Market Recap

11/10/25

Market Recap Tear-Sheet - November 10, 2025

Macro Market Performance

Sector & Thematic Standouts

Tech/Semis: NVDA +4.8%, AMD +2.0%, TSM +3%, SMH ETF +2%

Drivers: China resource export pause, shutdown relief“Magnificent Seven”: Strong recovery; MSFT +0.8%, AAPL +1.8%, TSLA +3.99%

Financials: BAC, WFC hit new 52w highs; insurers lag on ACA uncertainty

Energy: WTI crude +0.6% at $60.10/bbl; oil steady, natural gas +3.1%

Gold/Silver: Gold +2.8% ($4,100/oz), Silver +4.5% ($50/oz); safe-haven flows return

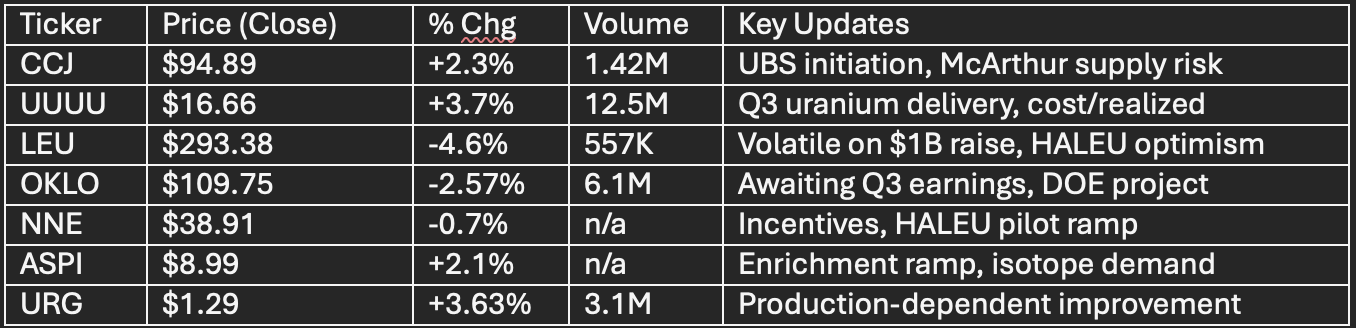

Nuclear & Uranium Sector Sheet

Uranium Spot Price: $77.45/lb, FY25e: $78.17/lb, YoY +1.18%

Nuclear Index: 48.61 (+0.43%); 1M -5.38%, 1Y +57.4%

Key Macro: Kazatomprom Q3 exports +33%; Cameco 2025 output seen -19%; SMR valuations under pressure

Market Microstructure/Technical

Breadth: Advancers outnumber decliners; strong volume (+18% above avg)

Put/Call Ratio: Total: 1.08 (elevated); Equity: 0.63 (risk management, not panic)

% Above 200d SMA: S&P 500, 53.1%, Nasdaq, 45.3%, Russell 2K, 53.2% (stabilizing)

Key Support: S&P 500, 6,700, Resistance, 6,850, ATH—6,930

Macro/Crypto/FX

Fed Watch: Dec. cut odds 67%; data dump post shutdown seen as catalyst

USD Index (DXY): 99.57 (-5.6% YoY), EURUSD 1.16, JPY 153

Bitcoin: $105,500 (+1.6%); flows accelerate on ETF and stimulus talk; ETH +5.5%, XRP +8.6%

Key Events: AMD Analyst Day & Oklo Q3 (Tues), Nvidia earnings (Nov 19), House votes on shutdown

Analyst View and Risks

Most risk-on session since May: tech, uranium, crypto strong

Market breadth improved, but leadership remains narrow; watch for follow-through

Nuclear sector: favor CCJ, UUUU, LEU fundamentals; pre-revenue (OKLO, NNE, ASPI) at risk if no near-term catalysts

Dec. Fed policy, “data dump,” and AI earnings key for sector rotation

Watch for volatility spikes as delayed economic data is released