Market Recap

11/6/25

U.S. Market Tear Sheet - November 6, 2025

Market Overview: Sharp Risk-Off Turn

S&P 500: 6,720.32 (-1.1%)

Dow Jones: 46,912.30 (-0.8%)

Nasdaq: 23,053.99 (-1.9%)

Russell 2000: 2,418.82 (-1.9%)

VIX: Approx. 18.0 (near-term highs)

Summary:

Broad-based equity selloff led by technology and consumer discretionary.

AI/semiconductors weighed on risk sentiment, with renewed attention on valuations and earnings growth.

Defensive rotation evident, healthcare outperformed, energy stable.

Macro & Policy Drivers

Government Shutdown: Longest in U.S. history, day 37. Data blackout affecting labor/inflation reporting. FAA to cut 10% of flights at 40 airports, compounding real-economy risks.

Federal Reserve: 70% probability of 25bp December rate cut (CME). Weaker labor data tilts expectations dovish; fixed income markets rally.

Supreme Court Tariffs: Justices skeptical of executive tariff authority, raising odds for adverse Trump ruling, market volatility likely near verdict.

Economic & Labor Data

Private Payrolls (Oct): -9,000 jobs, 4.4% headline U3 unemployment (Chicago Fed/est).

Layoffs: Highest October since 2003; tech sector cutbacks dominate.

GDP Outlook: Q4 consensus down to 1.0% annualized amid shutdown.

Credit & Rates

10-year Treasury: 4.09% (-6.4 bps, sharpest one-day rally in weeks).

Investment Grade/Tech Bonds: Heavy investor demand, especially for recent tech megacap issues.

VIX: ~18–19, indicating medium-level stress, increased institutional hedging activity.

Key Sector Performance

Commodity & Crypto Highlights

Gold: $4,004.78/oz (+0.62%); resilient haven. Year-to-date: +48%.

Crude Oil (WTI): $59.43/bbl; three-day decline on supply/demand.

Bitcoin: $101,977 (-3%); remains over key $100k level, JPMorgan “undervalued vs. gold”.

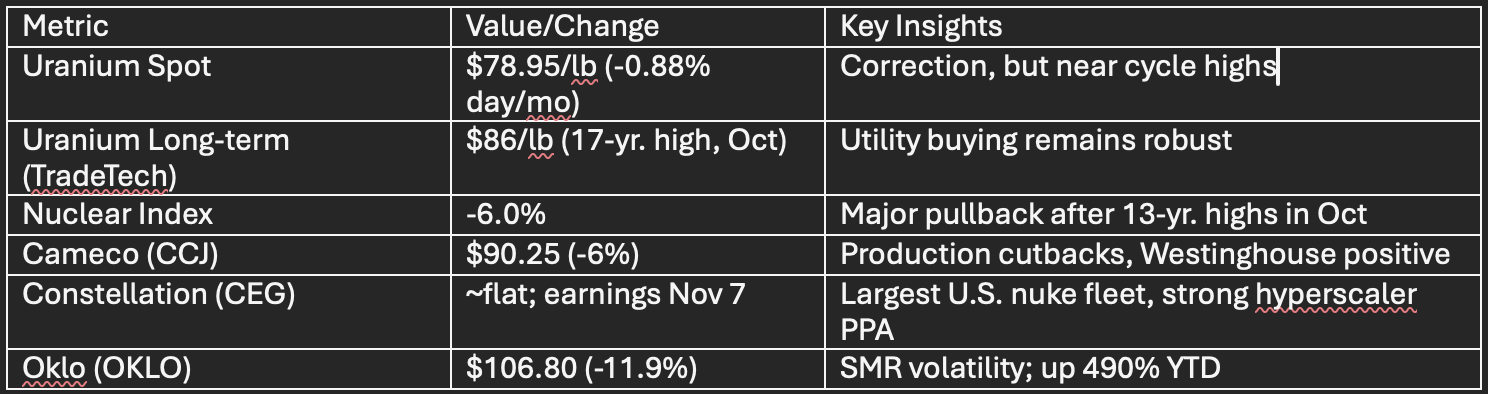

Nuclear & Uranium Sector Focus

Sector outlook: Pullback in equities, but fundamentals (supply-constrained, new U.S. policy favoring uranium, hyperscaler demand) remain bullish. Analyst consensus overwhelmingly constructive on quality uranium/nuclear plays.

Forward Catalysts

Constellation (CEG) earnings, post-market Nov 7.

Gov’t shutdown & Supreme Court tariff decision, watch for headline volatility.

Fed communications, expect December cut probability swings on any labor/inflation leaks.

SEQH Capital View

Remain tactically defensive in overvalued tech and cyclical sectors; rotation towards quality defensives.

Nuclear/uranium pullback viewed as an entry; secular bull thesis intact given demand/supply realities.

Maintain above-average vigilance for volatility and policy-driven headline risk.

Prepared by SEQH Capital Partners Research – November 6, 2025