Market Recap 10/24/25

Market Tear Sheet | October 24, 2025

MARKET SNAPSHOT: RECORD HIGHS ON COOLING INFLATION

CPI DATA DRIVES RALLY | September CPI: 3.0% YoY (exp: 3.1%) | Core CPI: 3.0% YoY | MoM: +0.3% (exp: 0.4%)

FED OUTLOOK | 99% probability 25 bps cut Oct 29 | Current: 4.00-4.25% | Path: Additional 2 cuts by Mar 2026

MARKET BREADTH | Advancers/Decliners: 2.05:1 (NYSE), 1.86:1 (Nasdaq) | Volume: 19.1B shares | 9 of 11 sectors green

MAJOR INDICES PERFORMANCE

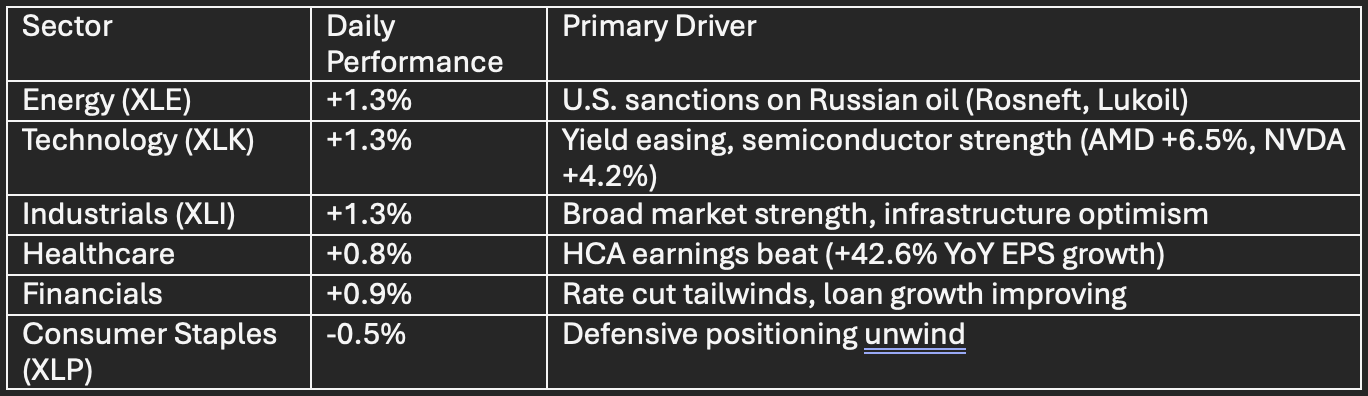

SECTOR ROTATION

FIXED INCOME & VOLATILITY

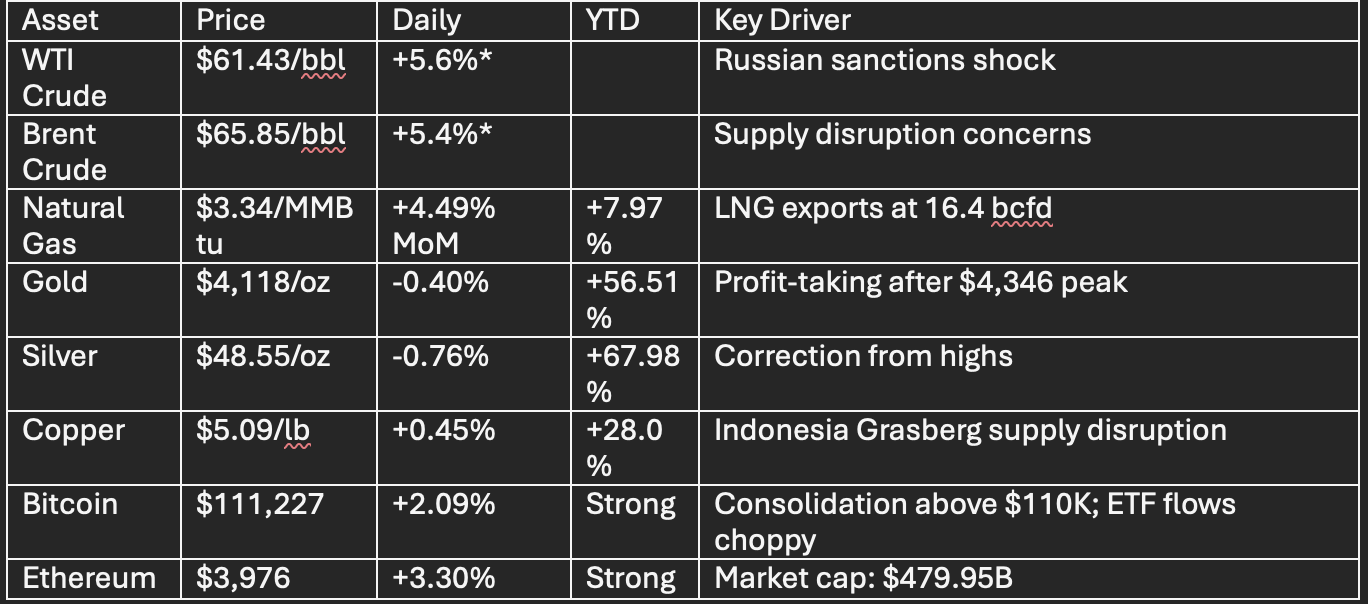

COMMODITIES & DIGITAL ASSETS

*Weekly gain from Thursday session

Crypto Market Cap: $3.72T | BTC Dominance: 59.65% | 24H Volume: $401.14B

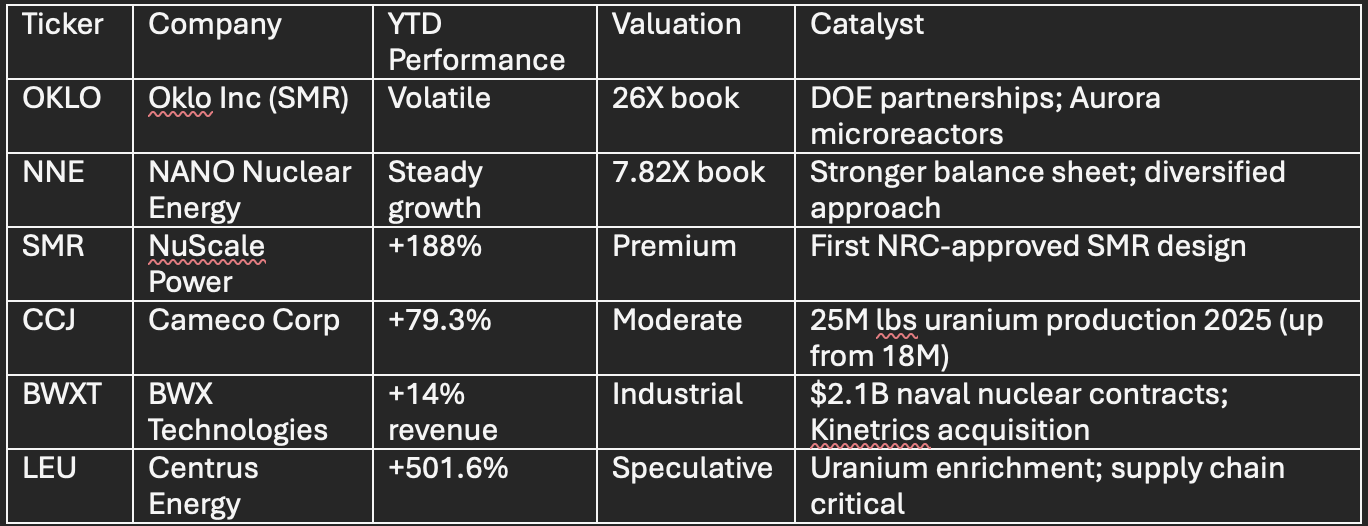

NUCLEAR ENERGY SECTOR: AI INFRASTRUCTURE DEMAND

Uranium Spot: $76.50/lb (+4.79% YTD) | Demand Outlook: +28% through 2030, +51% next decade

