Nuclear/Uranium Portfolio Builds

Three Growth-Focused Nuclear & Uranium Portfolios with Risk Analysis

This is an exciting start to a long process of analysis on these portfolios specific to nuclear and uranium. While these were not run through our custom quantitative models, they were put through our risk models.

Each of these will be analyzed in much greater detail, down to each individual holding over the coming weeks. Will be exciting to track their growth as well.

Based on comprehensive analysis of our watchlist tickers, we’ve constructed three distinct portfolios tailored to different risk profiles while maintaining a growth objective. Here’s the complete breakdown:

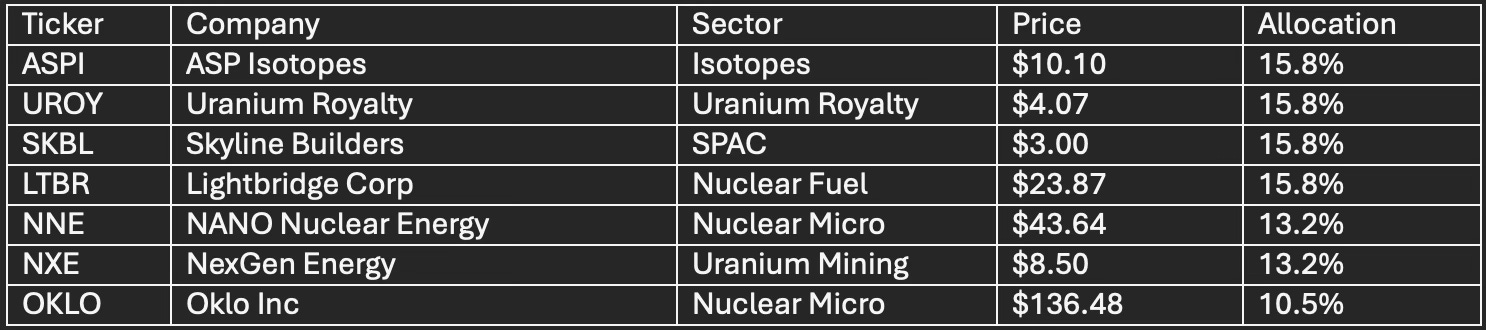

Portfolio 1: HIGH RISK - AGGRESSIVE GROWTH

Target: Maximum growth potential from emerging nuclear technologies

Expected Volatility: Very High | Time Horizon: 3-5+ years

Portfolio Characteristics:

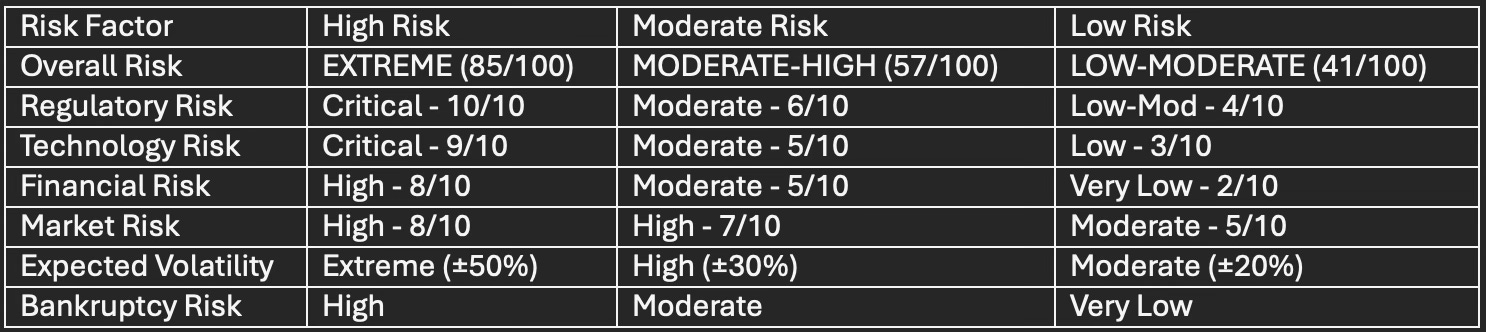

Average Risk Score: 81.6/100 (Extreme)

Average Market Cap: $4.2B (Small-Mid Cap)

Revenue Generating: 28.6%

Profitable: 0%

Average Beta: Extreme volatility

Critical Risk Factors:

Development Stage Risk (9/10): 71% are pre-revenue companies developing unproven technologies. OKLO and NNE are developing microreactor technology with no commercial deployments.

Regulatory Risk (10/10): All nuclear holdings require NRC approval, a multi-year process. OKLO and NNE must obtain construction permits before any deployment. Regulatory delays or denials could halt operations entirely.

Capital Risk (8/10): Pre-revenue companies are burning cash and will require significant additional funding. High dilution risk from future equity raises. (This is why we always factor runway into our model ports.)

Volatility Risk (10/10): ASPI’s beta of 3.31 means it moves 3.3x the market. Portfolio prone to speculation-driven 30-50% drawdowns.

Potential Upside: 500-1000%+ returns if technologies succeed. First-mover advantage in microreactor/advanced fuel markets with growing government support.

