4% YTD)

VIX: 26.42 (+11.67% day | +53.96% YoY) - Elevated fear levels

Pre-Market Futures (6:27 AM)

S&P 500 Futures: -0.01% (flat)

Nasdaq 100 Futures: -0.25%

Dow Futures: +142 pts (+0.31%)

MACRO SNAPSHOT

Today’s Economic Calendar

9:45 AM ET: Manufacturing PMI (exp. 52.0 vs. 52.5 prior) | Services PMI (exp. 54.6 vs. 54.8 prior)

10:00 AM ET: University of Michigan Consumer Sentiment FINAL (exp. 50.3 - near-record low)

Current Conditions: 52.3 (all-time low)

1-Year Inflation Expectations: 4.7% (vs. 4.6% prior)

Throughout Day: 5+ Federal Reserve officials speaking on rate outlook

Fed Rate Cut Expectations

December Rate Cut Probability: 37% (down from 97% in mid-October)

Current Fed Funds Rate: 3.75%-4.00%

Market fully pricing continuation; cut odds collapsed post-strong jobs report

Yield Environment

10-Year Treasury: 4.07% (-2bp, but up 11bp monthly)

2-Year Treasury: 3.53% (-1.9bp)

30-Year Treasury: 4.71% (-1bp)

Commodities

WTI Crude Oil: $57.51/bbl (-2.5% day | -1.7% monthly)