Thesis: AI data center electricity requirements driving nuclear renaissance; prefer established producers + uranium miners

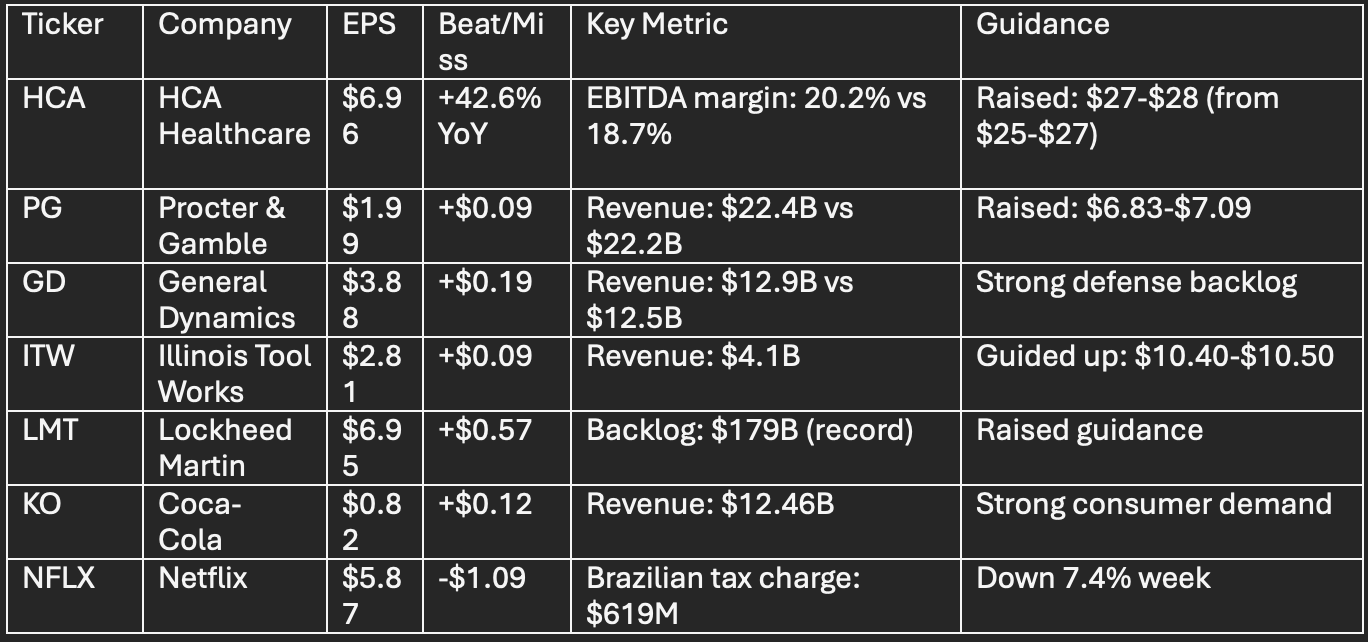

EARNINGS HIGHLIGHTS

Earnings Season: 9 of 11 sectors beating; margin expansion key theme; consumer resilience despite inflation

TOP STOCK MOVERS

GAINERS

• AMD +6.5% | Semiconductor strength; AI chip demand

• NVDA +4.2% | GPU leadership; data center momentum

• INTC +3.8% | Earnings optimism; turnaround narrative

• AAPL +2.6% | Approaching $4T market cap; iPhone 17 sales

• MSFT +2.4% | Azure cloud revenue growth

DECLINERS

• BA -2.1% | Production challenges persist

• XOM -1.8% | Energy sector lag despite oil surge

• CVX -1.6% | Refining margin pressure

GEOPOLITICAL & POLICY CATALYSTS

TRUMP-XI MEETING | Confirmed for next week during Asia trip; trade de-escalation signal; markets positive

RUSSIAN OIL SANCTIONS | U.S. targets Rosneft, Lukoil; crude +5.6%; reshapes global supply

GOVERNMENT SHUTDOWN | Ongoing; delayed CPI by 9 days; BLS reports suspended; data visibility limited

