MARKET RECAP 10/16/25

SEQH Capital Partners Research: Market Recap - October 16, 2025

Main Takeaway

October 16, 2025 was marked by exceptional market volatility, with investors rotating into safe-haven assets, record highs in precious metals, and sector-specific dynamics driven by evolving macro, policy, and liquidity conditions. The nuclear energy, healthcare, metals, and crypto segments all delivered significant developments, making today a pivotal session for sector rotation and advanced portfolio positioning.

Broad Market Performance

Major US indices experienced turbulent swings, with benchmark averages reversing early gains and ending mostly lower as credit fears resurfaced and regional banks reported new loan losses. Tech stocks initially rallied on AI optimism and strong semiconductor earnings before sentiment soured:

S&P 500: closed at 6,622.09, down 41.99 points (~0.63%). Seven out of eleven sectors finished in the green, led by Real Estate, Utilities, and Technology (XLK +1%).

Dow Jones: dropped 301.07 points to 45,913.16 (-0.65%).

Nasdaq Composite: closed at 24,641.06, down 88.12 points (-0.36%) despite initial strength in AI-driven stocks.

Across the board, market volatility was elevated, with the VIX rising 4.67% to 25.31. Safe-haven demand fueled a rally in bonds (10-year Treasury yield fell below 4%) and precious metals, emphasizing a defensive tone.

US-China trade tensions and a continued government shutdown dominated the macro narrative, depriving markets of new economic data and stoking risk-off sentiment.

Nuclear Sector: Explosive Upside and Structural Shifts

Nuclear equities remained the hottest energy subsector, far outperforming broader markets:

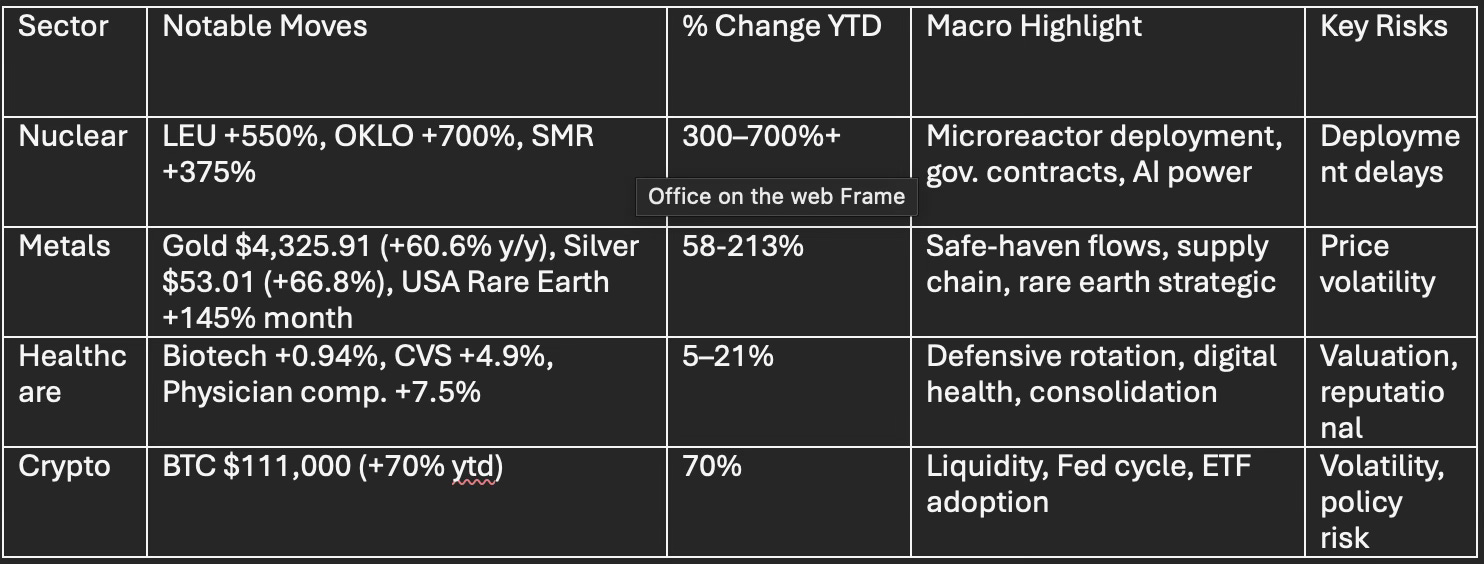

Centrus Energy (LEU): surged over 550% YTD on the Trump administration’s explicit support for expedited nuclear reactor development and HALEU fuel production, cementing its role in next-generation nuclear.

