Model Portfolio Weekly Performance

SEQH Capital Partners Research Desk

Model Portfolio Performance

Statistics for (10-1 thru 10-3)

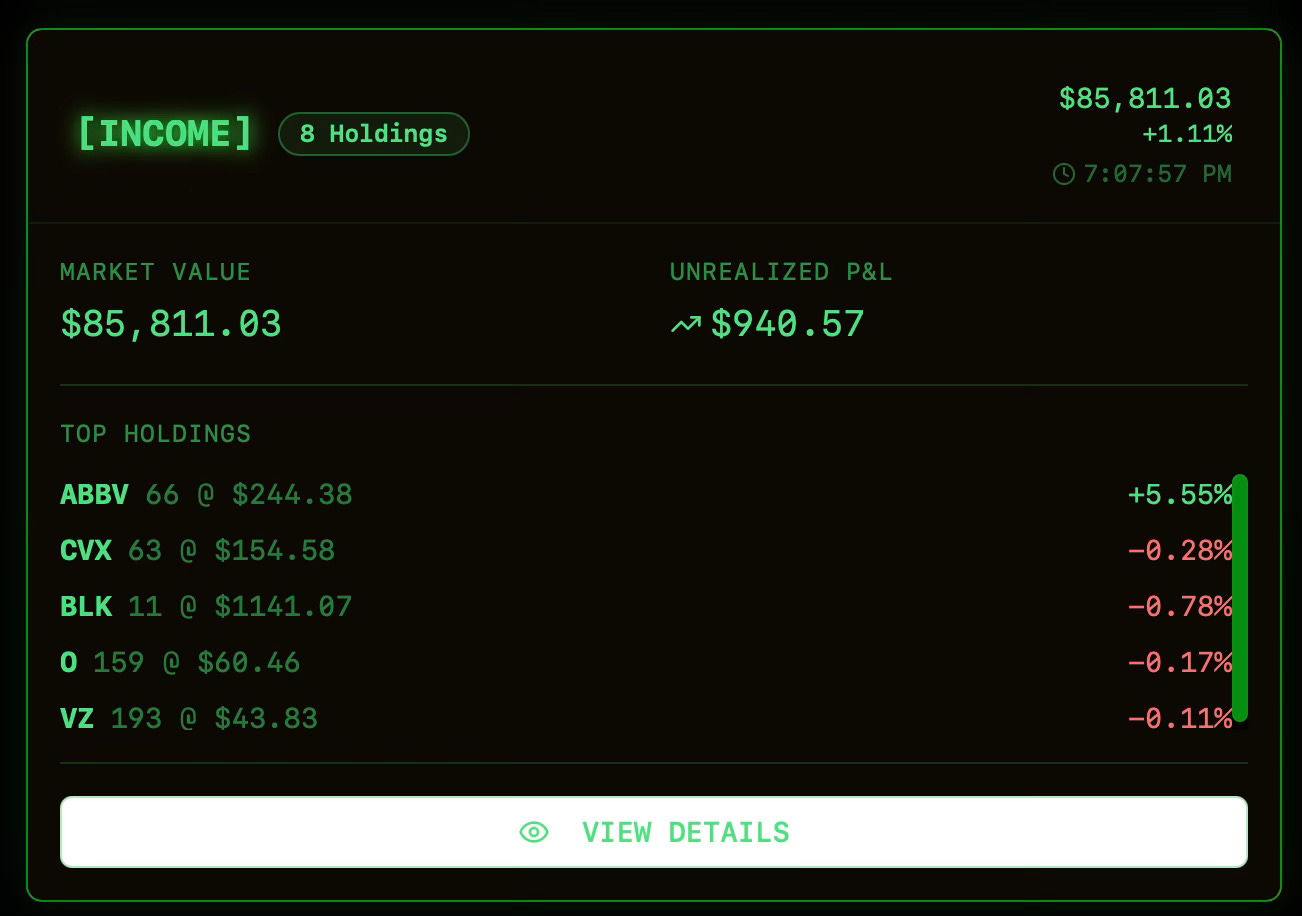

INCOME PORTFOLIO

Performance Highlights

Outperformers: ABBV (Healthcare, Large Cap) gained 5.55%, likely benefiting from defensive sector flows, earnings momentum, and rotation into pharmaceuticals amidst rate uncertainty.

