Market Recap 10/8/25

Major Index Performance

The S&P 500 and Nasdaq set new record closes, buoyed by excitement around artificial intelligence and Federal Reserve rate cut signals.

The Dow gained 0.14%, S&P 500 rose 0.56%, and Nasdaq climbed 0.98%.

Gold rallied above $4,000/oz, a new high, amid macroeconomic uncertainty and the government shutdown.

On NYSE: 350 new highs, 75 new lows; Advancers outnumbered decliners on Nasdaq.

Macro & Global Developments

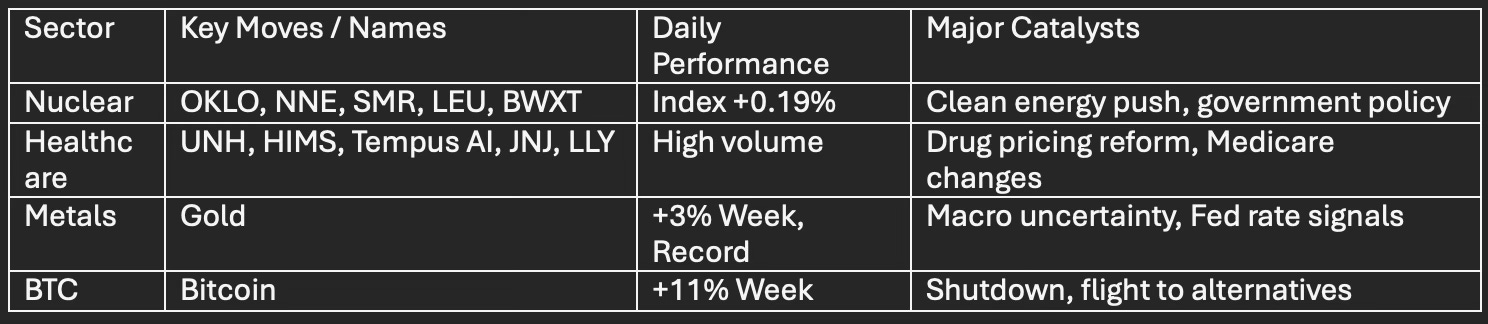

The ongoing federal shutdown reached its eighth day, delaying key economic reports and fueling reliance on alternative data.

Federal Reserve minutes indicated “around half” of FOMC participants expect two additional rate cuts before 2025 ends; the September meeting saw a 25 basis point reduction.

U.S. ADP private sector jobs fell by 32,000 in September, continuing recent weakness.

Global investor focus shifted to Fed speeches and delayed economic releases; volatility rose modestly, with VIX closing near 16.7, still well below its April highs.

Nuclear Sector

Nuclear Energy Index climbed to 51.50 USD, up 0.19% for the day and nearly 23% over the past month, reflecting robust expansion and policy tailwinds. The last 12 months show a 74.81% surge in value on sector benchmarks.

Leading nuclear equities driving volume included Oklo (OKLO), Nano Nuclear Energy (NNE), NuScale (SMR), Centrus Energy (LEU), and BWX Technologies (BWXT). These firms benefited from clean energy trends and anticipated public/private investment surges.

U.S. reactor fleet registered high operational levels, with most plants (Arkansas Nuclear, Callaway, Columbia, etc.) reporting 100% output on the day.

Healthcare Sector

Top healthcare stocks attracting large investor flows were UnitedHealth Group (UNH), Hims & Hers Health (HIMS), Tempus AI, Johnson & Johnson (JNJ), Novartis, and Eli Lilly (LLY). Sector interest was driven by telehealth platforms, precision medicine, pharmaceutical innovation, and defensive sector positioning amid uncertainty.

The Trump administration pushed deals with major pharma firms to lower drug prices, triggering activity among players like Pfizer.

Medicare policy changes, with increased focus on primary care physician pay and shifting calculation methodologies, were announced.

Stable premiums but declining plan counts marked Medicare Part D, with a shrinking option set projected for 2026.

Metals & BTC-Related Industries

Gold prices soared above $4,000/oz for the first time, up nearly 3% for the week, highlighting extreme risk aversion globally.

U.S. crude oil dropped to $61/barrel, a four-month low on oversupply fears and demand concerns.

Bitcoin rallied sharply, briefly trading above $122,000, representing week-on-week gains of about 11%.

Sector Highlights Table

Advanced Analyst Insights

Rate cut expectations drove risk sentiment and equity flows, even as data gaps complicated forecasting.

Large-cap outperformers included Dell (DELL), surging nearly 8% on upward revisions to financial projections.

Tariff threats loom over automakers, with $30B in profit impact projected by Moody’s.

Macro data absorption is limited due to the shutdown, shifting market reliance to private estimates and Fed communication.

Markets ended mixed but optimistic, with major indexes posting records yet volatility and alternative asset demand surging, a classic “flight to safety” setup amid macro uncertainty, sector rotations, and shifting policy landscapes.