Market Brief + Model Portfolio Risk Assessment

11/7/25

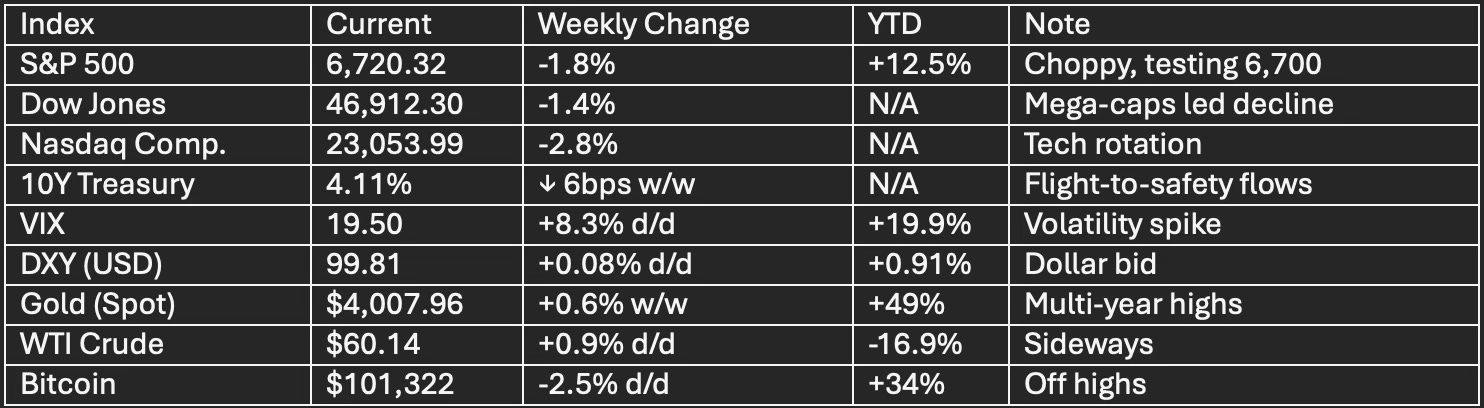

Market Tear Sheet

Date: November 7, 2025

Week in Review & Analytical Outlook

Key Market Metrics

Macro & Market Overview

Indices: Broad selloff led by tech; Nasdaq -2.8% on the week. S&P 500 trades below key moving averages, breadth remains weak (only 37.8% above 20-day MA).

Earnings: Mixed season; Qualcomm, Super Micro, and ARM beat expectations but guidance unimpressive. Airbnb jumps on growth surprise.

Jobs: October layoffs +65% YoY; highest for October since 2003. Tech and retail see steep cuts; AI/cost cutting drive outsized risk.

Fed Policy: Rate cut in October (now 3.75–4.00% target). December cut likely (72% probability); dissent grows over inflation vs. employment.

Government Shutdown: 37 days and counting; GDP hit estimated at -1.1pp for Q4. Data calendar remains severely delayed, adding risk premium.

China: Exports -1.1% YoY, U.S. shipments -25% YoY. Global trade headwinds persist; market reaction muted but risk remains elevated.

Commodity Sector: Gold surges to multi-year highs on risk aversion. Oil sideways despite war premium; energy equities outperform crude.

Market Concentration: Rally narrow, Mega-cap tech dominates, 69.3% of stocks declined yesterday.

Featured Stock Idea

Caterpillar (CAT)

Rationale: Upgraded to “Buy” by HSBC, $660 PT (prev. $405).

Drivers: Infrastructure, AI datacenter build, dividend stability.

Technical: Near 20+% discount vs. October highs; support at $610.

Framework: Defensive rotation into quality, leverages AI trend with cyclical upside.

Technical Moves & Sector Leadership

Tech/Semis:

Nvidia (NVDA): ↓4% Thursday; AI bubble narrative intensifies.

AMD: ↓7.3%; chip launches, long runway, valuation reset.

Qualcomm: ↓4% post-earnings; positive long-term on 5G, AI accelerators.

Financials:

JPMorgan, Citi, Wells outperform peers; banks buoyed by rate stability, strong credit quality.

Energy:

EQT Corp. +55% YoY; Valero +32%; Marathon +29%.

Tactical Picks:

Applied Materials (AMAT) – capex cycle restart, oversold.

Energy Sector ETF (XLE) – relative strength play.

US Bancorp (USB) – undervalued, 6.87% yield.

GDX (Gold Miners) – hedge, safe haven bid.

Market Breadth & Sentiment

Breadth: 29.4% above 20-day MA; risk of momentum break persists.

Advancers/Decliners: 28.5%/69.3%, recent selloff broad-based.

Volatility: VIX risk above 20 signals defensive posture; watch for panic sell triggers.

Sentiment: Institutional cash levels rising; retail flows slow but steady.

Event Risk | Key Catalysts Ahead

Fed Speak: FOMC rhetoric on December cut, inflation risks.

Earnings: Nvidia (mid-November), potential market turning point.

Gov’t Data: Awaiting CPI, PPI; shutdown resolution could shift outlook.

Strategic Risk Management

Tighten risk controls, preserve cash for tactical entry.

Prioritize high-quality, dividend growth names for exposure.

Avoid chasing extended high-beta tech; rotate into defensive leaders.

VIX >22 signals buy zone for disciplined accumulation.

Prepared for SEQH Capital Partners Research | Confidential

MODEL PORTFOLIO RISK ASSESSMENT