Recommended Allocation: MAX 5-10% of total portfolio

Suitability: Aggressive growth investors only, comfortable with 50%+ potential losses

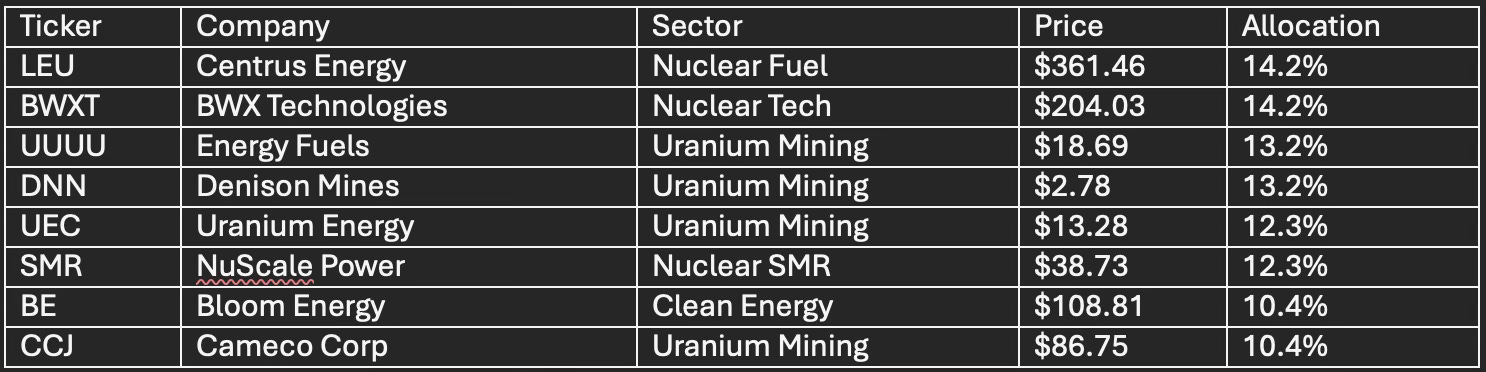

Portfolio 2: MODERATE RISK - BALANCED GROWTH

Target: Growth with established players for stability

Expected Volatility: Moderate to High | Time Horizon: 2-4 years

Portfolio Characteristics:

Average Risk Score: 56.8/100 (Moderate-High)

Average Market Cap: $15.4B (Mid-Cap)

Revenue Generating: 100%

Profitable: 25%

Average Beta: 1.51

Critical Risk Factors:

Uranium Price Risk (7/10): 62.5% are uranium miners highly correlated to spot price (~$65/lb, down from highs). Uranium prices facing tariff uncertainty and supply concerns.

Production Risk (6/10): UEC, DNN, UUUU face ISR mining permitting delays. SMR has first-of-kind technology execution risk despite NRC approval.

Sector Concentration Risk (6/10): Heavy uranium mining exposure (50% of portfolio) with limited diversification. All holdings correlated to nuclear sector sentiment.

Geopolitical Risk (6/10): U.S. uranium tariff uncertainty affecting supply chains. Kazakhstan supplies 40% of global uranium, creating concentration risk.

Financial Risk (5/10): 75% unprofitable and burning cash. Need sustained higher uranium prices for profitability.

Potential Upside: 100-300% returns if uranium bull market resumes. Growing government support for domestic uranium production and SMR deployment with Big Tech partnerships.

Recommended Allocation: 10-20% of total portfolio

Suitability: Growth investors comfortable with commodity exposure

Portfolio 3: LOW RISK - CONSERVATIVE GROWTH

Target: Steady growth with established nuclear and energy companies

Expected Volatility: Low to Moderate | Time Horizon: 1-3 years

Portfolio Characteristics:

Average Risk Score: 40.9/100 (Low-Moderate)

Average Market Cap: $38.4B (Large-Cap weighted)

Revenue Generating: 100%

Profitable: 87.5%

Average Beta: 1.23

Critical Risk Factors:

Market Valuation Risk (5/10): CEG (P/E 38.17) and VST (P/E 38.79) trade at elevated multiples after 40-450% YTD gains. Potential for profit-taking if growth disappoints.

Regulatory/Policy Risk (4/10): CEG’s Three Mile Island restart faces regulatory scrutiny. BWXT depends on government contracts (DoD, DoE). All benefit from pro-nuclear policy but vulnerable to changes.

Execution Risk (3/10): CEG and VST operate proven nuclear/power assets. CW and TLN are diversified aerospace/defense businesses. BWXT is established naval nuclear contractor. Minimal execution risk.

Financial Risk (2/10): 87.5% profitable with positive cash flow. Strong balance sheets generating significant EBITDA. Minimal financial stress.

Potential Upside: 30-80% returns over 1-3 years from nuclear growth theme. AI data center demand driving CEG and VST growth. Steady dividend income potential.

Recommended Allocation: 15-30% of total portfolio

Suitability: Conservative to moderate investors seeking income/growth blend

Comparative Risk Metrics

Key Investment Considerations

Market Context (October 2025):

Nuclear stocks surged 40%+ YTD as Microsoft, Amazon, and Google signed multibillion-dollar AI data center power agreements

Uranium prices declined to ~$65/lb from highs due to tariff uncertainty

U.S. targeting 4x increase in nuclear capacity to 400 GW by 2050

Technology companies projected to invest $250B in AI infrastructure in 2025

Critical Warnings:

All three portfolios are sector-concentrated (nuclear/energy) and should represent only a portion of a diversified portfolio

High Risk portfolio carries extreme regulatory and development risk - suitable only for aggressive investors with 5+ year horizons

Moderate Risk portfolio is highly sensitive to uranium price movements and geopolitical factors

Low Risk portfolio trades at elevated valuations after strong YTD performance