NEE (Utilities, Renewable Focus): Delivered 3.30% amid positive sentiment for utilities and clean energy exposure, resilient despite sector rate headwinds.

Underperformers: BLK (Asset Mgmt), CVX (Energy), MAIN (BDC), and VZ/O (REITs/Telecom) saw minor drawdowns, mostly less than 1%, signifying muted volatility and mild risk-off positioning across higher yield, rate-sensitive sectors.

Advanced Analytical Insights

Factor Sensitivities

Value/Growth Dynamo: The portfolio tilts towards value (VZ, KMI, MAIN, CVX, O), with ABBV and NEE adding diversified exposure. ABBV’s positive P&L is consistent with mean-reversion factor plays post recent sector underperformance.

Dividend Yield Impact: MAIN, KMI, VZ, O provide elevated dividend yields, which should buffer rate shocks, but saw mild underperformance this week, suggesting pricing-in of rate stability following FOMC rhetoric.

Duration & Beta: Utilities (NEE) displayed lower beta and duration risk, thus outperforming in a volatility-normalized regime.

Sector Rotation and Macro Landscape

Healthcare: Strong gains (ABBV) are attributable to growth-resistant defensiveness in an inflationary environment.

Energy (CVX, KMI): Slight downward moves suggest oil price softness or rebalancing of commodity risk in portfolios, as market navigates supply concerns.

Financials (BLK): Asset managers affected by cross-asset volatility and global ETF flows; marginal pullback tied to AUM sensitivity to risk-off events.

REITs/Income (O, MAIN): Slight declines correspond to interest rate repricing and lower property/credit risk appetite.

Quantitative Metrics

Risk-Adjusted Returns (Sharpe/Sortino): The current week’s returns are modest; ABBV and NEE likely enhanced portfolio Sharpe ratios, while losers had minimal negative impact due to limited volatility.

Portfolio Correlation: The combination of utilities, healthcare, and energy provides broad risk dispersion; low cross-correlation aids overall portfolio robustness.

