Market Brief + Model Portfolio Risk Assessment

10/31/25

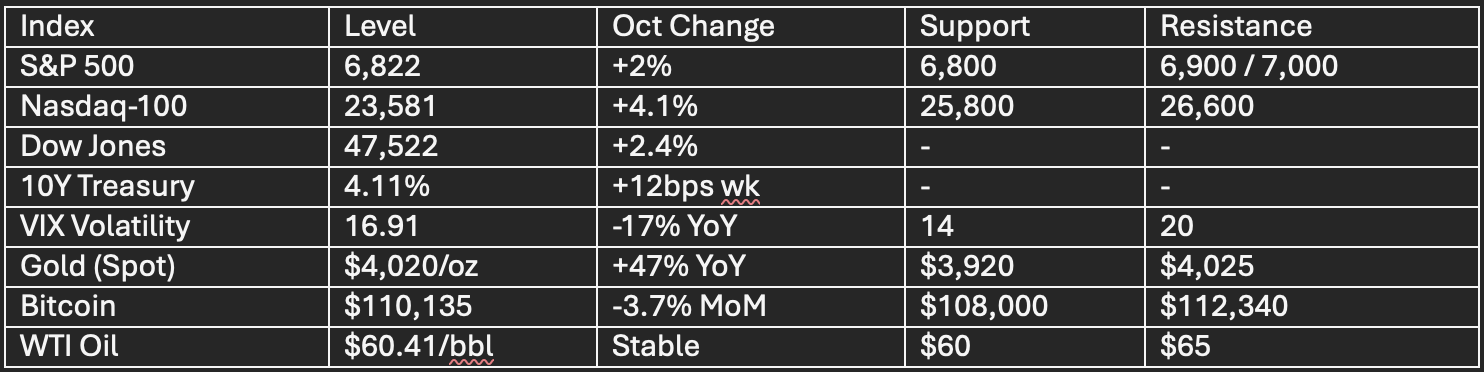

Market Brief Tear Sheet

Date: October 31, 2025

Market Overview

Equities:

S&P 500 futures +0.63%; Nasdaq 100 futures +1.14%; Dow futures marginally positive.

Week-to-date: S&P 500 up 0.45%, Nasdaq up 1.6%, Dow up 0.7%. October marks the Dow’s sixth straight monthly advance.

VIX volatility index at 16.91, lowest in months, risk-on sentiment remains elevated.

Macro & Fed:

Fed Funds Rate: 3.75–4.00% after 25bps cut this week. December cut odds drop to 68% on Powell’s “no foregone conclusion” remarks.

Data blackout persists with shutdown; November jobs report is key event.

U.S.–China trade truce: One-year agreement, limited tariff reductions, rare earth export controls paused.

Earnings Pulse:

83% of S&P 500 companies beat Q3 earnings estimates; 12.5% aggregate YoY EPS growth.

Apple (AAPL): Q4 rev $102.5B (up 8% YoY). Best holiday guidance on record.

Amazon (AMZN): Q3 rev $180.2B (up 20% YoY AWS), beat across all key lines. Pre-market: both AAPL +3%, AMZN +13%.

Meta, Microsoft: Investors rotate out due to AI capex surge, realized losses.

Key Market Data

Sector Heatmap (October 2025)

Breadth: Only 42% of S&P 500 stocks above 50-day MA, leadership remains narrow; momentum concentrated in mega caps and select cyclicals.

Strategic Trade Ideas

Bank of America (BAC): Technical breakout, higher-for-longer rates creating margin expansion. Target $58–60; stop $51.50.

Comfort Systems (FIX): Data center/build-out play, Zacks #1 momentum, +42% past 3 months; target 15–20% upside.

Corning (GLW): Advanced tech glass with strong sector tailwinds, accumulate on pullbacks.

Seagate (STX): AI-driven data storage; technical breakout, 20–25% upside potential.

Exxon Mobil (XOM): Oversold, value in energy sector; accumulate on support, watch for OPEC headlines.

Risk Factors & Macro Catalysts

Valuation Stretch: S&P 500 trades at 23x forward earnings.

Market Breadth: Narrow leadership, watch for rotation or correction.

Fed Uncertainty: December policy pivot now conditional; jobs report Friday is linchpin.

Geopolitics: Trade truce is temporary; Middle East risks remain.

Rates: 10Y yield climbing post-Fed, challenging high-multiple stocks.

Outlook: Base case assumes S&P consolidates in the 6,700–6,900 band, with jobs report as week’s swing factor. Momentum stocks, banks, and select defensives hold best risk-reward heading into November. Hedge with VIX calls, hold cash for tactical buys on volatility spikes.

MODEL PORTFOLIO RISK ASSESSMENT

21-day parametric VaR, % on NAV