Renergen Virginia Gas Project Analysis

11/10/25

Virginia Gas Project: Transformational Asset in Global Helium and Gas Markets

Project Genesis and Geological Context

The Virginia Gas Project, operated by Tetra4 (a Renergen subsidiary), covers 187,000 hectares across Welkom, Virginia, and Theunissen in South Africa’s Free State province, making it Africa’s only onshore petroleum production asset and South Africa’s sole source of indigenous natural gas and helium. The concession sits within the Vredefort Dome, a 2 billion-year-old impact crater, endowing the region with radiogenic helium sourced from uranium- and thorium-rich basements and biogenic methane produced by bacterial metabolism in fractured Witwatersrand rocks. This unique geology confers helium concentrations averaging 2.0–2.5%, over 10x global averages, and generates a renewable (biogenic) methane stream, positioning the project as one of the world’s richest unconventional helium accumulations.

Phased Development - Specifications and Growth Potential

Phase 1 (Commissioned Q3 2022; ~$60M capex):

Nameplate: 350 kg/day liquid helium, 2,500–2,700 GJ/day LNG (~50 tons/day).

Infrastructure: 52 km pipeline, cryogenic plant.

Status: Operational, with first commercial helium shipments in March 2025 after extended technical setbacks (cold box failure, integration delays, workaround Dewar solutions).

Function: Meets all domestic helium requirements; excess exported. LNG replaces costly diesel for domestic customers, improving energy security.

Phase 2 (Under development; $1.16B capex; Target completion 2027):

Nameplate: 4,200 kg/day helium (+34,400 GJ/day LNG, 868,000 tpy), a 12–14x increase over Phase 1.

Infrastructure: 350 wells, 450 km gathering pipeline, expanded processing/cryogenic capacity.

Impact: Once at full ramp, Virginia will deliver ~10% of global helium demand and provide critical new gas for South Africa, where supply shortages are acute.

Resource Base and Scale

Sproule’s 2021 independent review established transformative upgrades over prior evaluations:

Proven + probable (2P) helium reserves: 13.6 bcf (up 298% since 2019 update)

Proven + probable (2P) methane: 407 bcf

Only 14% of acreage independently assessed; rest remains prospective.

This extraordinary helium endowment is validated by persistent radiogenic generation and near-continuous resource renewal, a competitive advantage rarely matched globally.

Capital Structure and Strategic Funding

Debt commitments secured: $500M (US DFC), $250M (Standard Bank), supporting a 65–75% debt/25–35% equity target.

Key equity partners: Central Energy Fund (~$55M for 10% of Tetra4, R10B implied valuation), Mahlako Gas Energy, with further Nasdaq IPO proceeds planned.

ASP Isotopes is acquiring Renergen at a 41% premium, a substantial endorsement after rigorous due diligence.

Liquidity and funding challenges remain nontrivial, especially post-technical delays in Phase 1, but lender, government, and strategic partner support is robust.

Technical and Commissioning Challenges

Phase 1 suffered major cold box vacuum loss (mid-2023) and protracted OEM integration delays, impacting both cash flow and investor confidence.

As of Q1 2025, first liquid helium sales were achieved, but LNG and helium throughput remain below nameplate, Phase 1C optimizations are still required for full steady-state operations.

Recent focus is on technical stabilization, additional well connections, and system reliability, with anticipated operational inflection as maintenance and upgrades are completed.

Offtake and Revenue Certainty

~65% of Phase 2 helium contracted with blue-chip global buyers: Linde, Messer, Helium24, and iSi (SOL S.p.A.), 10–15 year terms, fixed USD/MCF with CPI escalation; balance available for spot market upside capture.

LNG offtake benefits from rising domestic demand amid regional gas scarcity and transition from coal to cleaner fuels.

Total project EBITDA, at full Phase 2 ramp and current price assumptions, is guided at ~$300–340M/year, meaningfully de-risked by long-term contracts and market structure.

Market and Strategic Advantages

Helium market: $3.4B in 2025 with 400%+ price surges during acute global shortages, Virginia’s production brings diversification and security to an industry dominated by US, Qatar, and (emerging) Russian supply.

End markets: Semiconductors (21% of demand), medical imaging, quantum computing, fiber optics, and space, core drivers for sustained helium demand and price resilience.