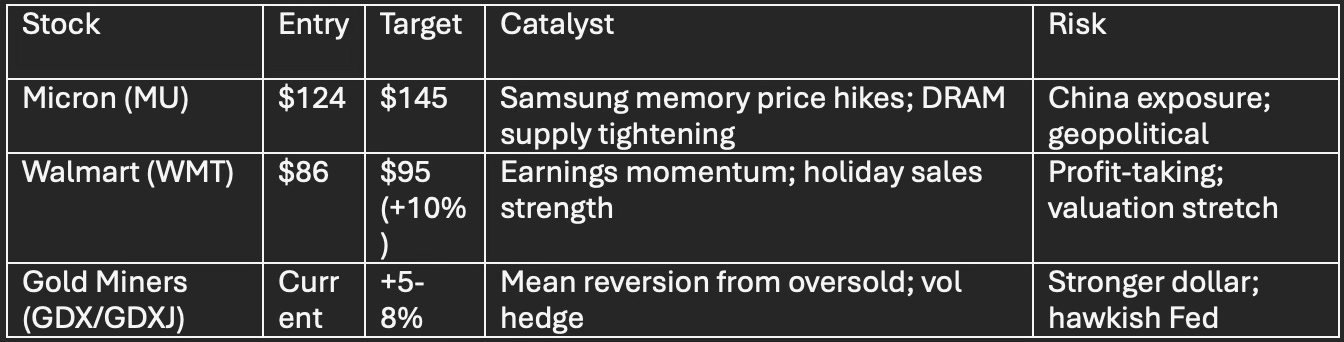

Gold: $4,031.94/oz (-1.1% day | -1.7% monthly) - Rate cut skepticism pressuring

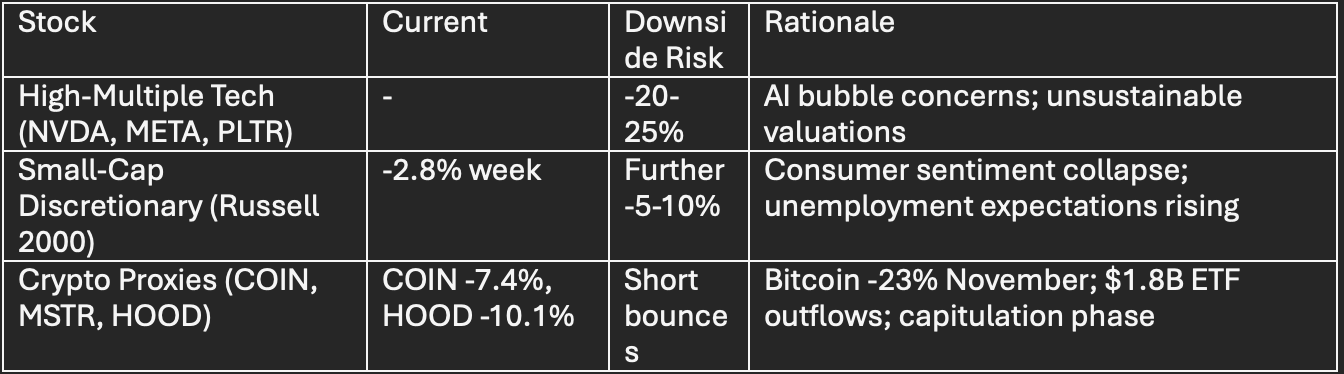

Bitcoin: $84,000 early Friday | -23% November (worst month since 2022)

EARNINGS & ANALYST ACTION

Yesterday’s Standout: Walmart (WMT)

Results: Revenue $179.5B (+5.8% YoY, beat $177.6B cons) | Q3 EPS beat

Stock Reaction: +6.5% (best S&P 500 performer)

Key Driver: E-commerce +28% domestic (+27% global) | Advertising +53%

Raised Guidance: FY sales growth now 4.8%-5.1% (from 3.75%-4.75%)

Analyst Action: BMO Capital raises target to $125 (implies +45% upside)

Catalyst Ahead: Nasdaq listing effective Dec 9; 50%+ e-commerce automation

Nvidia (NVDA) - The Disappointment

Beat Earnings: Q3 revenue $57B (+62% YoY) | Q4 guidance $65B (vs. $62B cons)

Stock Reaction: +5% premarket → -3.2% close (worst reversal this week)

Concern: 4 customers = 61% of revenue (concentration risk) | $500B order book sustainability questionable

Analyst Guidance: KeyBanc Buy $275 | Goldman Sachs Buy $250

Technical: Resistance at $186 rejected; support at $180.64 critical

Other Key Actions

Goldman Sachs downgrades Bath & Body Works (BBWI): Buy → Neutral | Target cut $39 → $17 (-56%)

Stock reaction: -25% (worst non-tech performer)

AON downgraded Overweight → Equal-Weight (Barclays, $379 target)

BMO Capital upgrades Walmart to $125 on omnichannel success

Today’s Pre-Market Earnings

BJ’s Wholesale (BJ): EPS $1.10 (cons -6.8% YoY)

Azenta (AZTA): EPS $0.21 (cons +16.7% YoY)

Moog Inc. (MOG.A): EPS $2.24 (cons +3.7% YoY)

SECTOR PERFORMANCE & ROTATION

Winners (Week)

Consumer Staples: +1.5% | Defensive rotation into weakness

Utilities: +0.4%

Losers (Week)

Technology: -2.7% | Nvidia reversal; semiconductor rout

Consumer Discretionary: -2.3% | BBWI collapse

Materials: -1.8% | Commodity weakness

Energy: -1.5% | Oil decline

Key Takeaway: K-Shaped Economy - Walmart thrives (+6.5%) while University of Michigan sentiment near all-time lows (50.3); affluent consumers spending while lower-income retrench; 71% expect unemployment to rise.

TOP STOCK MOVERS

LONGS (Near-Term 1-4 weeks)

AVOIDS/SHORTS (Risk-Off)

TECHNICAL ANALYSIS

S&P 500 Key Levels

Resistance: 6,760 (gap level) | 6,830 (intraday high)

Current: 6,538 (below 20-day MA at 6,772)

Support (CRITICAL): 6,544 (20-week MA) | 6,500 | 6,400 (year-to-date low)

Pattern: Head & Shoulders complete; bearish engulfing; oversold momentum

VIX Regime: 26.42 signals elevated risk; expect 22-28 trading range

Nvidia Technical Watch

Highest 7-day straddle IV (7.3% of stock price) since 10-report history

Resistance rejected at $186 | Support at $180.64 critical

Further downside if closes below $180.64

Volatility Compression Expected

VIX elevated but not panicking (would be 30+)

