Nuclear Company Earnings Outlook

SEQH Capital Research: Nuclear Sector Earnings Preview - Q3/Q4 2025

November 1, 2025

Executive Summary

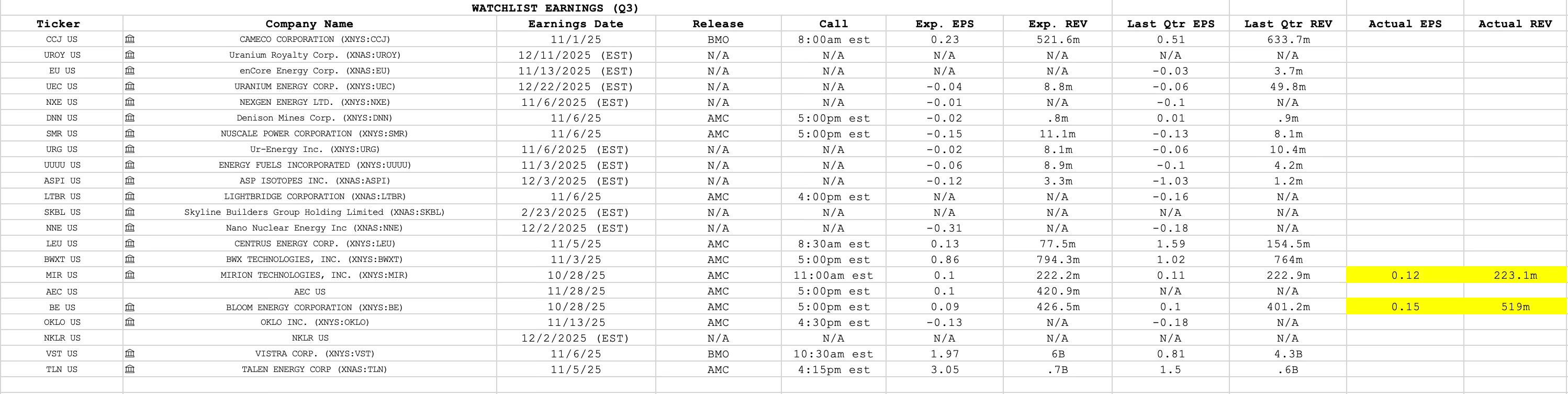

The nuclear energy sector enters a transformative earnings season with 22 companies reporting between late October and mid-December 2025, spanning uranium producers, advanced reactor developers, nuclear equipment manufacturers, and utilities capitalizing on surging AI-driven data center demand. Cameco Corporation (CCJ), the bellwether uranium producer, reports Q3 results this morning with consensus estimates of $0.23 EPS on $521.6 million revenue, setting the tone for an industry navigating a structural uranium supply deficit of 50 million pounds annually against 180 million pounds of global demand. The sector faces a critical inflection point: uranium spot prices hover at $82.40/lb after reaching year-highs of $83.18 in September, while uranium demand is forecast to surge 28% by 2030 and more than double to 150,000 metric tons annually by 2040, driven by the confluence of nuclear capacity expansion, energy security imperatives, and the AI revolution consuming 945 terawatt-hours by 2030.

Key Investment Themes: Investors should focus on five critical developments through this earnings cycle: (1) supply-demand fundamentals, with major producers Cameco and Kazatomprom reducing 2025 guidance and creating acute tightness; (2) AI data center nuclear partnerships, including Amazon-Talen’s 1,920 MW agreement and Google-NextEra’s Duane Arnold restart; (3) SMR commercialization progress, particularly NuScale (SMR) and Oklo (OKLO) advancing toward 2030 deployment; (4) enrichment and fuel services growth, led by Centrus Energy (LEU) and BWX Technologies (BWXT); and (5) policy tailwinds, including the Trump Administration’s May 2025 executive orders targeting 400 GW nuclear capacity by 2050.

Uranium Market Context: Structural Deficit Drives Multi-Year Bull Case

The uranium market has entered a genuine structural deficit that will persist well into the 2030s, underpinned by mathematics that no amount of short-term volatility can obscure. Global nuclear reactors consume approximately 180 million pounds of uranium annually, while primary mining production delivers only 130 million pounds, a persistent 50-million-pound deficit that has exhausted secondary inventories and stockpiles built during prior cycles.

