Market Recap 10/29/25

SEQH Capital Partners Research: October 29, 2025 Tear Sheet

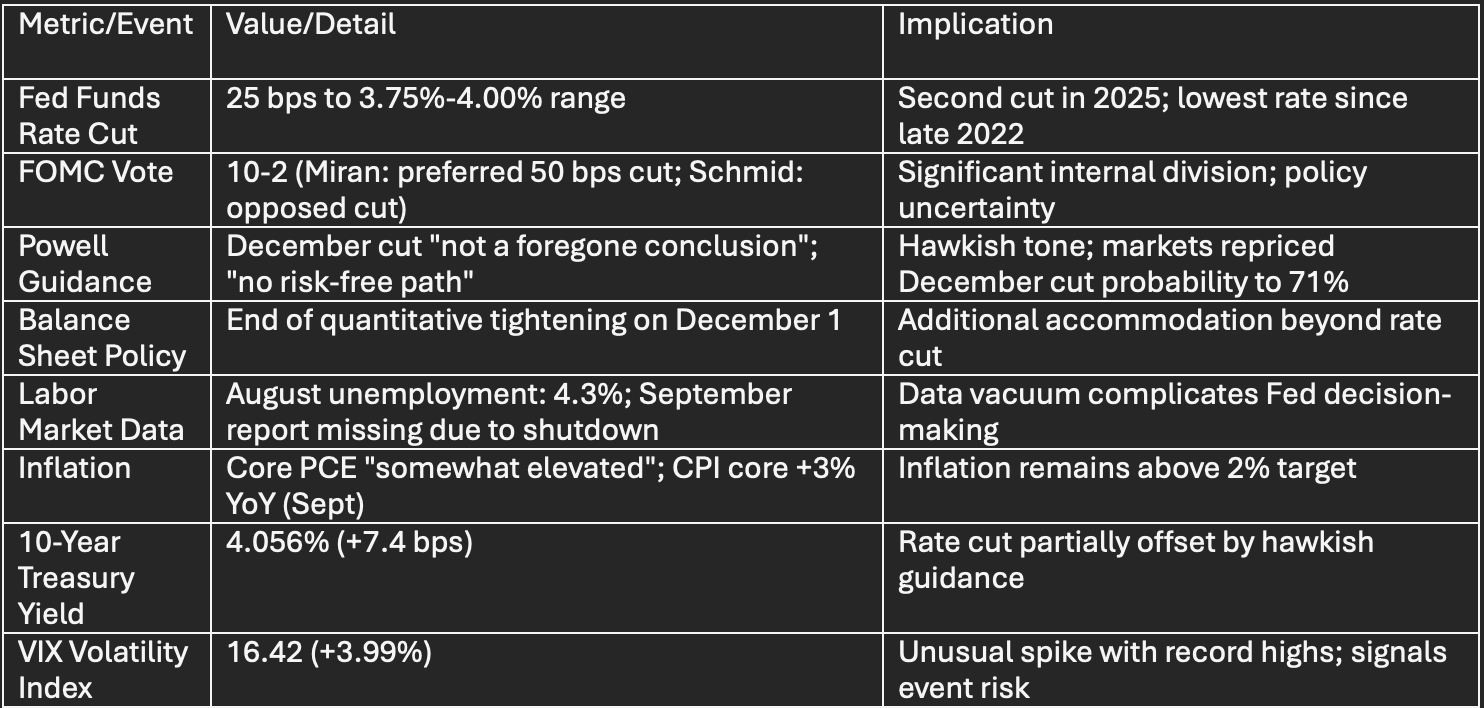

Federal Reserve Policy Shift: Key Data

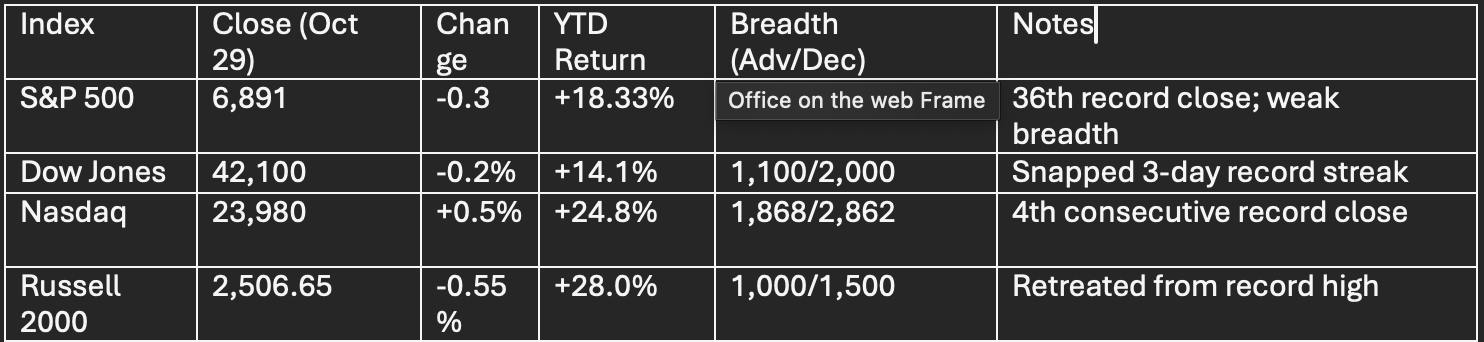

Market Performance: Key Indices & Breadth

Breadth Warning: Decliners outnumbered advancers on both NYSE and Nasdaq despite record highs, signaling concentration risk.

Nuclear & Uranium Sector: Catalysts & Performance

Catalysts:

$80B U.S. government partnership with Westinghouse (Cameco/Brookfield)

AI data center power demand driving nuclear adoption

Supply constraints: Cameco cuts 2025 production, Kazatomprom down 10%

World Nuclear Association forecasts 28% demand growth by 2030

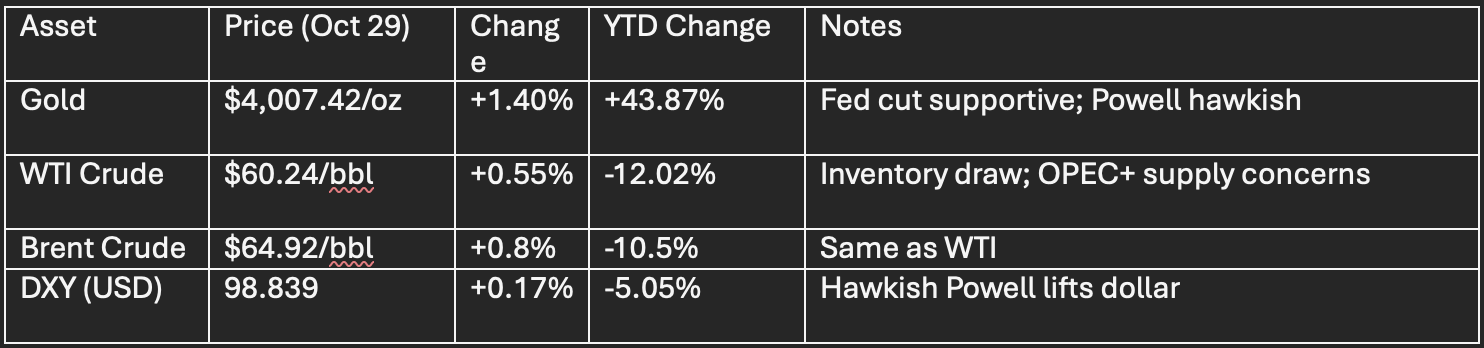

Commodities & Currency

Geopolitical & Policy

Investment Strategy: Key Takeaways

Nuclear/Uranium: $80B government deal is transformational; Cameco and uranium miners offer asymmetric upside. Maintain 3-5% sector allocation.

Magnificent Seven: Concentration risk elevated; hedge with puts or rotate into defensive sectors if earnings disappoint.

Market Breadth: Poor breadth warns of correction; avoid chasing new capital into S&P 500 at record highs.

Fed Policy: December cut not guaranteed; prepare for slower easing cycle and higher terminal rate (3.50-3.75%).

Commodities: Gold remains attractive hedge; oil pressured by supply concerns.

SEQH Capital Partners Research

October 29, 2025 | 6:15 PM EDT