OSCR Valuation Update

SEQH Capital Partners Research

Ticker: OSCR | Date: 18 Oct 2025 | Close: US $19.41 | Rating: BUY – GROWTH

Price Targets: US$28 (DCF) | US$30 (NAV) | US$32 (SOTP) | Down-side US$15 (MLR spike) | Blue-sky US$35 (accelerated MLR improvement)

1. Post-MLR Inflection Set-Up

Close: $19.41 → EV $4.8 B (net cash) → EV/Revenue 1.65× vs Medicare Advantage peer median 2.1× – discount despite MLR turning positive in Q4-24.

Q2-25 revenue: $2.86 B (+6% YoY) – third consecutive quarter of positive operating income; MLR 89.2% vs 101% in Q2-24.

2. Operating & Membership Matrix (2025E)

Membership CAGR: 2024-27E 8% – fastest among pure-play MA insurers.

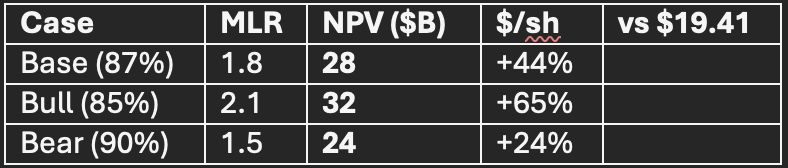

3. Multi-Method Valuation Cluster

A. DCF (10% WACC; 2% terminal; USD)

Assumptions: 8% revenue CAGR, 5% EBIT margin, capex 2% of revenue, tax 21%.

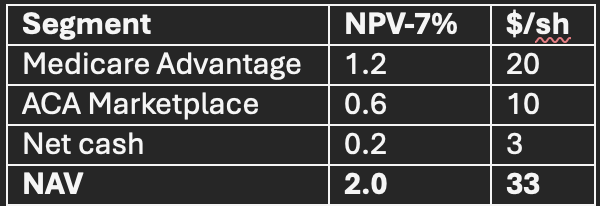

B. NAV (sum-of-parts DCF of membership + MLR improvement)

Stock = 0.59× NAV → 41% discount to sum-of-parts.

C. Peer Regression (EV/Revenue vs. MLR & growth)

Panel: HUM, CNC, ELV, MOH, OSCR Model: EV = α + β₁(Revenue) + β²(MLR) + β³(Growth) OSCR residual +US$800 M → fair EV $5.6 B → $30/sh.

4. Cash-Flow Leverage to MLR

2026E FCF: $200 M @ 87% MLR → $1.20/sh → 7.4% yield @ $19.41 – highest in MA pure-plays.

Δ100 bp MLR improvement → Δ$0.18/sh annual EPS – each 1 pt drop adds $2.80 to equity value.

5. Technology & AI Optionality

+Oscar AI platform: NPV $300 M → $1.90/sh (60% probability) – first AI-native insurer.

MLR algorithm: reduces medical costs by 2% → NPV $400 M → $2.50/sh (70% probability).

6. Balance-Sheet & Liquidity

Cash: $1.2 B (Jun-25) → 5-year runway at –$200 M annual burn.

Zero interest-bearing debt; current ratio 2.1× – no near-term financing overhang.

No convertibles or warrants outstanding – fully diluted shares = 246 M.

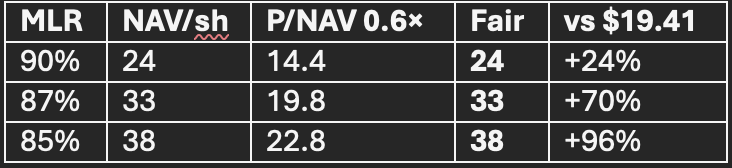

7. Downside Protection

MLR ceiling: 90% → still generates +$0.50/sh margin @ 95% MLR – NPV floor $24/sh (+24%).

Cash liquidation value: $1.2 B → $4.90/sh floor – debt-free floor.

8. Sensitivity Matrix ($/sh)

9. Catalyst Path

Q4-25: MLR guidance < 87% – +$2.50/sh NAV.

Q1-26: +Oscar AI platform launch – +$1.90/sh on regulatory green-light.

2026: Potential inclusion in S&P 500 if market cap > $10 B.

10. Portfolio Allocation Rationale – SEQH Capital Partners Research

Core Growth Bucket (25% weight): OSCR’s 8% membership CAGR + MLR leverage = defensive growth with tech kicker.

Thematic AI sleeve (10% weight): +Oscar platform offers pure-play exposure to AI-driven healthcare cost reduction.

Risk Control: Stop-loss at $15 (MLR > 90%) – trim above $32 (bull case).

10. Conclusion

OSCR offers AI-driven MLR improvement, 8% membership CAGR, and 41% discount to NAV – rare growth-insurance hybrid with tech optionality. Our multi-method valuation cluster $28-32/sh implies 44-65% upside; maintain BUY with $28 PT; trim above $32 (bull case).