Supply Constraints Intensifying: Cameco, the world’s second-largest uranium producer, cut 2025 production guidance in August, forecasting a 19% decline in mined output from its flagship McArthur River operation in Saskatchewan due to expansion delays. Simultaneously, Kazakhstan’s Kazatomprom, the global leader producing 24% of world supply, announced a 10% output reduction for 2026. These twin supply shocks have catalyzed spot price appreciation from the March low of $63.25/lb to the current $82.40/lb, with Goldman Sachs forecasting prices reaching $90-$100/lb by mid-2025 and Citigroup projecting $100/lb in 2026.

The supply crisis extends beyond near-term production cuts. Cameco’s Grant Isaac warned that the market “doesn’t appear to be pricing in” the depletion of Cigar Lake Mine (18 million lbs/year) within 10 years and McArthur River within 15-20 years. Kazatomprom similarly acknowledged that half its current projects will exhaust within a decade, and it cannot replicate its highest-grade deposits. The World Nuclear Association estimates that new uranium mines now require 10-20 years from discovery to production, up from 8-15 years previously, creating an insurmountable timeline mismatch as 70% of post-2027 utility demand remains uncontracted, the highest level in 30 years.

Demand Trajectory: The demand side presents an equally compelling bull case. The World Nuclear Association forecasts uranium requirements will rise from 68,920 metric tons in 2025 to 150,000 metric tons by 2040, a 117% increase, driven by 87% growth in global nuclear capacity to 746 GWe. This expansion is fueled by decarbonization mandates, energy security imperatives following Russia-Ukraine disruptions, and the AI data center boom requiring 24/7 carbon-free baseload power that only nuclear can reliably provide. Goldman Sachs projects the uranium supply deficit will widen from 17,500 tons in 2030 to 100,000 tons by 2045 as new reactors come online faster than new mines can supply them.

Tier 1: Uranium Producers & Developers - The Foundation

Cameco Corporation (CCJ) - Industry Bellwether Reports Today

Earnings Date: November 1, 2025 (Before Market Open) | Consensus: $0.23 EPS, $521.6M revenue

Cameco’s Q3 results will set the narrative for the entire uranium complex, with analysts expecting year-over-year revenue growth of 28.6% despite the company’s August production guidance cut. The market will scrutinize three critical areas: (1) Pricing power, as Cameco navigates spot prices averaging $81.58/lb in Q3, up 30% year-over-year, versus the company’s long-term contract portfolio; (2) McArthur River ramp-up progress, following delays that prompted the 19% production cut to 19 million pounds for 2025; and (3) Long-term contracting momentum, as CEO Tim Gitzel emphasized the company is “continuing to be selective in committing our unencumbered, tier-one, in-ground uranium inventory” amid strengthening nuclear fundamentals.

The Q2 2024 baseline provides context: Cameco reported $0.51 EPS on $633.7M revenue, but the company beat Q3 2024 estimates with strong operational performance across uranium and fuel services segments, driving adjusted EBITDA of $1 billion for the first nine months. The board increased the annual dividend from $0.12 to $0.16 per share and announced plans to double dividends to $0.24 by 2026, reflecting confidence in tier-one production restoration and industry fundamentals. For Q3 2025, any upward revision to 2025 EBITDA guidance (currently $5.0-5.2B) would signal improved pricing or volume, while investors will watch for 2026 guidance incorporating the expanded nuclear policy landscape.

Investment Outlook: Cameco trades at a Zacks Rank #3 (Hold) with consensus 2025 EPS of $1.27, representing solid execution but limited upside at current valuations after the stock’s 103.7% year-to-date gain. The long-term thesis remains intact: Cameco controls tier-one assets (McArthur River, Cigar Lake) with decades of reserves, the second-largest competitive nuclear fleet positioning, and a diversified fuel services business through its Westinghouse subsidiary. However, near-term earnings volatility is likely as uranium deliveries fluctuate quarterly, making the company best suited for patient, fundamental investors betting on the multi-year supply deficit.

Energy Fuels Inc. (UUUU) - Domestic Production Leader

Earnings Date: November 3, 2025 (EST) | Consensus: -$0.06 EPS, $9.85M revenue