Low-volume holiday week ahead will amplify moves on thin liquidity

Thanksgiving seasonality typically positive (+0.67% average S&P 500)

WEEK AHEAD OUTLOOK (Nov 25-29 — Thanksgiving Week)

Base Case: Choppy Consolidation (Flat to +1%)

S&P 500 consolidates 6,500-6,650 range

Modest Santa Claus rally attempt into Thanksgiving

Sector rotation Staples > Tech persists

VIX stabilizes 22-25; not collapsing or spiking further

Bull Case Triggers (+2-3%)

Oversold conditions mean-revert

Dovish Fed commentary reverses rate cut pessimism

Short covering into month-end positioning

Thanksgiving seasonality positive

Bear Case Triggers (-2-3%)

December cut odds drop below 25% (further decline)

Bitcoin breakdown cascades into broader risk-off

Nvidia/semis continue lower (technical breakdown)

Consumer spending disappoints Black Friday data

Key Data Points

Wed: GDP Q3 (second estimate) | Durable Goods | Fed Beige Book

Thu (Half-day): Holiday shortened week

Fri (Full close): Last trading day before Dec 1

PORTFOLIO POSITIONING

Recommended Allocation (Next 4 Weeks)

Equities: 55-60% (underweight vs. 65% normal baseline)

Fixed Income: 25-30% (overweight; extend duration)

Cash: 10-15% (elevated dry powder for dips)

Alternatives: 5% (commodities/gold hedge)

Sector Overweights: Consumer Staples | Utilities | Healthcare | Select Financials

Sector Underweights: Technology (esp. semis) | Consumer Discretionary | Materials

Options Strategy

Long VIX calls (Dec/Jan) for portfolio insurance

Covered calls on tech holdings to harvest premium

Put spreads on Nasdaq 100 for downside protection (22,000/21,500 strike)

Bull call spreads on Consumer Staples (WMT, PG, KO)

CRITICAL LEVELS TO WATCH

S&P 500

Hold above 6,544 (20-week MA): Constructive year-end setup

Break below 6,544: Opens door to 6,300-6,400 by early December

Nasdaq 100

Close above 18,565 stabilizes near-term dynamics

Below 18,000 confirms breakdown; targets 17,500

Bitcoin

Support: $80,000 (psychological) | $75,000 (major support)

Resistance: $90,000 (pre-crash peak)

$1.8B ETF outflows signal capitulation phase nearing completion

VIX

Hold 22-28 range = Normal elevated

Break 30+ = Market emergency scenario

Drop below 20 = Complacency return

ACTION ITEMS FOR FRIDAY

9:45 AM ET

Monitor Manufacturing & Services PMI

Above consensus → Fade any morning rally by 11 AM

Below consensus → Accelerate downside; watch for VIX spike to 28-30

10:00 AM ET

University of Michigan Sentiment (KEY): Expected 50.3

Watch 1-Year Inflation Expectations (cons 4.7%)

Unemployment expectations signal important consumer health indicator

Throughout Day

Track Fed speaker commentary for rate cut signals

Expect choppy, directionless midday trade

Position for early close; many desks booking profits ahead of Thanksgiving

Year-End Setup

Next major catalyst: December 17-18 FOMC meeting

Limited economic data between now and year-end

Favorable: Holiday-shortened weeks reduce volatility

Unfavorable: Low liquidity amplifies intraday swings

BOTTOM LINE: Markets testing critical support at S&P 500 6,544 (20-week MA). Consumer sentiment near all-time lows while wealthy households (Walmart) thrive, K-shaped recovery intact but fragile. Fed cut probability collapsed to 37%; next catalyst December FOMC. Use Thanksgiving week seasonality for tactical entries; maintain 10-15% cash. Avoid high-multiple tech on any bounce; overweight Staples/Utilities.

SEQH Capital Partners Research | Tear Sheet | November 21, 2025 | 6:30 AM EST