Unit Economics of ASPI

ASP Isotopes Inc. (ASPI) - Unit Economics Reality Check

SEQH Capital Research

November 2, 2025

Executive Summary: Where’s the Revenue?

ASPI doesn’t break out unit economics by business line in SEC filings, only consolidated numbers with vague segment labels. After digging through every 10-Q, 10-K, and press release, here’s what the numbers actually show versus what management promotes.

The Bottom Line: FY 2024 revenue was $4.1M, with essentially all of it from PET Labs radiopharmacy operations, not the proprietary isotope technology justifying the $1B+ valuation. The company burns ~$80M annually while touting contracts worth hundreds of millions that haven’t generated meaningful revenue yet.

Actual Financial Performance (Not the Press Release Version)

Consolidated Results - Q2 2025 (Most Recent Quarter)

Source: ASPI 10-Q filed Aug 14, 2025

Full Year Results Comparison

Source: ASPI 10-K filed March 30, 2025; ASPI investor relations income statement

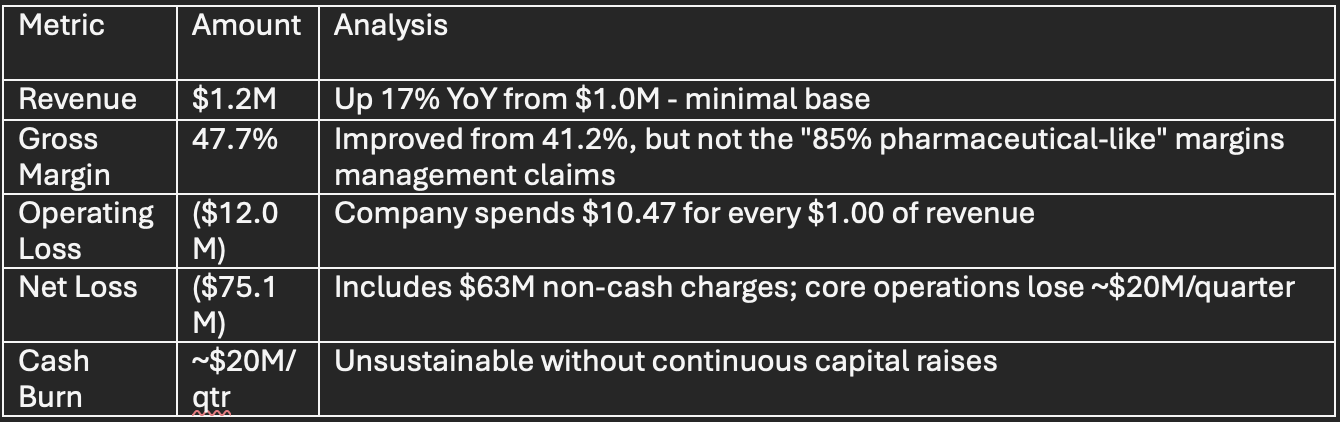

The 857% revenue “growth” sounds impressive until you realize it’s growing from an absurdly low base. More importantly, losses expanded faster than revenue.

Business-by-Business Reality Check

Since ASPI won’t provide this breakdown in audited financials, here’s what you can piece together from press releases and SEC filings:

1. PET Labs (Radiopharmaceuticals) - The Only Real Revenue

FY 2024 Revenue: ~$4.2M

Gross Margin: Likely 39-48% (consolidated company margin)

Status: Operational and stable

Reality: This IS the current business. Everything else is pre-revenue or minimal.

Source: ASPI Q2 2025 10-Q; management business updates

2. Molybdenum-100 - Zero Revenue Despite 3-Year-Old Contract

Contract Announced: November 2022 with BRICEM (Beijing Research Institute)

Projected Revenue: $2.5M to $27M per annum (25-year term)

Claimed Margin: ~85% “pharmaceutical-like”

Actual Revenue to Date: $0

Issue: Production delayed due to “feedstock supply complications”

Source: ASPI press release Nov 28, 2022; Q2 2025 business updates

Translation: Management announced a blockbuster contract three years ago. Still hasn’t shipped product. This should concern you.

3. Carbon-14 - Just Started Production (Finally)

Contract: Take-or-pay with RC-14 Inc. for minimum $2.4M annually

Claimed Margin: ~85%

Production Start: February 2025 (delayed from 2024 guidance)

H1 2025 Revenue: Minimal contribution, not separately disclosed

Reality: Too early to assess actual unit economics

Source: ASPI press release Feb 25, 2025; Q2 2025 10-Q

4. Silicon-28 - High Price, Low Volume, Uncertain Scaling

Pricing: $550,000 per kilogram (small research volumes)

Capacity: 50+ kg/year

Claimed Margin: ~75%

Current Status: Pre-revenue at commercial scale

Issue: $550K/kg pricing only works for research. Commercial pricing needs to be “significantly lower” per management.

Translation: The per-kg price sounds amazing, but it’s not a viable commercial model. Full capacity at current pricing = $27.5M revenue, but they’ve said that pricing doesn’t scale.

