Market Recap

11/11/25

U.S. MARKET ADVANCED TEAR-SHEET

Trading Day: November 11, 2025

Top-Level Index Performance

Sector Rotation & Breadth

Market rotation was out of mega-cap tech and into industrials, energy, and consumer staples.

NYSE advance/decline: 67% advancing; new highs/new lows: 146/66.

VIX: 17.60 (-7.8%), signaling subdued volatility.

Put/Call Ratio (SPX): 1.07, indicating moderated hedge demand.

Rates, FX, and Commodities

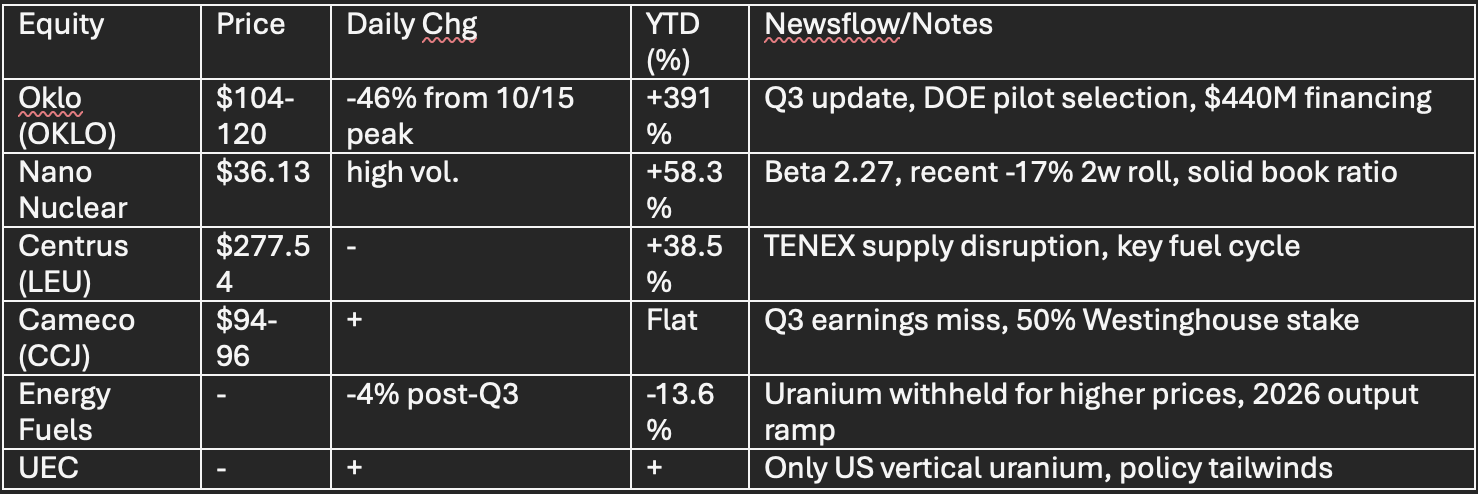

Nuclear & Uranium Sector Focus

Uranium Spot: $80/lb (up 25% YoY), long-term $85/lb, futures $80.80/lb.

Supply Deficit: 2025–2045 gap projected at >1.75B lbs; U.S. uranium now a Critical Mineral.

Nuclear Energy Index: 48.20, -12.89% MoM, still +60.7% YoY.

Pre-revenue SMR stocks remain volatile, Oklo risk skew high, NNE has valuation cushion.

Macro Catalysts and Key Themes

U.S. shutdown resolution catalyzed value rally, Dow ATH.

Mega-cap AI/tech: profit-taking on capex concerns, e.g., Nvidia -2.9% today, CoreWeave -16%.

Economic Data: Delayed jobs/CPI rolling out next; labor softening per ADP (-11K jobs/wk).

Earnings: Q3 nearly complete, 82% EPS beats; Buyback window robust through 12/19.

Fed: December cut 64% probability; rates anchored by soft macro & delayed data.

Tactical Calls

Favorable: Financials, Energy, Healthcare, select uranium producers.

Cautious: Mega-cap tech; SMR/speculative nuclear names.

Monitor: Market breadth, volatility, post-shutdown economic data flow; continued sector rotation.