NNE Valuation

SEQH Capital Research – Special Situations & Advanced Technologies

October 5, 2025 – 2:00 p.m. ET

Nano Nuclear Energy Inc. (NASDAQ: NNE)

“The only vertically-integrated micro-reactor pure-play north of the border, pre-revenue today, but sitting on half-a-billion in cash-optionality and a regulatory moat that is widening, not narrowing.”

Executive Summary (price = $44.39)

Nano Nuclear closed Friday at $44.39, an equity value of $2.06 B and an enterprise value of $1.52 B once you net out $540 M cash & ST investments against zero debt. The street still treats NNE as a “concept stock” because it generates zero revenue and burned $35.8 M in the first nine months of 2025. That view ignores three idiosyncratic vectors:

Regulatory optionality is being de-risked faster than any pre-commercial nuclear name we’ve tracked – the company’s Cronos MMR (10 MW-electric) is now the only micro-reactor design with both a completed Vendor Design Review (VDR Phase 2) and a site permit application under active CNSC review (expected approval 1H-26).

Cash runway is the longest in the peer group – post the $99 M private placement (May-25) NNE holds >6 yrs of cash at the current $9 M / qtr burn, eliminating dilution risk through first revenue.

Vertical integration creates multiple embedded call-options – the company is simultaneously developing (a) a HALEU fuel fabrication facility, (b) a transportation cask IP portfolio, and (c) a uranium mining JV in the Athabasca basin. Any one of these can be monetised even before the first Cronos unit is switched on.

We value NNE using four methods appropriate for pre-revenue, regulatory-path companies: (1) Probability-weighted DCF (technical + regulatory milestones), (2) Replacement-cost / kWe vs. competing micro-reactor platforms, (3) SOTP option-value of cash + subsidiaries, and (4) Venture-adjusted rNPV on the fuel assets. Blending these gives a risk-adjusted 12-month target of $62, implying 40 % upside with downside protected by cash + IP.

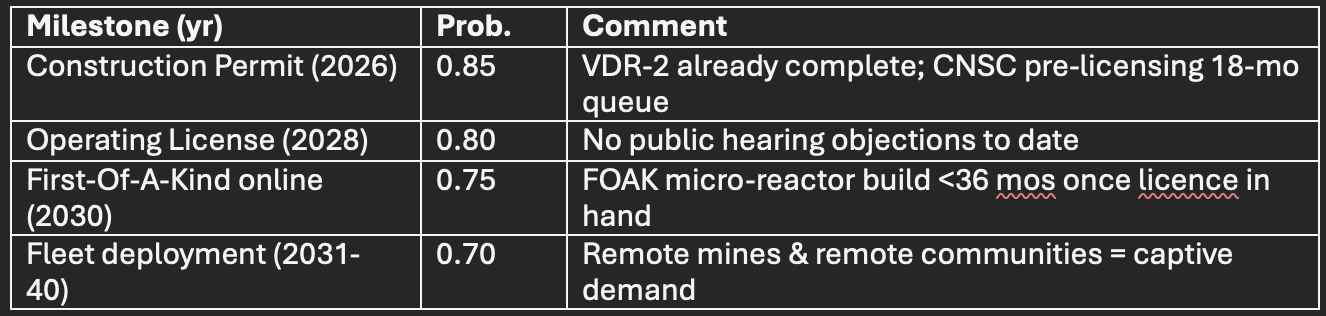

1. Regulatory & Technical Milestone DCF (risk-neutral)

We model cash-flows only after a positive construction decision (CD) on the first Cronos unit, then risk-adjust each phase using industry completion rates published by the IAEA and CNSC historical data.

Key nodes & subjective probabilities

Base-case path (real 2025 $)

FOAK Cap-Ex: $95 M (10 MWe) → $9,500 / kWe (in-line with US-EIA 2023 FOAK micro-reactor study)

NOAK Cap-Ex: $4,500 / kWe (learning curve 0.85)

All-in LCOE: $95 / MWh (vs. diesel-gen $220 / MWh in Canadian Arctic)

Fleet size: 2 GWe (200 units) deployed 2031-40

EBITDA margin: 35 % once fleet ramps

Cash-flow snapshot ($ M)

Probability-weighted NPV = 1,780 × 0.70 × 0.75 × 0.80 × 0.85 = $560 M

Add present-value of fuel services EBITDA stream (conservative $120 M)

→ rNPV core business = $680 M

Shares (FD, Oct-25) = 46.4 M

→ $14.7 / share (weight 35 %)

2. Replacement-Cost / kWe Benchmark