Terrestrial Energy (IMSR) Discovery Analysis

11/15/25

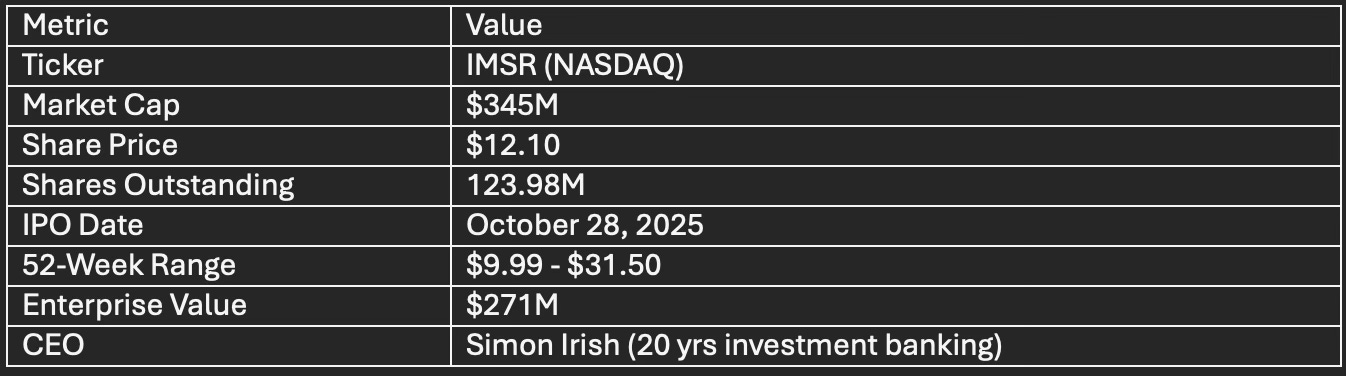

TERRESTRIAL ENERGY INC. (IMSR)

Date: November 15, 2025 | Analyst: SEQH Capital Research Team | Rating: BUY

INVESTMENT THESIS

Terrestrial Energy represents a compelling entry point into advanced nuclear energy at an attractive valuation. The company’s molten salt reactor technology delivers superior 44-48% thermal efficiency versus 30-35% for legacy designs while maintaining fuel supply optionality through Standard Assay Low-Enriched Uranium utilization. Recent regulatory approvals from the Canadian Nuclear Safety Commission and U.S. Nuclear Regulatory Commission, combined with DOE Advanced Reactor Demonstration Program selection, materially de-risk the pathway to commercial deployment. Current market capitalization of $345 million appears deeply discounted relative to addressable market opportunity and peer valuations, suggesting asymmetric return potential.

COMPANY OVERVIEW

Terrestrial Energy completed its business combination with HCM II Acquisition Corp. with minimal redemptions (<1%), raising $292 million in gross proceeds. The company operates as a pre-revenue development-stage advanced reactor developer focused on the Integral Molten Salt Reactor (IMSR) for grid, industrial, and data center applications.

TECHNOLOGY DIFFERENTIATION

The IMSR integrates all primary systems within a sealed vessel operating at atmospheric pressure, eliminating external piping while enabling direct industrial process heat delivery at 585°C. The 390 MW electrical design (two 195 MW core-units per plant) achieves material construction timeline reduction—under 4 years versus 10+ years for conventional nuclear—through factory-fabricated modular construction. Critically, the IMSR utilizes Standard Assay LEUI fuel (<5% U-235 enrichment), providing immediate access to established uranium supply infrastructure while avoiding the HALEU bottleneck constraining NuScale, Kairos, and TerraPower deployments.

Comparative analysis: NuScale (77 MWe/module, lighter water, limited process heat), Kairos Power (HALEU dependent, regulatory earlier stage), TerraPower Natrium (HALEU required, sodium handling complexity).

REGULATORY PATHWAY (DE-RISKING EVIDENT)

The progression through dual-nation regulatory review and DOE program selections substantially de-risks versus earlier-stage competitors. NRC approval in September 2025 represents the first commercial molten salt design Principal Design Criteria ruling, establishing foundational safety requirements across all major systems.

MARKET OPPORTUNITY & TAILWINDS

Grid-Scale & Data Centers: U.S. nuclear generation projected to grow 27% post-2035, with data center electricity demand expected to quintuple by 2035 (reaching 176 GW per Deloitte). Tech giants—Amazon (5 GW committed), Google (500 MW with Kairos), Microsoft—actively pursuing nuclear power agreements. Data center power economics favor constant baseload versus intermittent renewables.

Industrial Decarbonization: Global industrial sector comprises 30% of energy demand, with process heat applications at 400-950°C currently 95%+ fossil fuel-dependent. IMSR’s 585°C output enables direct heat supply to refining, chemicals, ammonia synthesis, and hydrogen production—a multi-gigawatt TAM over multi-decade deployment horizon.

SMR Market: Small modular reactor market projected at $5.18B by 2035 (42.31% CAGR from 2024), with LCOE targeting $50-70/MWh versus $110-228/MWh for recent conventional nuclear builds. IMSR’s efficiency advantage provides structural cost benefit.

COMPETITIVE POSITIONING

Terrestrial Energy commands a differentiated position within the advanced reactor ecosystem. First-mover advantage belongs to NuScale ($5.2B market cap, first NRC-certified design), while sector leader Oklo trades at $19B—both substantially above IMSR. However, IMSR’s molten salt technology delivers efficiency and process heat capabilities NuScale’s light water design cannot match. Fuel supply independence versus HALEU-dependent competitors (Kairos, X-energy) represents a material supply chain advantage. Texas A&M commercial deployment partnership and Westinghouse fuel contract provide tangible first-of-a-kind pathway visibility.

FINANCIAL PROFILE & VALUATION

Pre-revenue status reflects development-stage positioning with capital deployment focused on regulatory engagement, engineering advancement, and supply chain establishment. Minimal negative equity position warrants evaluation within context of nuclear development model, substantial upfront investment precedes revenue generation. $292M capital raise provides adequate runway; however, first-of-a-kind plant construction will necessitate multi-billion dollar project-level financing or additional raises by mid-to-late 2020s.

CATALYSTS & INFLECTION POINTS (12-24 MONTHS)

Near-term (6-12 months): NRC construction and operating license pathway advancement; announcement of additional DOE funding; first customer offtake agreement execution; Texas A&M site permitting commencement.

Medium-term (12-24 months): NRC licensing milestone announcements; first major industrial or data center customer partnership; Westinghouse fuel plant construction commencement; additional U.S. or international deployment site selections.

Each represents a binary outcome with material stock price implications. Positive catalysts could drive 3-5x valuations toward peer multiples; regulatory delays or project setbacks present meaningful downside risk.

RISK ASSESSMENT

Execution Risk (High): First-of-a-kind nuclear projects historically exceed budgets by 102.5% and experience extended timelines. IMSR targets early 2030s deployment; regulatory or technical delays would significantly impact returns.

Funding Risk (Medium): Current capital sufficient for regulatory progression; commercial deployment requires multi-billion dollar project financing. Future equity dilution or debt-dependent structure represent concerns.

Technology Validation Risk (Medium): Molten salt reactors demonstrate decades-old chemistry but lack extended commercial operation data. Long-term corrosion behavior and operational reliability require real-world validation.

Market Adoption Risk (Medium-High): Commercial pipeline remains nascent. First-of-a-kind project execution and customer willingness to adopt emerging technology versus proven alternatives constitute execution dependencies.

Regulatory Risk (Medium): Policy shifts across administrations could impact funding or timeline. NRC process could surface unexpected technical requirements.

VALUATION & RECOMMENDATION

Current Valuation: $345M market cap reflects 61.6% drawdown from $31.50 IPO-period highs, potentially creating attractive entry opportunity. 52-week trading range $9.99-$31.50 suggests market volatility rather than negative company developments.

Comparable Multiples: NuScale ($5.2B), Oklo ($19B), TerraPower (private). IMSR’s regulatory advancement and fuel supply advantage support premium to earlier-stage competitors, yet remain discounted to leaders.

Investment Horizon: 5-7 years minimum. Near-term share price pressure likely; material upside requires successful regulatory progression and commercial deployment pathway validation.

Position Sizing: Recommend 1-3% portfolio allocation for qualified investors with appropriate risk tolerance. Venture-style allocation framework appropriate given binary outcome characteristics. Average into position on regulatory milestone achievements.

Rating: BUY | Target Allocation: 1-3% | Price Target: $28-35 (12-24 month horizon, subject to catalyst achievement)

KEY METRICS TO MONITOR

Track quarterly progress on: (1) NRC licensing pathway advancement, (2) DOE ARDP project milestone achievement, (3) Customer offtake agreement announcements, (4) Supply chain partnership expansion, (5) Capital burn rate and cash runway, (6) Competitive technology readiness announcements, (7) Policy environment shifts affecting nuclear support.

FULL 15-PAGE INVESTMENT DISCOVERY ANALYSIS REPORT BELOW: