Market Recap 10/31/25

Final Recap for October

INTERNAL MARKET TEARSHEET

October 31, 2025 | End-of-Day Close

EXECUTIVE SUMMARY

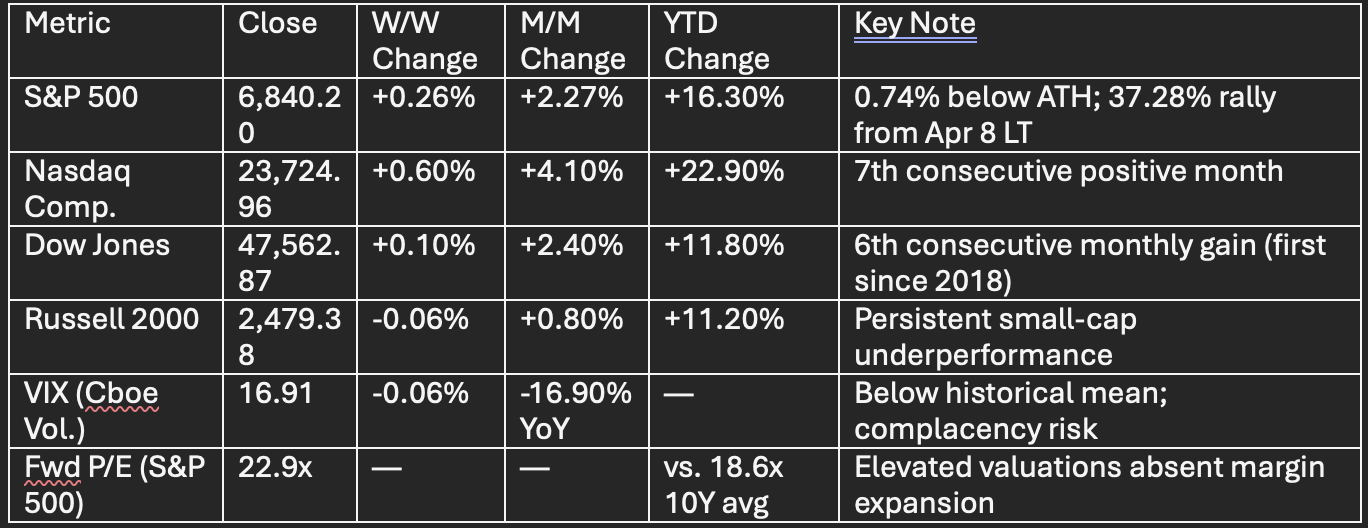

The U.S. equity complex closed Friday with modest gains, concluding an exceptionally strong month marked by divergent mega-cap performance and a hawkish Fed policy pivot. The S&P 500 (6,840.20, +0.26%) achieved its sixth consecutive monthly advance, the longest streak since mid-2021, while the Nasdaq (+0.60%) extended its seven-month winning streak. However, Powell’s October 29 commentary that a December rate cut is “far from” guaranteed reframed market expectations, with CME FedWatch odds for December easing collapsing from ~90% to 56-67% in 48 hours. Critically, Q3 earnings beat rates reached 83% with +10.7% blended growth, potentially the strongest on record, yet Amazon (+9.6%) was alone in sustained institutional enthusiasm while Meta (-11%) and Microsoft (-5.7% over two sessions) faced renewed scrutiny on AI capex ROI trajectories. The most significant tactical opportunity emerged from the Trump administration’s $80 billion Westinghouse nuclear deal, which catalyzed a structural revaluation of uranium equities and unlocked a multi-year policy tailwind that macro strategists should integrate into baseline scenarios.

BROAD MARKET PERFORMANCE & VALUATION FRAMEWORK

EQUITY MARKET DRIVERS: EARNINGS QUALITY MASKS BIFURCATION

Earnings Season Metrics (64% of S&P 500 reported)

EPS beat rate: 83% (vs. 78% 5Y avg, 75% 10Y avg), suggests highest on record if sustained through quarter-end

Revenue beat rate: 79% (vs. 70% 5Y avg)

Blended Q3 growth: +10.7% YoY (up from 9.1% last week, 7.9% at Q-end)

Net profit margin: 12.9% (vs. 12.5% YoY, 12.1% 5Y avg)

Margin expansion: +40 bps YoY, driven by IT sector efficiency gains (27.6% NM vs. 25.1% YoY)

Sector Earnings Quality Divergence

Technology: NM 27.6% (highest on record); Amazon AWS growth accelerated to 20% (fastest since 2022); despite this, Meta’s capex guidance ($70-72B for 2025, +$4-6B vs. prior) triggered institutional concern re: AI monetization timeline

Financials: +11.1% YoY growth; NM 20.0% vs. 18.0% YoY

Utilities: +13.2% YoY; NM 16.9% (stable)

Communication Services: -13.5% YoY; NM compressed to 12.5% (vs. 14.8% YoY), Meta carnage ripple effect

Energy: NM 8.1% vs. 9.8% 5Y avg; depressed by Q4 oil price weakness despite record upstream production

Guidance Complexity

28 companies issued negative 2H guidance vs. 21 positive, indicating Q4 uncertainty despite robust 9M results. Forward 2025/2026 growth expectations remain anchored at +11.0%/+13.9% respectively, suggesting consensus has priced in “normalization” post-election policy clarity.