Oklo Inc. (OKLO): soared more than 700% YTD; the company’s microreactor platform gained remarkable momentum with new deployment initiatives targeting data centers and military use.

NuScale Power (SMR): rocketed higher after landmark deployment deals, including a historic TVA contract, and NRC design approval. NuScale stock is up 223% over the past year, +375% from its April lows, signaling a nuclear renaissance backed by real contracts.

Government Policy: The new White House directive fast-tracks advanced microreactor rollouts for defense, propelling the sector’s growth prospects and investor confidence.

Market Context: Investor enthusiasm is underlined by record trading volumes and a surge in advanced nuclear stocks held by institutional portfolios. However, deployment timelines and revenue realization for new reactors remain key risks.

Metals: Precious and Strategic Materials at Record Highs

Gold & Silver

Gold: hit a historic record, trading as high as $4,325.91/oz (up 2.78% daily, +18.19% monthly, +60.59% y/y). The macro catalyst is a flight to safety, dovish Fed rate cut expectations, persistent US-China tension, and a weakening US Dollar. Central banks accelerated gold reserve accumulation, echoing a move away from dollar dominance. Miners like Barrick Gold and Newmont poised for outsized earnings.

Silver: continued its dramatic run, up to $53.01/oz (+27% monthly, +66% y/y). Silver’s YTD performance outpaced gold, largely on industrial and monetary demand.

Industrial & Rare Metals

Copper: moderately up at $4.92/lb (+7.93% monthly, +14.59% y/y).

Platinum: rallied to $1,677.80/oz (+22.3% monthly, +68.6% y/y).

Rare Earths:

USA Rare Earth surged 145% over the past month, +213% y/y, extolled for its strategic role in US supply chain resilience.

Ramaco Resources (METC) jumped 8.58% amid new rare earth discoveries tied to defensive and EV sector demand, with analysts hiking price targets sharply.

Shanghai Metals Market: Battery-grade rare earths (Neodymium, Praseodymium, Cerium, etc.) generally held steady or rose slightly; Neodymium and Pr-Nd alloys declined marginally.

Healthcare Sector: Defensive Outperformance and Compensation Surges

Market Cap: $5.9 trillion, Revenue $3.1 trillion, Earnings $140.4 billion; PE ratios elevated at 24.5x for the sector.

Performance: Healthcare (-1.14%) lagged defensives, with Biotech (+0.94%) and Life Sciences (-0.81%) outperforming high-cost Healthtech (-5.02%) and Medical Equipment (-2.08%).

Major Stocks: CVS Health (+4.9%), McKesson (+4.8%), Johnson & Johnson (+0.8%), Alnylam Pharma (+4.3%).

Fundamentals: Physician compensation hit decade highs on supply-demand imbalances—medical specialties rose 7.5% y/y, primary care +21.8% since 2020.

Volume/Innovation: The sector is experiencing consolidation, M&A rebound, and an accelerated pivot toward AI-powered digital health and genomics.

Risk Factors: Despite earnings growth, traditional valuation and reputation concerns persist, Gallup polls, for example, show only 44% public confidence in healthcare quality.

Crypto: Bitcoin Consolidates, Macro Liquidity Emerges as New Driver

BTC Price: After correcting 2.7% intraday, Bitcoin stabilized at ~$111,000, consolidating above the crucial $102,000 support; volatility mirrors wider market risk-off moves.

Despite the day’s drop, Bitcoin remains up 70% YTD, supported by ETF inflows and institutional adoption. The four-year halving cycle narrative is losing traction, with macro liquidity and Fed policy now seen as key price drivers.

Outlook: Analysts expect further gains if the Fed continues monetary easing, with 2026 eyed as a potential new peak for BTC outside classic cycle models.

Advanced Data Table: Key Sector Stats - October 16, 2025

Conclusion

Today’s trading session crystallized a sectoral rotation into hard assets and defensive industries, driven by monetary easing expectations, trade/policy uncertainty, and structural supply-chain changes. Nuclear energy stocks are the undisputed leaders of the clean energy space, metals posted historic advances, healthcare remains a key defensive allocation, and Bitcoin’s price action increasingly reflects global liquidity themes. Investors should remain nimble and monitor cross-asset volatility and macro policy for actionable signals.