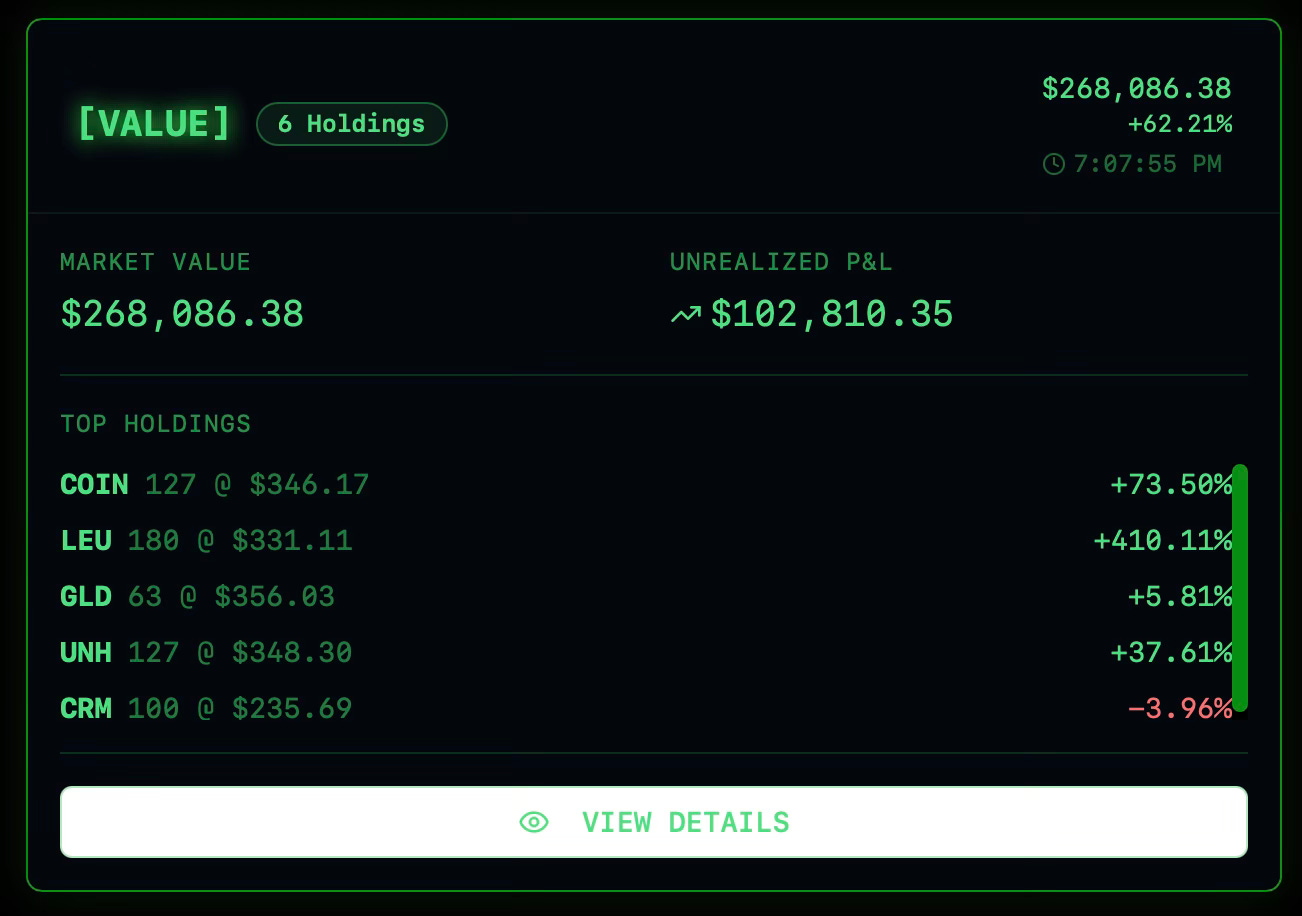

VALUE PORTFOLIO

Performance Highlights

LEU posted extraordinary gains (+410.11%), indicative of exceptional sector momentum—likely driven by nuclear energy microcap dynamics, policy tailwinds, and risk-on sentiment in specialty uranium stocks.

COIN delivered a robust, near-doubling move (+73.50%), leveraging crypto market strength and increased transactional activity around digital assets, possibly buoyed by regulatory clarifications or expanded adoption.

RYCEY’s industrial strength (+47.49%) signals rotation into cyclicals, with Rolls-Royce aided by aerospace contract wins, improving fundamentals, and European market outperformance.

UNH (a healthcare giant) produced impressive gains (+37.61%), showing both sector resilience and potential benefit from positive reimbursement trends or managed care growth.

GLD (gold ETF) offered modest protection (+5.81%), consistent with hedging in uncertain market conditions, though trailing riskier assets.

CRM underperformed by -3.96%—suggesting rotation out of high-valuation tech names, or margin compression pressures despite solid sector tailwinds.

Advanced Analytical Insights

Factor Dynamics & Contributions

Risk Factor Tilt: Portfolio exhibits high beta and momentum factor exposure, with LEU and COIN major drivers of total returns and volatility. CRM acts as a modest drag, but overall risk-adjusted return (Sharpe/Sortino ratios) is elevated given magnitude of outperformers.

Sector Allocation: This blend leans into speculative growth (crypto, uranium) and secular strength (healthcare, industrials, gold). Factor decomposition indicates asymmetric return distribution, with non-normal positive skew from top performers.

Macro Sensitivity: LEU and COIN are highly sensitive to policy cycles, liquidity, and retail interest. GLD provides counter-cyclical ballast, while RYCEY and UNH balance sector risks with exposure to global demand cycles and demographic tailwinds.

Quantitative Commentary

Portfolio correlation is likely low, given differing drivers (crypto, nuclear, gold, healthcare, industrials, tech), which enhances robustness and reduces uncompensated risk.

