Market Recap 10/7/25

Market Recap – October 7, 2025

Today’s session marked a shift in tone, with major indices snapping their multi-session winning streaks as investors reacted to fresh corporate disappointments, sector volatility, and persistent macro headwinds. A confluence of risk-averse triggers, especially the ongoing U.S. government shutdown (day 7) and sharp moves in key large-cap stocks, catalyzed a modest pullback following a string of record highs across the S&P 500 and Nasdaq.

Key Index Performance

The S&P 500 experienced its first daily decline after eight positive sessions, shedding ~0.4% as Oracle’s >5% tumble and sliding cyclical names led the retreat.

The Nasdaq dropped 0.8%, weighed by mixed tech performance and a broad rotation out of recent leaders.

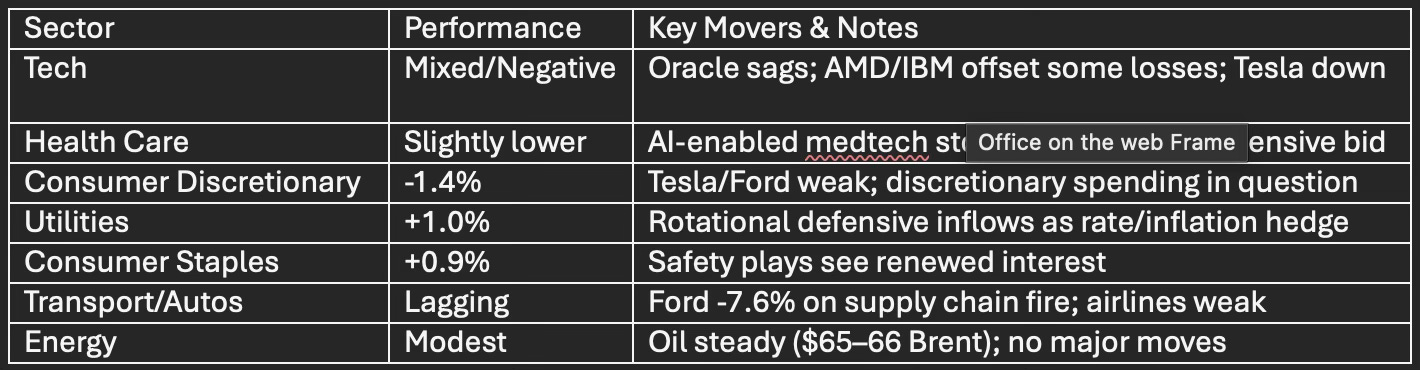

The Dow dipped 99 points, or 0.2%, with notable laggards in transport and automotive stocks.

Intraday Market Drivers

1. Oracle Selloff & Tech Reset

Oracle shares sank over 5% after reporting disappointing cloud margin and AI-infrastructure results, sparking sector-wide re-evaluation of “AI boom” euphoria and triggering profit-taking across megacaps.

AMD emerged as a relative outperformer (+4%) on a new supply partnership with OpenAI; IBM gained on AI news, but Tesla slid 4.4% after launching a lower-cost Model Y variant.

Oracle’s results and Tesla’s product news ignited pronounced single-name volatility, fueling segment rotations throughout the day.

2. Ongoing Government Shutdown: Policy & Data Risks

The seventh day of the U.S. government shutdown continues to impede the publication of official economic releases, amplifying uncertainty and suppressing risk appetite. With key macro data flows curtailed, investor focus shifted to secondary sources and upcoming Fed remarks for guidance.

Market participants are pricing in further Fed easing after September’s rate cut, but uncertainty on the path, timing, and magnitude of potential cuts remains elevated, pending both economic clarity and political resolution.

3. Flight to Safety

Heightened uncertainty and a defensive equity tone prompted flows into traditional havens: Gold futures briefly pierced $4,000/oz, and U.S. Treasury yields inched lower as investors sought shelter from headline risk and policy ambiguity.

Sector Performance & Rotation

The overall sector breadth shifted defensive, with Utilities and Consumer Staples advancing, while cyclicals, tech (ex-AI), and consumer discretionary led on the downside.

Healthcare exhibited resilience, with AI and med-tech subsegments moving against the trend as market participants rotated toward companies demonstrating innovation and fundamental strength.

Macro Backdrop & Policy Themes

Economic Data & Fed Policy

With ongoing disruption to economic releases, the macro narrative is dominated by speculation around further potential rate cuts and “soft landing” expectations.

Q2 GDP stands at 3.8% (annualized, third estimate), unemployment ticked up to 4.3% (August), and the federal funds rate target is now 4.00–4.25% after the September cut.

The job openings-to-unemployed ratio has narrowed (≈0.98), signaling slight softening in labor demand. CPI and other inflation data are delayed, keeping fixed-income and equity markets highly sensitive to Fed communications.

Policy & Event Watch

Key events this week include the FOMC minutes (Wednesday), which may shed light on internal Fed debate, and Fed Chair Powell’s Thursday speech, which could provide the next catalyst for rate/inflation expectations and asset re-pricing.

Commodities & Rates

Brent crude oil held stable near $65–66/bbl; 30-yr U.S. mortgage rates hovered at 6.34%; the U.S. dollar advanced on defensive flows.

Analyst Perspective

Today’s session underscores both the fragility and resilience of the post-summer market rally. Profit-taking from recent highs was catalyzed by earnings disappointments and ongoing macro-policy uncertainty. Sector rotations reveal risk-off features (defensives, healthcare) and continued preference for names with proven innovation in AI and technology. With official data flow restricted, markets are unusually sensitive to policy signals and single-stock narratives.

Momentum remains subject to headline risk, with outsized reactions to corporate actions (Oracle, Tesla, Ford) and policy developments (shutdown, Fed speak) likely to drive trading before core macro stability is restored.

Prepared by SEQH Capital Partners Research

As of market close, October 7, 2025