Market Recap 11/3/25

U.S. MARKET TEAR SHEET | NOVEMBER 3, 2025

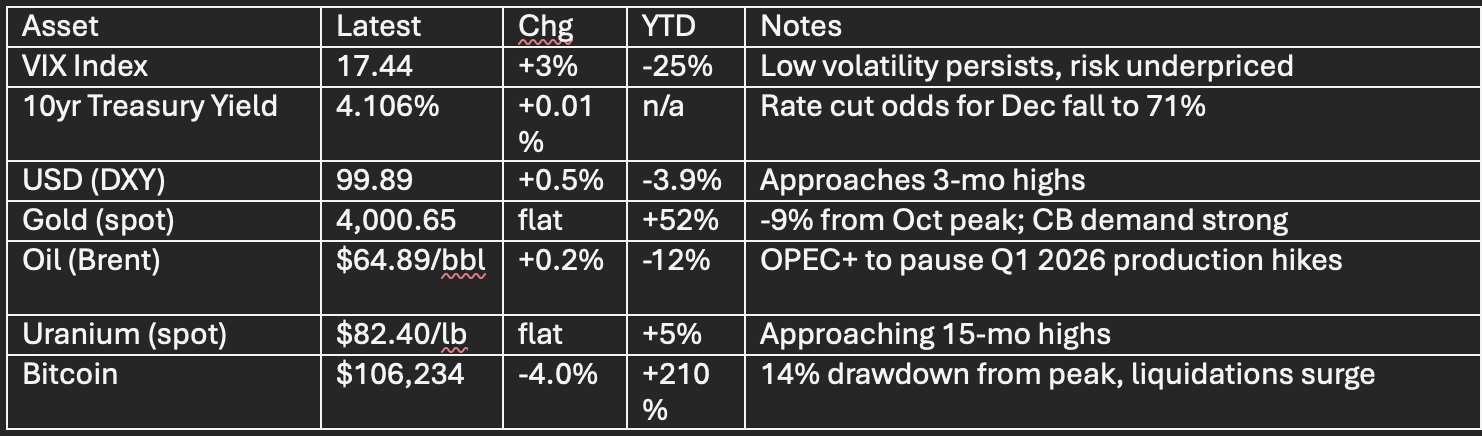

Market Snapshot

Market breadth remained negative with most S&P equities down despite positive index closes on tech leadership.

Mega-cap and AI-linked stocks continued to drive performance; small-cap and cyclical sectors underperformed.

Sector strength: Technology, Consumer Discretionary;

Weakness: Energy, Real Estate, Consumer Staples.

Key Developments

Amazon / OpenAI / Nvidia Partnership

$38B, 7-year deal: AWS infrastructure supports OpenAI’s data needs via hundreds of thousands of Nvidia GPUs.

Amazon +4.5% (new ATH), Nvidia +3.2% (YTD +54%), Loop Capital raises NVDA PT to $350, $8.5T market cap scenario mapped.

U.S. restrictions reinforce Nvidia’s leadership in advanced AI chips; MSFT export licenses into UAE data centers mark policy shift.

Corporate M&A

Kimberly-Clark to acquire Kenvue for $48.7B (largest U.S. consumer deal to date, all-cash/stock).

Kenvue +14% (deal premium); Kimberly-Clark -13/15% (integration/legal risk around Tylenol litigation weighs).

Transaction builds a $32B revenue health franchise; $2.1B synergy target, closing expected 2H26.

Palantir (PLTR): Q3 Earnings

Revenue $1.178B (+63% y/y, beat by $88M), EPS $0.21 vs. $0.17 est, Rule of 40 hits 114%.

U.S. commercial revenue +121% y/y, gov’t +52%; Q4 guide: $1.33B (61% y/y).

Raising FY outlook again; fortress balance sheet: $6.4B cash, zero debt. Stock +170% YTD.

Macro & Sector Data

ISM Manufacturing PMI: 48.7 (contracting, 8th month).

Crypto large-cap drawdown led by Fed hawkishness; $400M+ in liquidations.

Ongoing shutdown delays key macro-data; market relying on ISM, ADP, U. Michigan data.

Nuclear & Uranium Sector Focus

Landmark $80B Federal Partnership Announced

Westinghouse Electric, Cameco, Brookfield: New $80B U.S. government partnership to deploy AP1000 reactors.

Supports Presidential target: quadruple U.S. nuclear generation in 25 years.

Projected to sustain 45,000 jobs/project (2-unit), >100,000 for national deployment.

First-of-its-kind scale: transforms U.S. nuclear infrastructure policy.

Market Performance & Thematics

Uranium spot: $82.40/lb (+4.6% y/y); path toward $90-100/lb by 2026 predicted.

Nuclear Energy Index: 53.76 (-2.7% today, +80% YTD); 13.5-year highs within past week.

Key gainers (YTD): Oklo (+526%), Cameco (to ATH post-announcement)

Acute supply/demand tension: Cameco and Kazatomprom each lowered output, U.S. strategic stockpiling up, Russia excluded from U.S. enrichment supply.

Global uranium deficit projected through 2035 as new construction (>60 reactors in progress) persists; sector expected to outperform cyclically and structurally.

SEQH CAP RESEARCH: STRATEGIC TAKEAWAYS

Leadership Narrowness at Highs: Mega-cap AI, cloud, and chip names now responsible for majority of S&P500/Nasdaq YTD return. Market breadth and rotation risk remain key as passive flows chase performance.

Nuclear/uranium thesis: Unmatched structural drivers, federal policy, supply chain tightness, generational growth mandate. Remain overweight sector, emphasizing established producers and services (Cameco, BWXT, NuScale, Centrus).

Macro Volatility: December rate cut odds pared to 71%; shutdown heightens data risk. Monitor for inflections in real rates, vol, and risk premium.

Selectivity Essential: M&A (Kimberly-Clark/Kenvue) highlights that valuation discipline and synergy realization matter.

Crypto/Commodities: Unwind of excess leverage creates tactical opportunity in headline-driven selling; gold steadies despite rate back-up.