Renergen Limited Earnings and Business Outlook Recap

11/3/25

Renergen Limited (JSE: REN | ASX: RLT)

Advanced Analytical Tear Sheet | SEQH Capital Research | November 3, 2025

Investment Thesis

Renergen is emerging as a global critical materials leader through its fully financed Virginia Gas Project (South Africa), which hosts world-leading helium concentrations (3–4%) and renewable methane reserves. With Phase 2 approved and financed, Renergen transitions from development-stage to transformative scale-up, targeting 16x production growth and positioning among the top five global helium producers.

High-conviction opportunity in an under-supplied, geopolitically strategic commodity essential for semiconductors, AI, energy, and healthcare.

Strategic Asset Overview

Location: Free State, South Africa, over 187,000 hectares within the Vredefort Crater.

Helium Reserves: 13.6 Bcf proven (highest global grade, 3–4% vs 0.1% Qatar).

Feedstock Quality: >90% methane purity; biogenic origin supports renewable gas designation.

Competitive Moat: 35x typical global helium concentration, non-U.S./Qatar producer with full commercial scale potential.

Key Strategic Edge: Unique combination of world-class geology, government backing, secured financing, and long-term offtake contracts.

Financial Highlights

MetricH1 FY26YoY GrowthFY25CommentRevenueR29.09M+13.6%R52.1MPre-scale rampNet LossR134.5M—R236.1MExpansion phase costsOpexR112.1M+39%—Build-up periodInterest Exp.R75.4M+199%—Financing for Phase 2Loss per ShareR0.91↑ from 0.46—Trough year before inflection

Phase 2 Targets:

Revenue Potential: $409M/year

EBITDA Margin: ~65%

Payback: ~4.4 years post-commissioning

Reserve NAV: ~$3.0B net (20x market cap)

Phase 2 Expansion Economics

Helium Output: 5,000 kg/day ≈ $146M annual revenue @ $450/MCF

LNG Output: 800 t/day ≈ $263M annual revenue @ $900/t

CapEx: $1.16B (65% debt / 35% equity)

Financiers: $500M (U.S. DFC), $250M (Standard Bank), $30M (ASP Isotopes)

EPC Partners: Chart Industries, WBHO, Aurex (He4u Consortium); Saipem for FEED

65% of helium output secured via take-or-pay contracts with Linde, Messer, Helium 24, and iSi.

Market Position & Macro Tailwinds

Helium Market (2025): $3.36B value, prices +18% YoY to $450/MCF. Tight supply supported by semiconductor and AI supercycle demand.

LNG Market (South Africa): Energy transition catalyst; domestic demand to reach 870 PJ by 2032. LNG priced ~25% below diesel, serving transport and industrial sectors.

Demand Drivers:

Semiconductors → 24% market share, 5x demand growth by 2035.

Healthcare & Aerospace → 25% of market share by 2030.

Industrial Applications → Welding, leak detection, cryogenics.

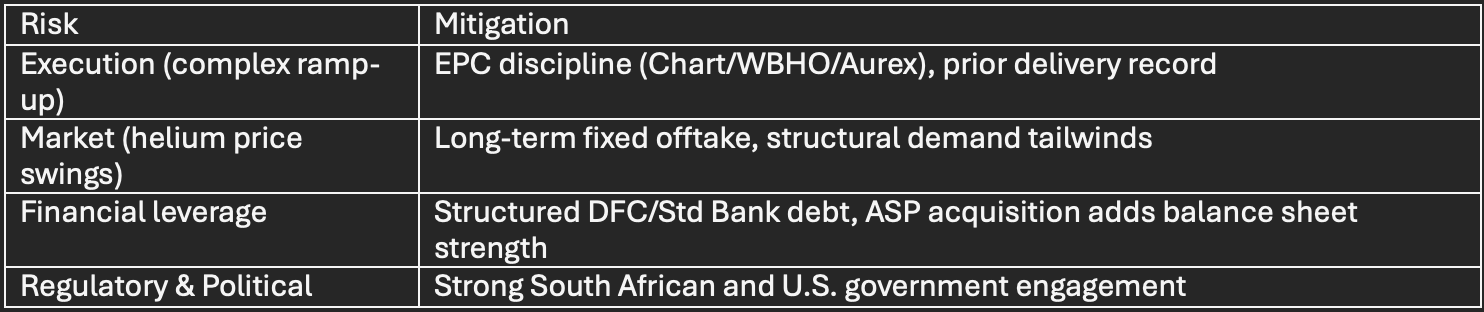

Risk & Mitigation Summary

Valuation & Outlook

Estimated Net Helium Asset Value: ~$3.0B

Implied Upside: >20x vs current $130M market cap (R16.38/share)

Price Target Range: $25–40/share by 2030

Key Catalysts:

ASP Isotopes merger (Q3 2025 close)

Phase 2 commissioning and ramp-up

U.S./EU semiconductor and LNG expansion tailwinds

Conclusion: Renergen offers de-risked execution, strategic backing, and unmatched asset quality within critical energy and materials markets. A rare, high-conviction exposure to helium scarcity and the energy transition.

ASP Isotopes Acquisition Impact (NASDAQ: ASPI)

Transaction Snapshot

Structure: Scheme of Arrangement under SA law; 99.8% approval, expected Q3 2025 close.

Strategic Rationale: Vertical integration of helium, LNG, and enriched isotopes across semiconductor and healthcare sectors.

Financing: Combined leverage of DFC ($500M) and Standard Bank ($250M) ensures Phase 2 completion.

Financial Synergy Outlook

Integration Advantages:

Combined technology platform unites helium and isotope production.

Expands footprint into U.S. capital markets, unlocking valuation uplift.

Creates a cash-generating critical materials player with >$300M EBITDA run-rate potential by 2030.

SEQH Capital View:

The ASP–Renergen pairing forms a vertically integrated, government-backed critical materials powerhouse. Execution of Phase 2 and merger synergies together support a re-rating opportunity exceeding 10x current valuations over the next five years.

FULL 7-PAGE REPORT ON THE ABOVE RESEARCH:

Includes effect of strong Renergen earnings on acquisition by ASP Isotopes.