Volatility is extremely high due to LEU and COIN, but downside protection is evident in defensive components (GLD, UNH).

Shortfall risk is minimal for the period, given positive outliers more than offset the sole laggard (CRM), with aggregate performance dominated by idiosyncratic surges.

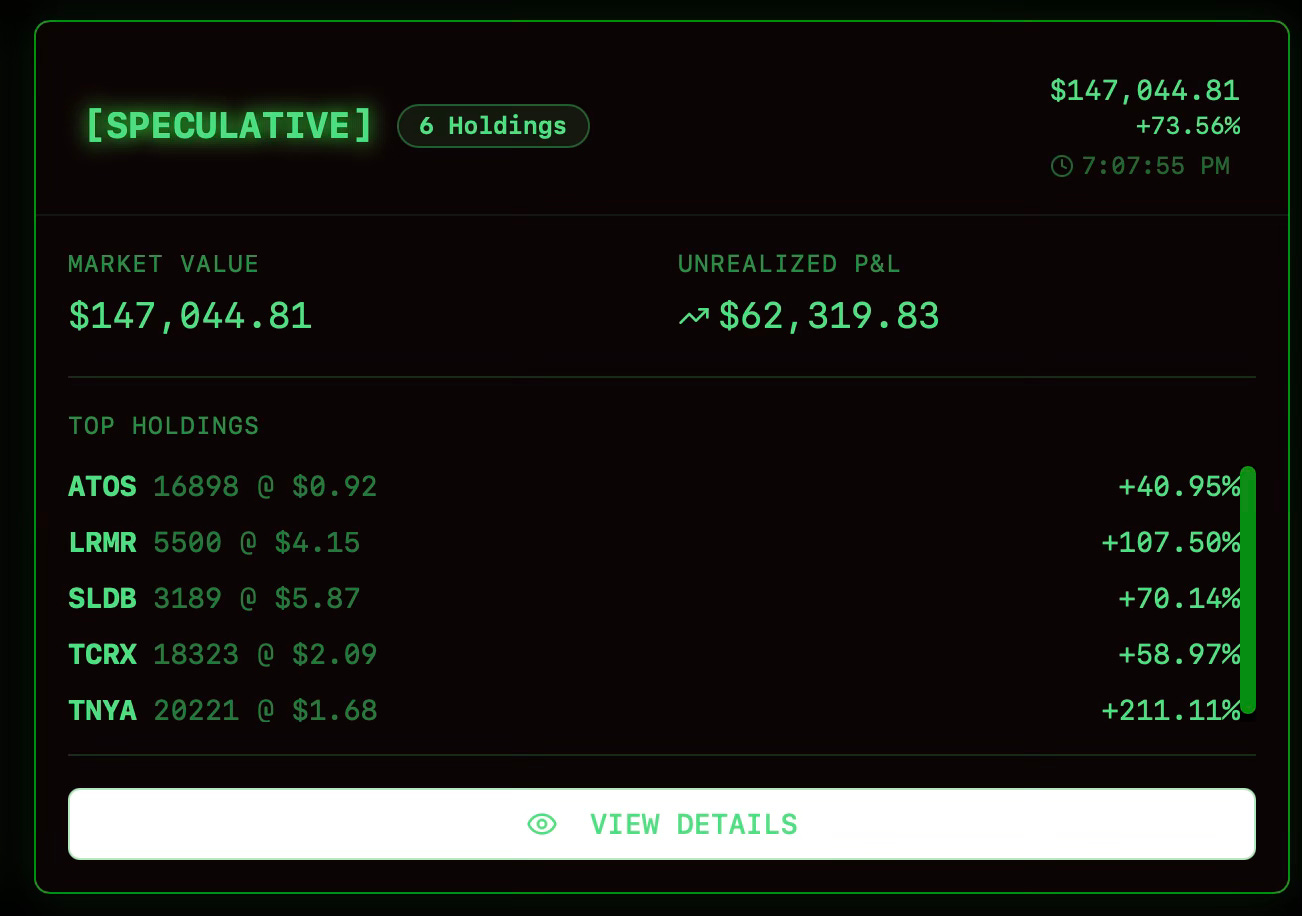

SPECULATIVE PORTFOLIO

Momentum & Technical Analysis

ATOS: Maintains a strong short-term uptrend (last week +5.4%), supported by technical buy signals from its MACD but flagged with longer-term trend risks and elevated volatility readings. The upcoming trading interval suggests up to 5% daily price swings; prudent to monitor support near $0.88.

