Market Brief + Model Portfolio Risk Assessment

11/12/25

SEQH Capital Partners Morning Market Tear Sheet

November 12, 2025 – Pre-Opening Summary

Market Overview

S&P 500 Futures: +0.55%

Dow Jones Industrial Average Futures: Flat to slightly positive

Nasdaq Futures: Modest rise

VIX (Volatility Index): -2.5%, signaling short-term market stability

European Equities (STOXX 600): +0.65%

Asia Session: Nikkei 225 +0.43%; CSI 300 -0.13%

Bitcoin: Slightly positive, trading near $105k.

Macro & Political Drivers

Consensus is strengthening for a near-term end to the U.S. government shutdown as critical votes take place in the House today, supporting risk-on sentiment across global markets.

Lingering uncertainty over a December Fed rate cut as recent U.S. labor market data showed weakness, but inflation remains sticky and policymakers signal hawkish leanings.

European stocks reach new highs, led by financials, reflecting relief around U.S. fiscal impasse and stable macro signals.

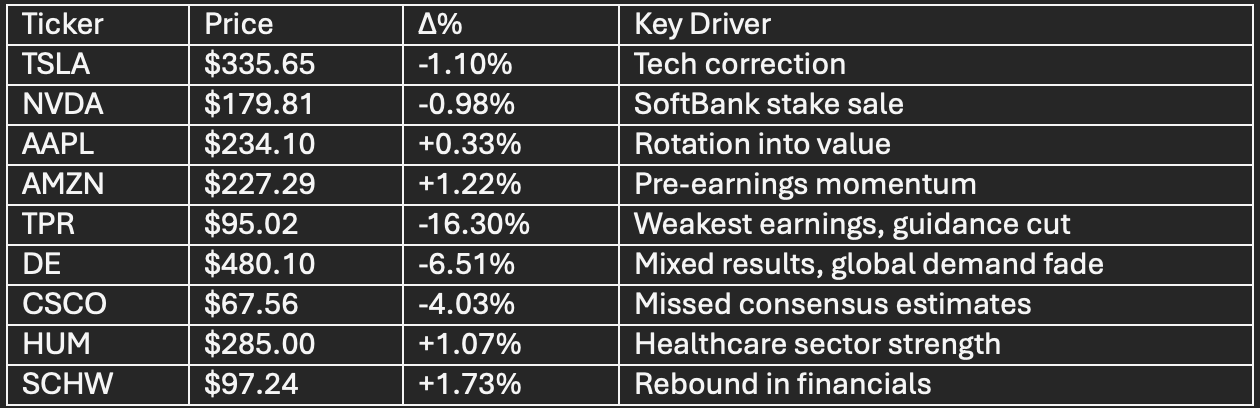

Pre-Market Movers (US Equities)

Sector Rotation

Following recent technology sector volatility, capital flows are favoring lower-valuation sectors and defensive stocks, with financials and select healthcare showing relative strength.

Nvidia fell approximately 3% as SoftBank divested its entire position in the company, weighing on chip sector performance.

Commodities

Oil: Pullback of ~1% after a three-day rally, driven by oversupply concerns and OPEC demand expectations.

Gold: Flat ahead of inflation data and Fed commentary.

Macro Calendar

Key Earnings Today

Major reports expected from Applied Materials (AMAT), Deere & Company (DE), Tapestry (TPR), Amcor (AMCR), and Cisco Systems (CSCO).

Deere beat on EPS but outlook remains cautious; Tapestry sharply missed and cut guidance, impacting discretionary sector sentiment.

Analyst Commentary

Momentum remains the dominant factor in price action, amid a pervasive willingness by investors to maintain positions that have performed well throughout 2025. Rotations are visible but prudent asset allocation favors U.S. financials and large-cap value, while elevated volatility persists in high-growth technology and cyclical sectors.

Critical Watchlist

Vote on U.S. government funding in the House (shutdown resolution)

Fed communications regarding the December rate decision

Key corporate earnings: AMAT, DE, CSCO, TPR

Oil/OPEC supply outlook; tech sector recovery; rotation signals

MODEL PORTFOLIO PRE-MARKET RISK ASSESSMENT BELOW: