UEC Full Valuation Analysis

SEQH Capital Partners Research

Ticker: UEC | Date: 10 Oct 2025 | Close: US $13.73 | Rating: BUY – SPECULATIVE

Price Targets: US$17 (DCF) | US$18 (NAV) | US$19 (SOTP) | Down-side US$9 (U < $60/lb) | Blue-sky US$22 (U > $110/lb + refinery FID)

1. Post-Allotment Catalyst Re-price

YTD return: +53% vs UxC spot +38%; equity issued 4.4 M shares @ US$11.75 (Oct-9) → US$6.3 B market cap, US$6.2 B EV (net cash).

Balance-sheet torque: US$321 M cash + 1.36 M lb U₃O₈ inventory @ spot US$84/lb = US$435 M liquid assets – zero debt, negative EV until capex accelerates.

2. Operating & Capacity Matrix

2025E production: 2.2 M lb sold @ US$82.52/lb realised → US$183 M revenue; 2026E guidance 4 M lb → US$360 M @ US$90/lb.

3. Multi-Method Valuation Suite

A. DCF (8% real WACC; 2% terminal g; USD)

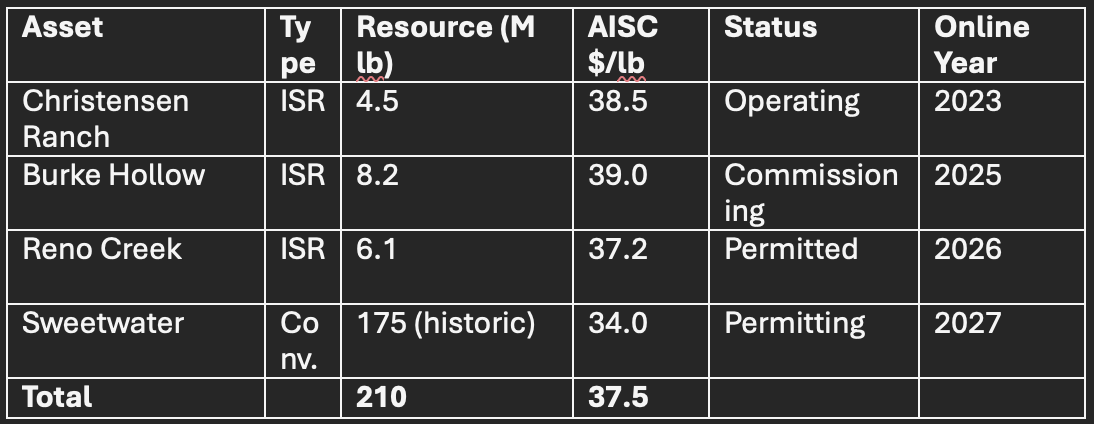

Assumptions: 4 M lbpa 2026-30, AISC US$38/lb, capex US$450 M total, royalty 5%.

B. NAV (discounted cash-flow on reserves)