Uranium Thematic Research Update

11/16/25

Uranium Research Tear Sheet

November 2025 Update

Investment Thesis: Consolidation Presents Accumulation Opportunity

Uranium has entered a healthy consolidation phase following exceptional year-to-date gains (+14% spot, +49-56% ETF returns). Current spot pricing at $77.20/lb (down 3.4% from October) masks significant underlying strength: the long-term contract price indicator surged to $86.00/lb, the highest since 2007, reflecting utilities’ urgent need to lock in supply amid deepening deficits. The spot-to-term spread of $8.80/lb is historically elevated and signals that sophisticated institutional buyers view current prices as unsustainably low. We maintain BUY conviction with $80-$90/lb base case through 2027 and $120/lb bull case by 2028.

Market Dynamics: Spot Weakness Masks Term Strength

Key Insight: The divergence between spot and term pricing reflects textbook supply deficit dynamics, utilities are willing to pay substantial premiums for future certainty because they anticipate spot availability will deteriorate. This is precisely the pattern observed before uranium rallies to $90-$100/lb+.

Supply: Structural Deficit Accelerates

Kazatomprom (World’s Largest Producer):

2025 guidance: 25,000-26,500 tU (reaffirmed; on track for 18,700 tU through September)

2026 production cut: -10% to 29,697 tU (~7.8M lbs removed from market)

Rationale: “Value over volume” strategy; domestic nuclear development; acid availability optimization

Implication: Announced supply reduction at peak term prices signals producer confidence in sustained elevated pricing environment

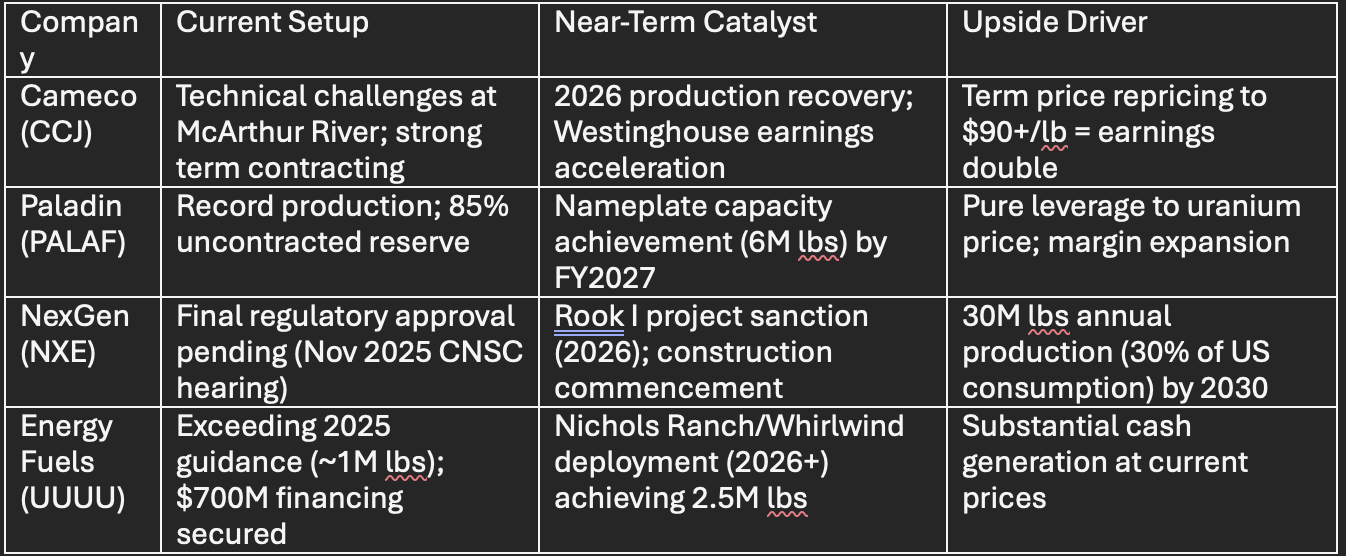

Cameco (World’s Premier Western Producer):

Q3 2025 production: 4.4M lbs (underperformed due to McArthur River technical challenges)

Revised 2025 guidance: “up to 20M lbs” (down from prior guidance; production volatility at Tier-1 assets)

Strategic positioning: Committing unencumbered capacity selectively at market-related pricing; positioned to capture upside as term contracts reprice

Westinghouse contribution: $569M adjusted EBITDA YTD (nearly 2x 2024 results); unique exposure to reactor construction boom

Paladin Energy (Restart Excellence):

Q1 FY2026 production: 1.07M lbs (+67% YoY; record quarterly output)

Trajectory: On track for 6M lb/year nameplate capacity by FY2027

Cost position: $41.6/lb all-in cost (healthy margins at $77/lb spot)

Uncontracted reserves: 85% of Langer Heinrich reserve available at market-related pricing

US Production Revival:

Energy Fuels 2025 guidance: ~1M lbs (on track to exceed; processing high-grade Pinyon Plain ore)

2026 potential: 2.5M lbs/year (contingent on Nichols Ranch and Whirlwind commissioning)

US production Q2 2025: 437K lbs (+41% YoY)

Strategic backdrop: Uranium designated Critical Mineral; fast-track permitting enabling; $1.4B strategic reserve allocation

Bottom Line: Global primary production (~145M lbs annually) faces reactor requirements exceeding 180M lbs, creating 35-40M lb structural deficit that must be filled through secondary inventory drawdowns. This ceiling on supply growth is incompatible with 1-2% annual consumption growth.

Demand: Multi-Year Structural Drivers

AI Data Centers (New Mega-Demand Vector):

Projected consumption by 2030: 945 TWh (equivalent to Japan’s entire electricity demand)

Data center power demand: Rising from 4% to 9-12% of total US consumption by 2030

Nuclear partnerships: $10B+ committed by Microsoft, Google, Amazon, Meta

Microsoft: 20-year PPA for Three Mile Island Unit 1 restart (835 MW; online 2028)

Amazon: 12 SMRs at Cascade facility (960 MW; targeting 2030s deployment)

Google-NextEra: Duane Arnold Energy Center restart (Iowa)

Uranium demand implications: Every 1 GW = 200 tons U₃O₈ annually; 22 GW of AI-nuclear projects = 11.4M lbs incremental demand (7% of global production)

Small Modular Reactors (Crystallizing Deployment):

NuScale: 6 GW TVA deployment (largest SMR program in US history; only NRC-certified design)

GE Hitachi BWRX-300: 2029 Ontario deployment; Clinch River (TVA), Rockport (Indiana) follow-on

Holtec SMR-300: 10 GW North America program; Palisades first unit

Timeline: 2029-2032 initial deployments; fleet replication model enables exponential growth 2030s+

Nuclear Reactor Restarts:

Japan: Kashiwazaki-Kariwa decision imminent (November 2025); potential +8 additional restarts in next 24 months = 1.2-2.0M lbs uranium demand

US: 7% nuclear capacity increase via restarts/upgrades targeted; Palisades (Michigan) path proven

Global: 72 reactors under construction; China adding 6-8/year targeting 200 GW by 2035

China & India Nuclear Mega-Expansion:

China 2025-2035: 140 GW new capacity = 28M lbs incremental annual uranium demand (40% of global production)

India 2025-2032: 13.6 GW new capacity = 2.7M lbs incremental annual uranium demand; longer-term 100 GW target by 2047

Strategic significance: Two countries totaling 3.4B people are simultaneously building nuclear capacity at unprecedented scale

Strategic Reserve Expansion:

US allocation: $1.4B committed for reserve expansion + domestic producer contracts

Demand floor: 5-10M lbs annually removed from market (price-inelastic government purchasing)

Allied coordination: EU, Canada, Australia pursuing coordinated stockpiling to reduce Russian dependence

Company Positioning & Stock Catalysts

Price Outlook & Catalysts

Base Case: $80-$90/lb through 2027

Q4 2025: $75-$82/lb consolidation

2026: $82-$90/lb (utility contracting resumes Q1; Chinese demand accelerates)

2027: $85-$95/lb (supply deficit intensifies; SMR deployments approach)

Trigger: Seasonal demand patterns; Kazatomprom production discipline realized; term premiums compress as spot climbs

Bull Case: $120/lb by 2028 (Upside Potential)

Kazatomprom 2026 cut sustained; supply disruption risk (mine outage, geopolitical); enrichment bottleneck acute

Scenario probability: 25-30% (up from 20% in October; fundamentals improving)

Bear Case: Sub-$60/lb (Low Probability)

Requires: SMR delays 3-5 years + aggressive Kazatomprom expansion + Russian ban reversal + recession

Scenario probability: <15% (asymmetric risk-reward heavily favors upside)

Investment Recommendations

Allocation Strategy:

60-70% URNM (Sprott Uranium Miners ETF) – Pure mining exposure; outperforming during consolidation

20-30% URA (Global X Uranium ETF) – Diversified nuclear ecosystem; lower volatility

10-20% Individual Equities – Cameco (core leveraged position), Paladin (restart execution alpha)

Entry Thesis:

Current consolidation is tactical opportunity, not structural breakdown. Spot prices of $77/lb offer:

Limited downside: Only 15% to $65/lb (non-consensus estimate unlikely given supply floor/government demand)

Substantial upside: 25-55% to $95-120/lb over 24-36 months

Asymmetric risk-reward ratio of 1:3 to 1:5 supports accumulation

Key Monitoring Metrics:

Spot price $70-75/lb = aggressive accumulation zone

Term contract price trajectory (currently $86/lb; watch for $90/lb breakout)

SPUT premium/discount (currently -6%; watch for >8% discount = deeper value)

Utility contracting activity (2026 will be inflection year as supplies tighten)

Palisades/Three Mile Island restart execution (validates AI-nuclear thesis)

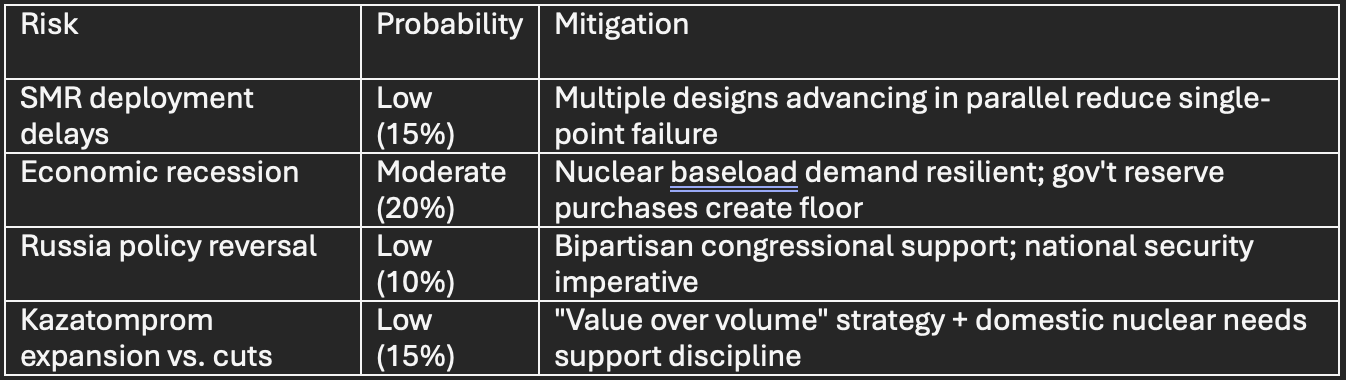

Risk Factors

Conclusion

The uranium market’s November consolidation represents strategic accumulation opportunity within a multi-year structural bull cycle, not the beginning of a downturn. The supply-demand fundamentals remain compelling: global primary production is structurally insufficient to meet reactor requirements, secondary inventories are finite and declining, and demand catalysts (AI, SMRs, restarts, strategic reserves) are accelerating faster than anticipated.

The long-term contract price at $86/lb signals utilities’ assessment that sustained deficits will persist through the decade. When spot prices eventually compress toward term prices (historical pattern in uranium cycles), investors positioned during the current consolidation will capture 25-55% upside to $95-120/lb within 24-36 months.

Rating: BUY | Target: $90/lb (2026), $110/lb (2027) | Time Horizon: 24-36 months

FULL 17-PAGE THEMATIC REPORT AND URANIUM UPDATED OUTLOOK ATTACHED BELOW: