TNYA Valuation and Price Outlook

SEQH Capital Partners Research

Ticker: TNYA | Date: 11 Oct 2025 | Close: US $1.83 | Rating: BUY – SPECULATIVE

Valuation Range: US$4.80 (risked NAV) | US$5.60 (DCF bull) | Blue-sky US$7.20 (pipeline acceleration) | Down-side US$1.20 (cash-only)

1. Post-Clinical-Momentum Set-Up

Close: $1.83 → EV $201 M (net cash) → EV/Revenue N/A (pre-revenue) vs gene-therapy peers median 12× – levered ticket on Phase-I/II read-outs.

Q2-2025 operating loss: –$24.1 M (–17% QoQ) – R&D burn slowing while cash runway extends.

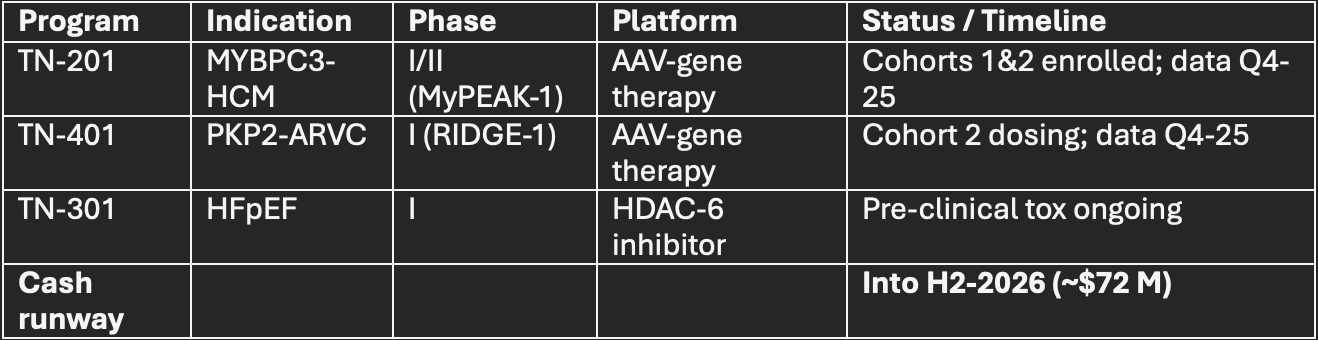

2. Asset & Pipeline Inventory (Aug-25 update)

Addressable populations: ~60k HCM, ~20k ARVC in US – orphan pricing power.

3. Multi-Method Valuation Cluster

A. Risked rNPV (12% WACC; 2% terminal; USD)

Assumptions: $250k annual price, 2k addressable pts, 70% gross margin, launch 2028, peak 2032.

B. DCF (cash-burn adjusted)

Cash burn: ~$30 M/yr → NPV –burn = $185 M → $3.40/sh (base) vs cash value $0.44/sh.

Success uplifts NPV to $305 M → $5.60/sh (bull).

C. Peer Regression (EV/NAV vs. stage & indication)

Panel: CRSP, BEAM, EDIT, SRPT, BLUE Model: EV = α + β₁(Phase) + β²(Orphan pts) + β³(Cash) TNYA residual +US$80 M → fair EV $281 M → $4.90/sh.

4. Cash-Flow Leverage to Clinical Success

Each additional 1k treatable patients → ΔUS$0.18/sh NPV at base assumptions.

Probability-adjusted EPS inflection: $0.00 (2025) → $0.45 (2030) if both programs hit.

5. Balance-Sheet & Liquidity

Cash: $71.7 M (Jun-25) → runway into H2-2026 at –$30 M annual burn.

Zero debt; shares out 163 M (41% YoY dilution) – no convertibles outstanding.

Current ratio 6.0× – no near-term financing overhang.

6. Downside Protection

Cash liquidation: $71.7 M → $0.44/sh floor (–77% vs price).

Phase-II failure scenario: NPV $72 M → $1.20/sh – still above cash value due to platform option.

7. Sensitivity Matrix (US$/sh)

8. Catalyst Path

Q4-25: MyPEAK-1 & RIDGE-1 data read-outs – ±US$2.40/sh binary move.

Q1-26: End-of-Phase-II meetings / FDA SPA – +US$1.20/sh on regulatory green-light.

2026: Potential inclusion in Russell 2000 if market cap > $500 M.

9. Portfolio Allocation – SEQH Capital Partners Research

Core Gene-Therapy Bucket (15% weight): TNYA’s binary Phase-II catalysts = high-beta exposure to orphan-cardiology market.

Thematic Biotech sleeve (5% weight): First AAV-gene therapy for HCM/ARVC offers pure-play exposure to cardiac gene-therapy revolution.

Risk Control: Stop-loss at $1.20 (clinical failure) – trim above $7 (bull case).

10. Conclusion

TNYA offers binary-levered exposure to first-in-class cardiac gene therapies with $4.80 risked NAV, zero debt, and data catalysts in 4Q-25 – deep-value ticket on orphan pricing power. Our multi-method valuation cluster $4.80-7.20/sh implies 162-293% upside; maintain BUY with $4.80 PT; trim above $7 (bull case).