Market Recap

11/4/25

U.S. & Global Market Tear Sheet

Trading Date: November 4, 2025

Market Overview

Equity Indices:

S&P 500: 6,771.55 (▼1.17%)

Nasdaq Composite: 23,834.72 (▼2.04%)

Dow Jones Industrial: 47,085.24 (▼0.53%)

SOX Semiconductor Index: 7,270.97 (▼4.01%)

Summary:

U.S. equities endured a pronounced risk-off session as elevated AI sector valuations fueled a broad selloff. Large-cap Technology and Semiconductor shares led declines, coinciding with deteriorating breadth and hawkish commentary from the Federal Reserve. The S&P 500 marked its worst day since October 10, with only 39% of stocks advancing and new lows outpacing highs for the third time in four sessions.

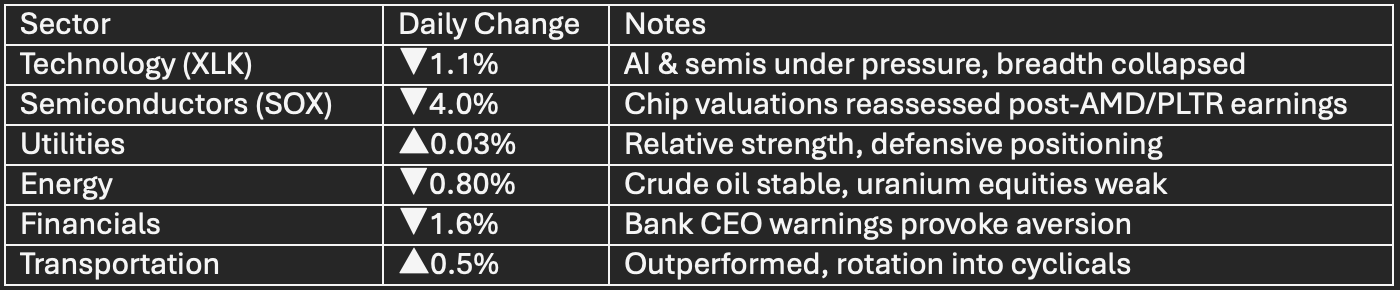

Sector Performance

Breadth:

S&P 500 advancers: 38.6%

Decliners: 58.8%

Stocks above 200DMA: 57.5% (near five-week lows)

Featured Corporate & Macro Developments

Earnings Highlights:

Palantir (PLTR): Delivered Q3 revenue $1.181B (+63% YoY), adj EPS $0.21; stock collapsed 9% on valuation concerns.

AMD: Q3 rev $9.25B (beat), adj EPS $1.20, Q4 guide $9.6B; shares fell on slowing data center growth despite strong guidance, major OpenAI / Oracle wins.

Uber: Revenue $13.47B (+20% YoY), record bookings, stock -5% after $479M legal drag hit income.

Spotify (SPOT): Premium users +12% to 281M, MAUs hit 713M, Q3 revenue €4.27B, operating income €582M. Mixed 4Q guidance pressured shares.

Fed & Yields:

10Y Treasury: 4.090% (▼1.6bp), as December rate cut odds faded to ~72% vs 90%.

Fed Chair Powell: “Rate cut not assured.”

Hawkish tone triggered defensive sector bid, dollar breakout to 6-month highs.

Commodities & FX

Macro Context:

China ended VAT offset for gold retail, major jewelry retailer stocks sank 8–12%.

Euro at 3-month lows, yen firmer as Japan signaled intervention.

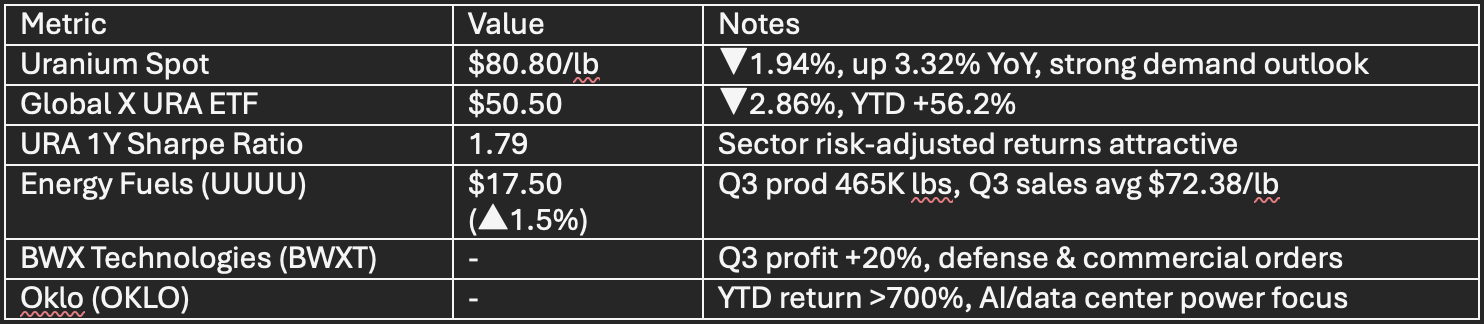

Nuclear & Uranium Market Intelligence

Fundamentals:

WNA projects nuclear uranium demand +28% by 2030.

Constellation Energy commits 5.8GW new gen/battery capacity in MD.

Cryptocurrency Market

Technical & Breadth Analytics

S&P 500 sits 1.73% below record October 28 close.

Market leadership narrowing: “Magnificent Seven” now sole drivers; equal-weight S&P at weakest breadth since 2003.

Fewer than 40% of S&P 500 stocks above 20DMA, strongest signals of a possible breadth-driven correction(see chart).

SEQH Capital Partners Outlook

Investment Implications:

AI/Tech valuations at inflection point, risks rising despite healthy earnings.

Favor quality, secular nuclear and uranium growth exposure versus cyclical high-multiple tech.

Position tactically amid breadth deterioration and Fed uncertainty.

Near-term upside rests on breadth stabilization and Fed signaling; downside risks elevated.