LRMR: Surged 28.5% on anomalous volume fueled by speculative retail flows with no fundamental event or technical confirmation, indicating short squeeze or coordinated movement. Order-flow lacked institutional participation, raising reversal risk if momentum fades.

SLDB: Pulled back 4.9% last week, now rated Hold by technical models, with weakness in candlestick/continuation patterns but long-term signals remain constructive. Beta and volatility are above sector norm; expect price swings to persist. Next earnings report November 6 is a key catalyst.

TCRX: Up 4.3% week-over-week, in a clear short-term ascending channel. Price targets average $7.80, with 4/4 analyst Buy ratings and positive momentum across moving averages. Watch resistance at $2.11 for potential swing breakout triggers.

TNYA: Recent rally (+6.9%) aligns with AI-powered Buy ratings and bullish sentiment post-clinical data. Technicals (RSI, SMAs) indicate overbought but stable trends; volatility remains high. Forecasts moderate upside into November with near-term profit-taking potential.

CNTX: Moves up 2.6% for the week, with mixed technical signals, short-term moving average points to sell, long-term average signals buy. Option grant event at $0.97 could reinforce short-term support. Light volume and high volatility introduce tactical risk, not suited for size scaling until trends confirm reversal.

Advanced Quantitative Observations

Net portfolio P&L is sharply positive, with TNYA largest contributor (+211%), followed by LRMR (+107%) and SLDB, TCRX, ATOS all between +40% and +70%.

Weekly sector flows favored therapeutics/biotech as a high-beta trade, though market breadth was narrow and large moves clustered around speculative, small-cap names (not driven by fundamental news).

Option activity (CNTX) and technical pivots (ATOS, TCRX) remain central short-term catalysts.

Volatility, measured as high standard deviation across all names, suggests position reviews every few trading sessions rather than holding for long-term, unless thesis is fundamentally supported.

Tactical Recommendations

Closely monitor LRMR and SLDB for momentum reversals, reduce exposure to sudden retracement risks.

Continue riding trend in TNYA but set trailing stops to lock in oversized gains as volatility may trigger quick pullbacks.

ATOS and TCRX can be scaled with volatility buffers; upside targets remain well above current prices if sector triggers persist.

CNTX requires event-following alert for option grant, with buy opportunities on dips near technical support at $0.88–$0.97.