South Africa’s regulatory fast-tracking (SIP status) and US/EU recognition of helium as a critical mineral create a uniquely valuable geopolitical and supply chain hedging position for Virginia.

ESG, Environmental and Community Impact

Producing ultra-high-purity helium with much lower associated CO₂ intensity (due to elevated gas concentrations and absence of heavier hydrocarbons); credible sustainability and ESG narrative.

Job creation: ~360 temporary, 160 permanent roles expected in region, plus downstream benefits to energy-reliant industries.

Community and environmental engagement ongoing; most EIA appeals addressed with two remaining under review for climate/seismic impact.

Financial Performance and Valuation Insight

FY2025 revenue: R52.1M (80% YoY growth but still at operational loss as plant ramps).

Market cap (Nov 2025): $110–115M; forward EBITDA multiple at full Phase 2: ~0.34x (vs 8–10x global comps).

Strategic equity deals (e.g., CEF) have valued Tetra4 at $550M, 5x above market, highlighting disconnect and latent embedded value for informed investors.

The pending ASP Isotopes acquisition not only crystallizes a valuation floor but also affords ASP/Renergen shareholders long-run upside exposure within a diversified global critical-gas champion.

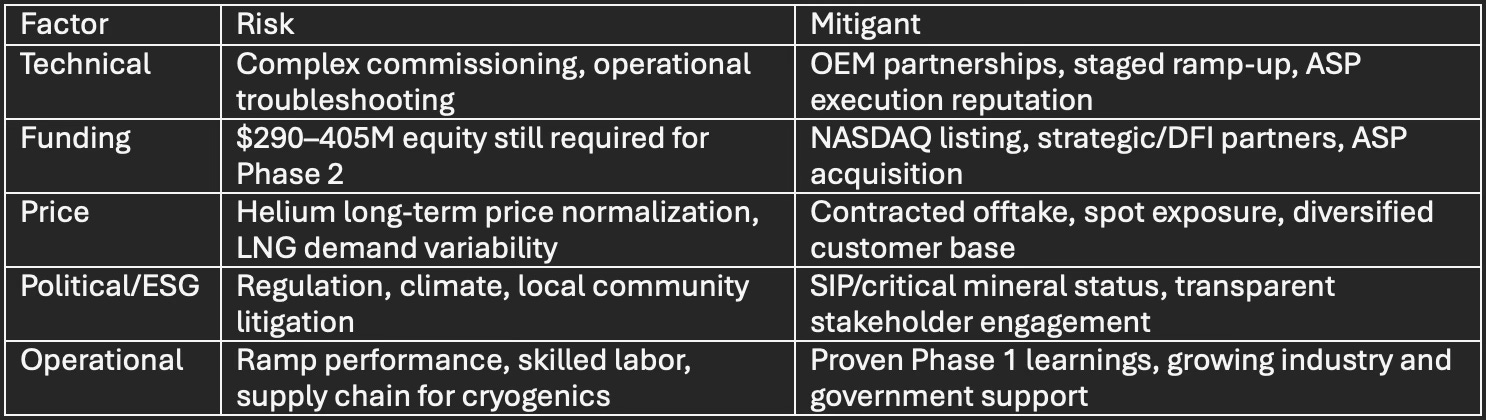

Project Execution and Risk Matrix

Conclusion: High-Conviction, Asymmetric Opportunity

The Virginia Gas Project delivers transformative helium and LNG scale, deep structural demand alignment (semis, medical, quantum computing), and critical supply diversification for a fundamentally tight global market. Technical delays and capital intensity have depressed Renergen’s valuation, positioning it with one of the deepest value disconnects globally among pre-profit resource assets. The ASP deal both normalizes funding and validates the exceptional strategic worth of this project.

For institutional and professional audiences, this is a classic asymmetric, high-reward setup: Unique geology and technical validation; global offtake and pricing power; government and strategic capital alignment; and a clear operational path to $300M+ annual EBITDA profile. The project’s success, or failure, defines Renergen’s value, while the strategic optionality created by ASP, DFI, and CEF involvement substantially improves the risk/reward skew for sophisticated investors and supply chain participants.

FULL 12-PAGE REPORT ATTACHED BELOW.

INCLUDES IN_DEPTH VALUATION DETAIL ALONG WITH SEQH CAPITAL FULL INVESTMENT THESIS AND IMPACT ON ASP ISOTOPES.