CANADA TRADE | Trump halts talks; CAD weakens

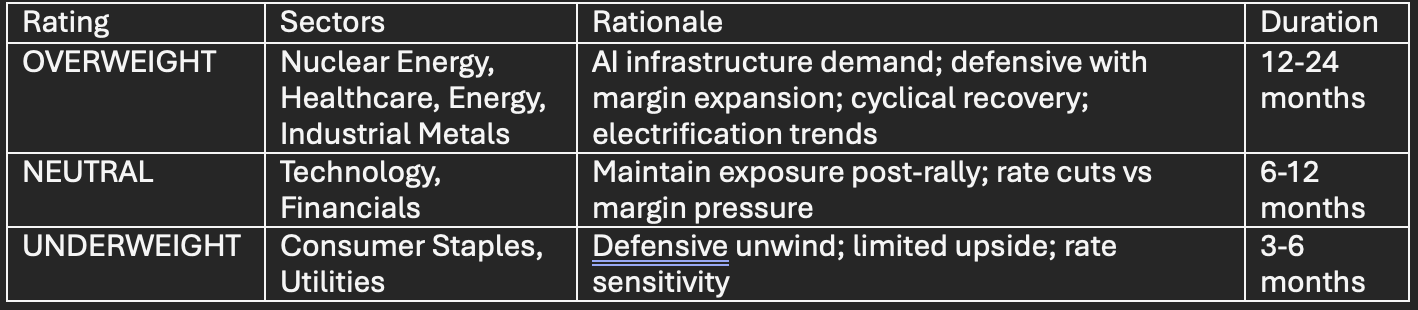

SECTOR ALLOCATION MATRIX

RISK FACTORS

IMMEDIATE (0-3 months)

❶ Fed policy error (insufficient or excessive cuts)

❷ Valuation multiples (S&P 500 P/E: 27.88 vs historical norms)

❸ Government shutdown extension (data blackout, fiscal dysfunction)

NEAR-TERM (3-6 months)

❹ Geopolitical escalation (Ukraine, Middle East, Taiwan)

❺ Recession indicators (yield curve, employment weakening)

❻ Tech sector earnings disappointment

STRUCTURAL (6-12 months)

❼ Inflation persistence above 2% target

❽ Energy supply volatility from sanctions

❾ Debt ceiling crisis

INVESTMENT STRATEGY

TACTICAL POSITIONING

• Precious Metals: Accumulate gold near $4,100 support for long-term hedges; correction is healthy profit-taking

• Bitcoin/Crypto: Maintain 2-5% allocation; consolidation above $110K validates institutional support

• Nuclear: Favor CCJ, BWXT over speculative SMRs (OKLO, NNE) due to valuation; LEU high-risk/high-reward

• Energy: Prefer integrated majors and refiners (PARR 10.4X forward P/E) over E&P; cyclical recovery early stage

PORTFOLIO CONSTRUCTION

• Diversification: Spread across nuclear (structural), healthcare (defensive), energy (cyclical), industrial metals (secular)

• Dry Powder: Maintain 10-15% cash for volatility; VIX at 16.36 suggests complacency

• Rebalancing: Trim mega-cap tech winners (NVDA, AMD, AAPL) into strength; rotate to undervalued sectors

MACRO THESIS

Markets entering late-cycle expansion with Fed easing support. Cooling inflation validates soft landing, but 3.0% CPI remains elevated. Record highs on strong breadth suggest bull market continuation, though valuation discipline essential. Nuclear energy and industrial metals offer best risk-adjusted structural growth; healthcare provides ballast.

KEY METRICS SUMMARY

BOTTOM LINE: October 24 delivered textbook risk-on behavior: record highs, VIX compression, dollar weakness, and sector breadth. Cooling inflation cements Fed easing path, but 3% CPI and 27.88 P/E demand selectivity. Nuclear energy’s AI-driven structural demand, healthcare’s defensive growth, and energy’s cyclical recovery offer best opportunities. Maintain diversification, preserve cash, and favor quality over momentum.

SEQH Capital Partners Research | Investment Analysis Division

Report Date: October 24, 2025, 6:15 PM EDT