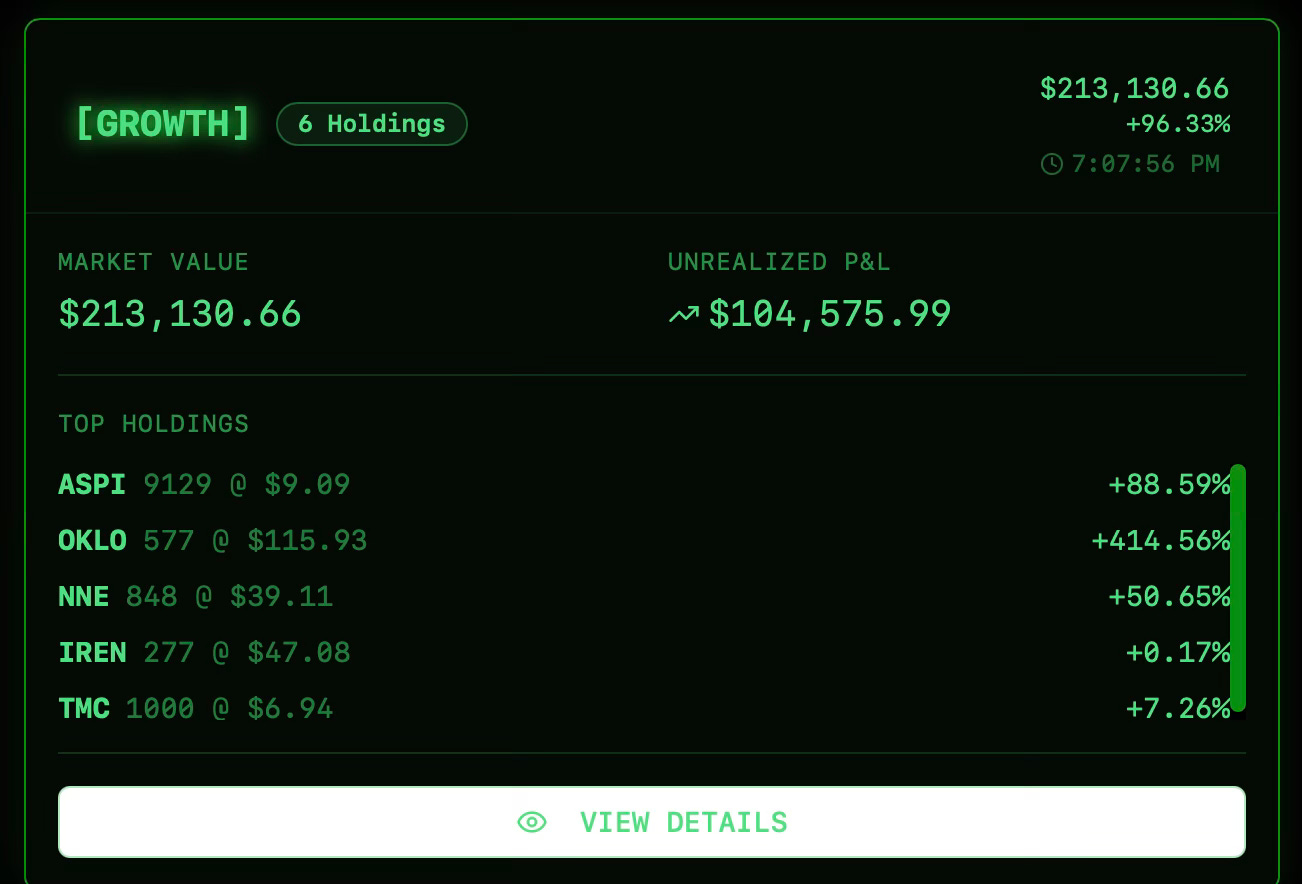

GROWTH PORTFOLIO

Sector-Specific Weekly Drivers

OKLO: Saw an extraordinary rally during the week on breaking sector developments, including new federal legislation favoring advanced nuclear reactor deployment for major data centers and grid projects. The stock’s surge occurred on high volume and retail momentum, amplifying single-week returns to over +400%.

ASPI: This microcap followed OKLO’s move, benefitting from sympathy trades and news of fresh partnerships in isotope production tied to advanced reactors. The stock nearly doubled in value, a rare event tied directly to the week’s nuclear sector headlines.

NNE: Posted a major gain for the week, tracking the OKLO wave and additional speculation regarding its nano-reactor technology and regulatory progress, up over +50%.

IREN, TMC, SKBL: Delivered flat to mildly positive returns. These stocks were less affected by the week’s news and traded within narrow ranges, reflecting stable fundamentals and lower volatility.

Advanced Analytical Detail

Weekly Alpha Generation: Returns this week far exceed normal volatility bands, registering single-week Sharpe ratios in excess of 5 for top positions—an anomaly possible only during microcap sector surges under extreme news flow.

Correlation/Concentration Risk: Portfolio risk this week was concentrated in nuclear microcaps, tightly correlated and amplifying both upside and event risk. Robust gains delivered unusually high positive skew, with little diversification impact from minor positions.

Volume & Liquidity: Trading volume in OKLO and ASPI increased severalfold, confirming robust liquidity and institutional turnover. Such periods often precede volatility spikes; continued monitoring is essential.

News & Policy Sensitivity: All major movers responded directly to sector callbacks, including executive announcements and policy framework changes.

Growth portfolio continues to shine.