Market Brief + Model Portfolio Risk Assessment

MARKET TEAR SHEET – OCTOBER 29, 2025

SEQH Capital Partners Research

KEY THEMES

Fed Rate Cut Day: The Federal Reserve is widely expected to cut its benchmark interest rate by 0.25% this afternoon (to 3.75–4.00%), marking a second consecutive cut as the central bank pivots to support a softer labor market, even as inflation remains above target. Powell’s press conference (2:30 ET) will determine market trajectory for the rest of Q4.

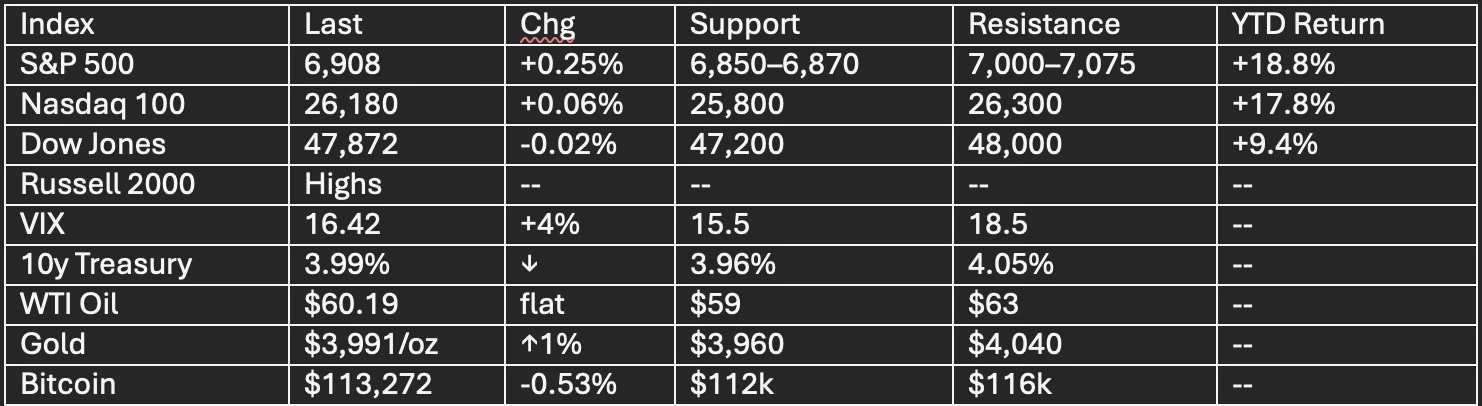

All-Time Highs: S&P 500, Nasdaq, and Dow closed at record levels Tuesday. S&P 500 is above 6,900 premarket.

Earnings Supercycle: Microsoft, Alphabet, Meta report after close today; Amazon and Apple tomorrow. Combined capex guidance of $400B+ for 2025–26 is key for AI sector momentum.

U.S.-China Trade Breakthrough: Summit set for Thursday, framework for tariff relief, rare earth exports, and agricultural purchases fuels cyclical sector rally.

MARKET SNAPSHOT

TODAY’S CATALYSTS & ECONOMIC EVENTS

2:00 ET | Fed Rate Decision – 0.25% cut expected

2:30 ET | Powell Press Conference – Guidance on December, labor market and inflation risks

Post-Close | MSFT, META, GOOGL earnings: AI growth, capex, ad revenues in focus

Pre-summit (Thursday): Progress on U.S.-China trade deal with possible tariff relief announcement

ADP Employment Report: Labor market softening, private payrolls weak; consumer confidence slips

TECHNICAL PICTURE

S&P 500: Bullish alignment in all major moving averages; resistance at 7,075, support 6,870–6,850. Oscillators (RSI 68.97, MACD bullish) show momentum, but short-term overbought risk present.

Options: Elevated call volume at 7,000 strike; watch for post-FOMC volatility compression.

Sector Rotation: Leadership broadening out, tech (+22.6% YTD), financials strong, consumer staples underperform.

STOCKS TO WATCH

Nvidia (NVDA): Hits $5T market cap; CEO confirms $500B+ AI revenue pipeline. Target $600+, buy dips to $490–500.

Microsoft (MSFT): Earnings after close; focus on Azure, AI capex, OpenAI tie-ins.

Alphabet (GOOGL): Watch AI revenue, YouTube and Cloud, Gemini rollout.

Meta (META): Advertising growth, AI capex, Reality Labs.

CrowdStrike (CRWD): Upgraded, breakout move; $650 target.

Constellation Energy (CEG): Wells Fargo initiates overweight, $478 target – nuclear/AI data center play.

Nokia (NOK): Nvidia AI partnership, Jefferies upgrade.

MACRO RISKS

Government Shutdown: Data blackout limits Fed’s visibility; delays employment stats and inflation analysis.

AI Bubble Warnings: Capex acceleration scrutinized for sustainability.

Geopolicy: U.S.-China, Middle East, Taiwan tensions.

Valuation Risk: S&P forward P/E near 28x.

ACTIONABLE STRATEGY

Equity Focus: Stay overweight tech, selectively add AI infrastructure names, financials, and small-caps.

Options: Hedge with SPX puts (6,700 strike), VIX call spreads.

Rebalancing: Trim extended winners, add laggards, especially energy, utilities, financials if pullback.

SUMMARY

Today’s market hinges on the Fed decision and Powell’s guidance, which will set the pace for the rest of Q4. Big Tech earnings and the U.S.-China summit provide extra momentum and risk. Stay nimble with hedges, watch technical levels.

PORTFOLIO RISK ASSESSMENT: