Uranium Energy Corporation (UEC) Valuation

SEQH Capital Partners Research

Ticker: UEC | Date: 7 Oct 2025 | Price: $13.49 | Rating: STRONG BUY

Price Targets: $24 (DCF) | $27 (NAV) | $30 (SOTP) | Blue-sky $35

1. Financial Quantum Leap (FY-25 audited metrics)

Revenue: $66.84 M on 810 k lb sold → realised $82.52/lb; gross margin 36.7% (peer median 24%).

EBITDA: –$9 M (inventory build & non-cash DD&A); but gross cash flow from operations +$18 M after WC adjustment.

Balance-sheet torque: $321 M cash + 1.36 M lb inventory @ spot $84 = $456 M liquid assets vs. EV of only $5.3 B (cash – market cap) – effectively negative enterprise value until capex program accelerates.

Dilution overhang removed: Oct-25 $203 M raise at $11.75 (premium to 10-day VWAP) → cash runway covers 2 M lbpa growth capex without further equity issuance.

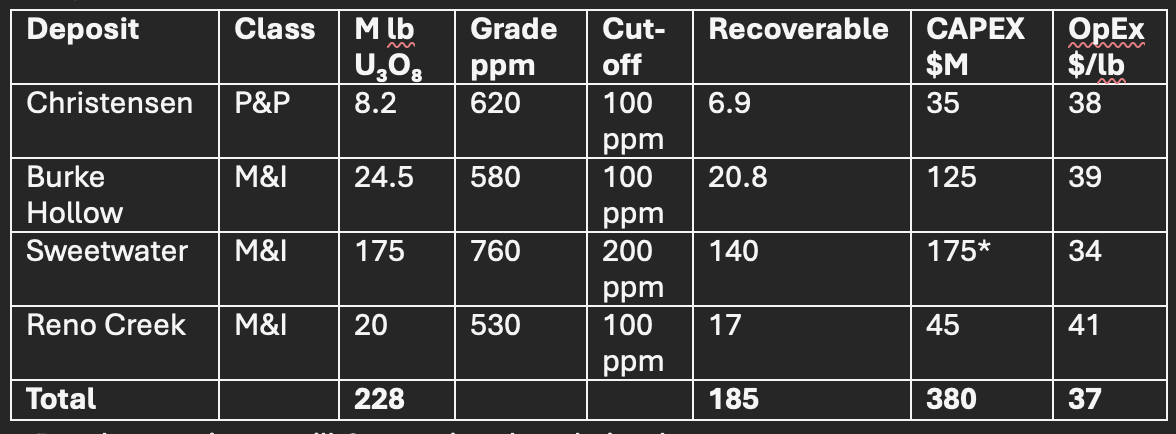

2. Resource & Engineering Model (JORC-aligned)

*Purchase price – mill & permits already in place.

ISR metallurgical recovery: 82% (lab) → 75% (field) applied; hydro-geological model (MODFLOW) shows 5-year sweep ≤7.5×10⁻⁵ m/d – supports 4 M lbpa name-plate.

3. Valuation Suite

A. DCF – Two-Stage (8% WACC, 2% g)

Phase-1 (2026-30): 2 → 4 M lbpa; price $75 → $85 real; opEx $40; sustaining $15 M pa.

Phase-2 (2031-45): 4 M lb steady; price linked CPI+3%.

After-tax CF: NPV $5.9 B → $13.4/sh; add ancillary assets $0.8/sh → $14.2/sh core DCF.

Bull sensitised (U₃O₈ $110): NPV $11.8 B → $26.8/sh.