MARKET RECAP 10/10/25

Markets endured a sharp, broad-based selloff on Friday, October 10, 2025, with major U.S. indices plunging as President Trump escalated tariff threats against China in response to a new wave of rare earths export controls from Beijing. The downturn reverberated across risk assets, including equities, metals, and crypto, while defensives and select sectors managed relative outperformance.

Index Performance & Macro Highlights

The S&P 500 dropped 2.7%, the steepest fall in six months, and the Nasdaq plunged nearly 3.5%, led by a dramatic selloff in big tech and semiconductor stocks.

The Dow fell 1.88%, with just a handful of defensive names ending higher.

Market volatility spiked as President Trump announced imminent 100% tariffs on Chinese imports and signaled further escalation if rare earths access remained restricted.

U.S. oil prices slid over 4%, settling below $59/barrel, exacerbating investor worries about demand and margins in the energy sector.

Consumer sentiment data was stable but still significantly below levels seen a year ago, reflecting persistent concerns over inflation and jobs.

Chia Tariff & China Trade News

Friday’s sudden escalation stemmed from China’s export ban on rare earths, a direct hit to global tech, defense, and metals markets.

In retaliation, President Trump announced a planned 100% tariff on Chinese imports effective November 1. Markets recoiled at the implications for global growth, risk premiums, and supply chain stability.

Rare earth and EV names were among the hardest hit, though U.S.-centric metals producers and some defensive consumer names held up better.

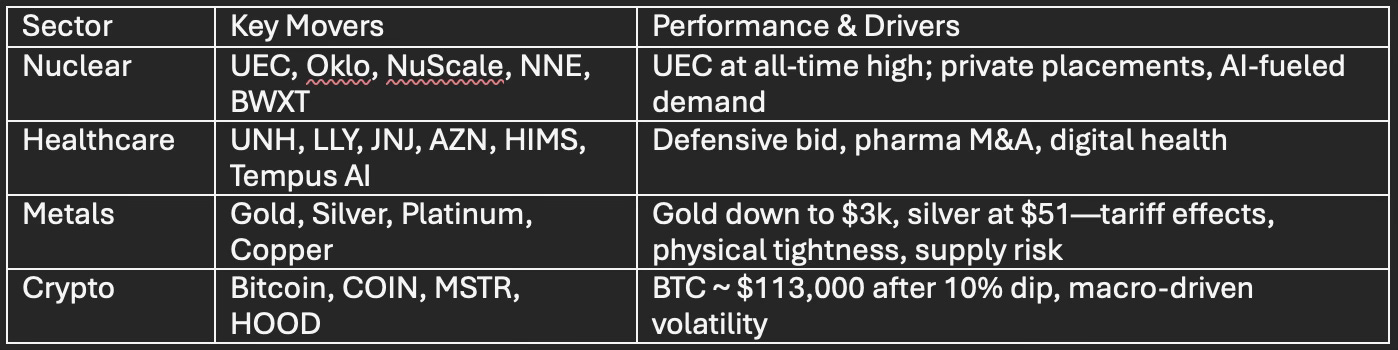

Nuclear Sector Highlights

Nuclear energy maintained strong momentum amid the global fuel security narrative. Uranium Energy Corp surged to an all-time high of $15.17, capping a 118% rise over the past year, driven by renewed interest in domestic uranium supply and AI-driven energy demand.

Notable nuclear stocks in focus included Oklo, NuScale Power, Centrus Energy, Nano Nuclear Energy (NNE), and BWX Technologies, all seeing heavy trading as the sector benefits from a renaissance in nuclear as a clean baseload source.

Nano Nuclear Energy completed a $400M private placement to fund its microreactor development, boosting its cash reserves for future growth.

Terra Innovatum, a new SPAC in micro-reactors, debuted with volatile trading, highlighting the speculative enthusiasm and risks in the next-gen nuclear space.

Healthcare and Pharma Developments

Healthcare remained relatively defensive, with stocks like UnitedHealth, Eli Lilly, Johnson & Johnson, and AstraZeneca attracting high trading volumes.

Pharma sector focus was on potential M&A, particularly after recent Pfizer moves. Eli Lilly and AstraZeneca stood out for both price action and industry speculation.

Digital health and precision medicine plays, including Tempus AI and Intuitive Surgical, also featured amid shifts in sector leadership.

Metals and Precious Commodities

Precious metals saw extreme divergence: Gold retreated sharply from a record $4,000/oz to around $3,004 as safe-haven flows adjusted to clarifications on tariff exemptions for some bullion imports.

Silver, by contrast, rocketed to $51.30/oz, its highest in over 40 years—bolstered by robust industrial demand from green tech and acute physical shortages, evidenced by backwardation and record Comex lease rates.

Base metals like copper faced fresh selling as a new 50% U.S. tariff on copper imports was proposed, aggravating price volatility and supply anxiety heading into LME week.

Bitcoin & Crypto Market Action

Crypto markets tumbled in tandem with equities. Bitcoin dropped as low as $108,000 before rebounding to the $113,000 range, reflecting a 3-10% intraday swing on extreme tariff risk-off sentiment.

Forecasts remain mixed, models suggest a 50% probability of BTC reclaiming $140,000+ by month-end, but short-term volatility is expected to persist as macro headwinds dominate price discovery.

Crypto-related equities (COIN, MSTR, HOOD) also fell sharply as global cross-asset correlations spiked.

Advanced Sector Tables

Closing Perspective

Today’s trade redefined near-term volatility expectations, with global markets rattled by renewed geopolitical risk and supply chain strain. Market leadership remains in flux, defensive themes retain relative strength, and sectors exposed to trade and tariff headlines (tech, metals, crypto) are set for continued volatility. The nuclear theme is increasingly salient as strategic supply takes precedence in policy, while precious metals realignment signals further reallocation among institutional investors.