5. HALEU (Nuclear Fuel) - Pure Speculation

Projected Revenue: $375M potential (TerraPower contract)

Projected Margin: 40-63% depending on feedstock

Plant Cost: <$100M per facility

Target Timeline: 2027

Current Status: Zero revenue, licensing not obtained

Reality: Entire business is 2027-2030 projections, not demonstrated economics

Source: ASPI investor presentations; TerraPower agreement disclosures

6. Renergen Merger - Combining Two Loss-Making Companies

Renergen FY2025 Revenue: ~$700K (minimal)

ASPI Equity Raise for Deal: $210M (September 2025)

Pro Forma Combined Revenue: ~$7M (both companies early-stage)

Pro Forma Combined Loss: ~$48M annually

Management 2030 Target: >$300M EBITDA

Reality: Both companies currently unprofitable; 2030 target requires 43x revenue growth

Source: Renergen scheme circular June 2025; ASPI 8-K filings May-Aug 2025

The “Energy Cost Savings” Story: Management claims Renergen LNG can reduce isotope production energy costs by 94%. That’s material if true (energy = 90% of COGS), but it’s forward-looking integration economics, not current reality.

7. Quantum Leap Energy (Nuclear Waste) - 3-4 Years From Revenue

Upfront Cost: $3M ($150K cash + 266K shares)

Development Spend: $4.5M Mini Unit, $12.5M Midi/Maxi Unit

Revenue Model: 6% royalty on net revenues (15 years)

Timeline: 36 months to commercial validation

Reality: Development stage, no near-term revenue

Source: ASPI 8-K filed Oct 22, 2025; QLE acquisition press release

The Unit Economics Problem: What You Can’t Find

Data NOT Disclosed in SEC Filings:

Revenue by product (only two vague segments: “Specialist Isotopes” 95%, “Nuclear Fuels” 5%)

Production costs per kilogram by isotope type

Actual production volumes vs. nameplate capacity

Plant utilization rates

Product-specific gross margins

Contractual minimum volumes (vs. maximum potential)

Per-plant profitability

Where Unit Economics Data Appears:

Contract maximums: Press releases (not binding minimums)

Margin estimates: Investor presentations (not audited P&Ls)

Pricing: Management statements (often small-volume research pricing)

Production targets: Forward-looking guidance (not achieved results)

Cost Structure: The Real Numbers

Q2 2025 Operating Expenses Breakdown

Source: ASPI Q2 2025 10-Q

The Math: ASPI generated $1.2M in revenue and spent $12.5M in operating expenses. SG&A alone is 973% of revenue—corporate overhead, M&A costs, and business development for a company generating less revenue than a mid-sized dentist’s office.

This cost structure only works if revenue scales dramatically. If it doesn’t, dilution accelerates.

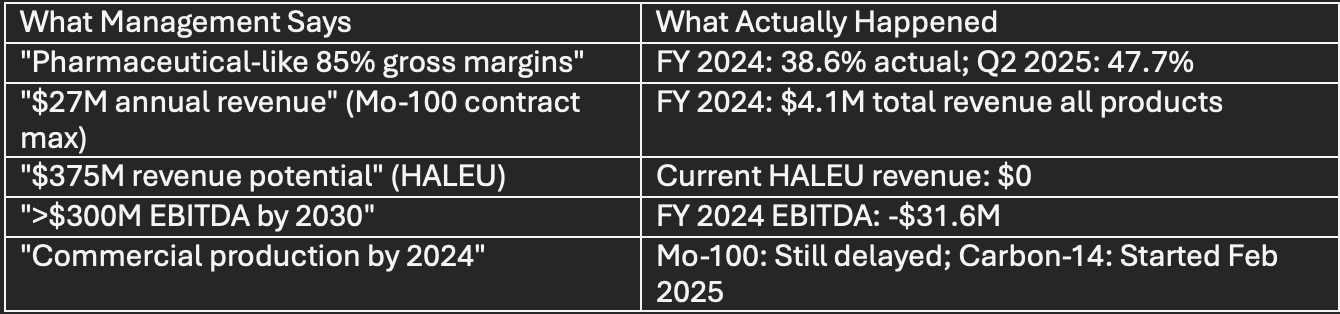

Management Guidance vs. Actual Results

Sources: ASPI press releases 2022-2025; ASPI 10-K FY 2024

Investment Thesis: What You’re Actually Buying

Bear Case (What the current data shows):

Three years post-Mo-100 contract, zero revenue due to execution issues

FY 2024 revenue of $4.1M almost entirely from acquired radiopharmacy, not proprietary tech

$80M annual cash burn requires continuous dilutive capital raises

Forward projections consistently miss (production delays, timeline slippage)

Trading at 234x revenue with no clear path to profitability in next 2 years

What You’re Buying: A development-stage advanced materials company with unproven commercial-scale unit economics, trading on 2027-2030 projections rather than demonstrated profitability. This is a high-risk speculation on technology commercialization, not an investment backed by transparent, audited business-line economics.

Where to Find the Limited Data Available

Since ASPI doesn’t provide granular unit economics in SEC filings, you’re stuck with:

SEC EDGAR (sec.gov): Search “ASP Isotopes” for 10-Q and 10-K—consolidated financials only

Company IR (ir.aspisotopes.com): Press releases with contract announcements and forward guidance

Earnings Transcripts: Quarterly calls via SeekingAlpha or earnings.io for management commentary

Third-Party Research: Ocean Wall Partners, Blue Gem Research (Google for PDFs)

Bottom Line: You were right to be frustrated. ASPI provides “rosy stories for future rockstar profits” in press releases while actual audited unit economics by business line don’t exist in public filings. The company is pre-commercial for its core isotope technology, burning significant cash, and dependent on successful execution of 2027-2030 projections that have consistently slipped.

HOW OUR FIRM SEES IT: The SEQH Capital Bull Case

We acknowledge the bear case above. The near-term unit economics are indeed anemic. But we believe the market is underpricing ASPI’s embedded optionality and transformational margin expansion potential. Here’s our analytical framework: