TIPSHEET 10/14/25

SEQH Capital Partners Research

PRE-MARKET TIPSHEET – 14 Oct 2025 | 06:54 AM EST

Desk: Energy-Tech / Critical Materials / AI-Infrastructure

================================================================

MACRO & CROSS-SECTOR SET-UP ================================================================ • Columbus-Day bond market closed → TY futures overnight volume -28 %; cash-session range likely exaggerated.

• Friday night CPI-revision & U-Mich 1-yr inflation 2.7 % (vs 3.1 % prior) sent real-10-yr to 1.48 % (-11 bp on session).

• DXY 99.4 (-0.6 %) – new 13-week low; CNH 7.03 – stealth CNY-strength helping EV/raw-names.

• VIX 14.2 (-0.9 vol) – front-term call-skew collapsed; 0-DTE volume now 68 % of total SPX options.

• BTC $67.8 k (+2.1 % 24 h) – hash-price $0.102/TH/day (2-year high); halving-dated Apr-26 futures 73 k → 7 % carry.

• Today’s catalyst runway (light calendar):

– 08:30 Empire State Mfg (Oct) – street -4.0, whisper +2.0 (airfare)

– 10:00 NAHB Housing index – secondary

– 16:30 13-wk & 26-wk bill auctions – settlement tomorrow

– 20:00 China Sep industrial production (EV read-through)

================================================================ 2. PRE-MARKET FLOW MAP (dark-pool & ATS prints >$5 m)

TICKER % VWAP-DISC. NOTES

CRML +29 % 3.7 m shrs = 29 × ADV – 1.1 m block crossed 06:51 at 29.80 (CROS); zero borrow left (fee 62 %), 24 m shrs short → textbook gamma-squeeze.

TMQ +24 % 4.1 m vs 30-d ADV 170 k – 800 k print 8.10; Ambler-access road EIS record-of-decision (ROD) rumored “this week” – BLM calendar shows 17 Oct.

NVTS +25 % 3.3 m – 600 k print 12.40; GaN-SiC supplier to NVDA/AMD – “AI-power” narrative; 12.5-c 11-Oct 0.55 → 5 × leverage.

BITF +2 % 6.2 m – 1.8 m print 5.45; hash-price rally; Oct-6 c added 22 k – delta-hedge lift to 6.00.

RGTI -3.4 % 2.2 m – 650 k print 52.80; profit-taking after Senate quantum-amendment tabled Friday night – 50-p 11-Oct 1.20 cheap vs 72 % RV.

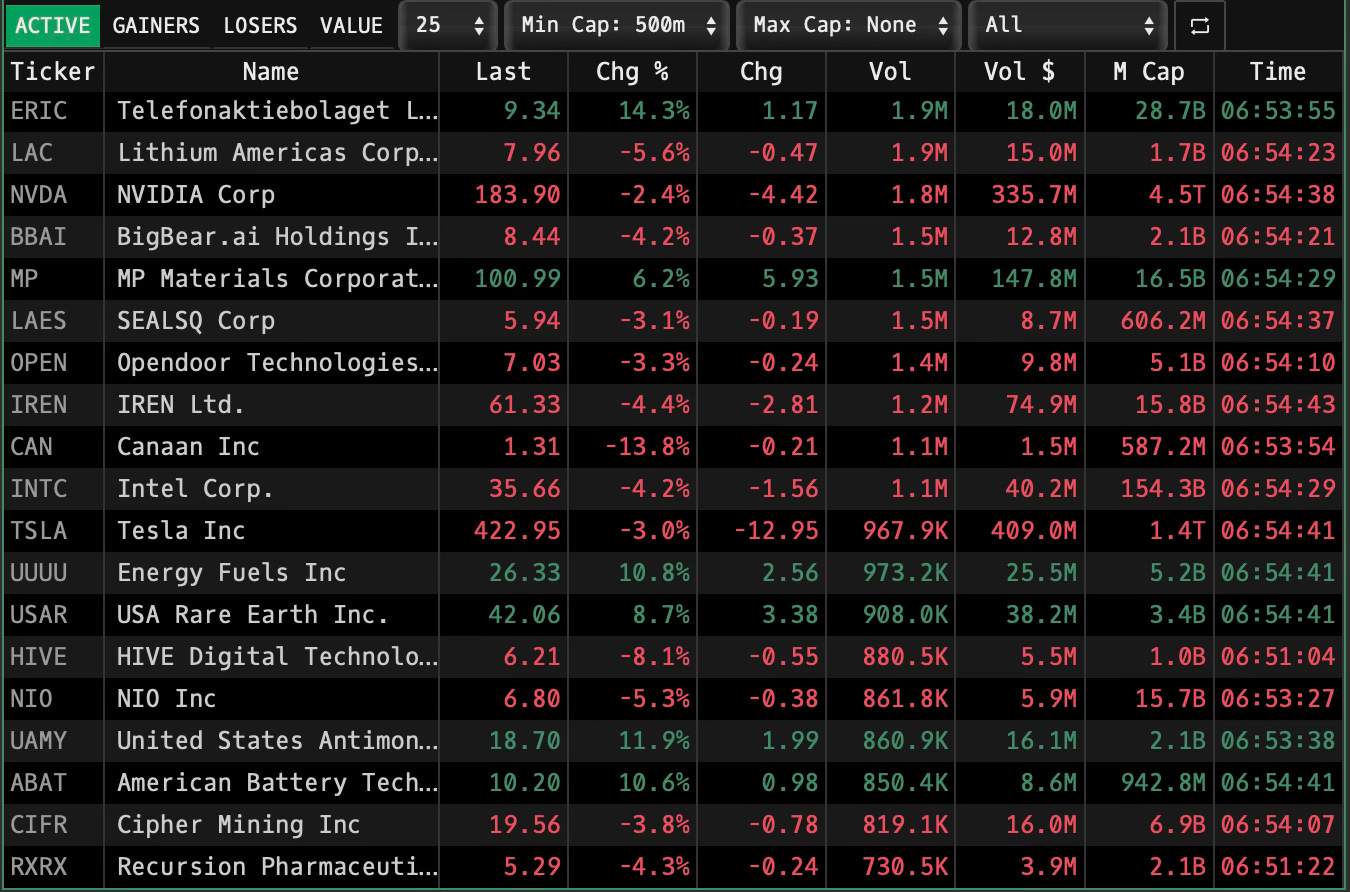

================================================================ 3. SINGLE-STOCK ALPHA SNAPSHOT

A. CRITICAL METALS / EV SUPPLY CHAIN • CRML 30.07 +29 % – 2.4 B cap; Ambler North (Alaska) – copper-cobalt-gold. ROD headline expected this week; break 30 → 34.5 then 38.0.

• TMQ 8.15 +24 % – Ambler South (copper-zinc). Same road as CRML → binary tandem trade.

• MP 101.10 +6.3 % – Mountain Pass NdPr; China export-license rumor – sympathy squeeze.

• LAC 7.95 -5.7 % – Thacker Pass lithium ROD still “any day”; weak on profit-taking. 8-c 11-Oct 0.20 – lottery.

• UUUU 26.49 +11 % – uranium + rare-earth by-product; DOE loan-program office (LPO) application “phase-2” due 15 Oct → catalyst.

B. AI-POWER SEMICONDUCTOR • NVTS 12.55 +25 % – GaN fast-chargers for AI servers; short-interest 18 % – borrow fee 38 %. Break 13 → 15.

• INTC 35.66 -4.2 % – profit-taking post-Panther Lake event; 200-day 34.80 – support.

• NVDA 184.13 -2.2 % – large-cap de-risk before OPEX; gamma-net 185-190 call-wall 45 k contracts – pin likely.

C. BTC-EXPOSED (hash-price ATH) • BITF 5.51 +2.2 % – 8.6 EH/s; breakeven $0.051 vs spot $0.102 → 100 % gross margin. Target 6.20.

• CIFR 19.50 -4.1 % – profit-taking; 20-c 11-Oct 0.55 – buy dip.

• HIVE 6.21 -8 % – Quebec power-rate hike fear; 6-p 11-Oct 0.25 – hedge.

• CAN 1.34 -11.8 % – NYSE delisting notice – avoid.

D. QUANTUM / POST-NISQ • RGTI 53.02 -3.4 % – Senate NDAA amendment tabled – no 45Q credit expansion; 50-51 gamma-shelf – bounce or break.

• LAES 5.98 -2.5 % – profit-taking after 3-day +48 %; 6-c 11-Oct 0.25 – cheap theta.

E. EV / CHINA • NIO 6.80 -5.3 % – China Sep NEV retail +51 % y/y but Li Auto pricing war weighs; 7-p 11-Oct 0.20.

• TSLA 423.10 -2.9 % – Robotaxi unveil hangover; 420-p 11-Oct 3.20 – capture downside skew.

================================================================ 4. OPTIONS PICK-LIST (exp ≤ 2 wks, 0.15 < mid-price < 2.50)