Vistra Corp (VST) Earnings Recap and Outlook

11/6/25

VISTRA CORP (NYSE: VST)

Q3 2025 Earnings Summary | Research

SEQH Capital Research | November 6, 2025

Investment Snapshot

Vistra’s Q3 2025 earnings miss (EPS $1.75 vs. $3.50 consensus; Revenue $4.97B vs. $6.91B) represents a tactical opportunity, not a fundamental deterioration. The company stands at the nexus of America’s electricity demand inflection, driven by AI data centers, electrification, and industrial reshoring, with unmatched operational positioning: second-largest nuclear fleet (6.3 GW, 95% capacity factor), leading market share in high-growth ERCOT/PJM regions, and $10B deployable capital through 2027.

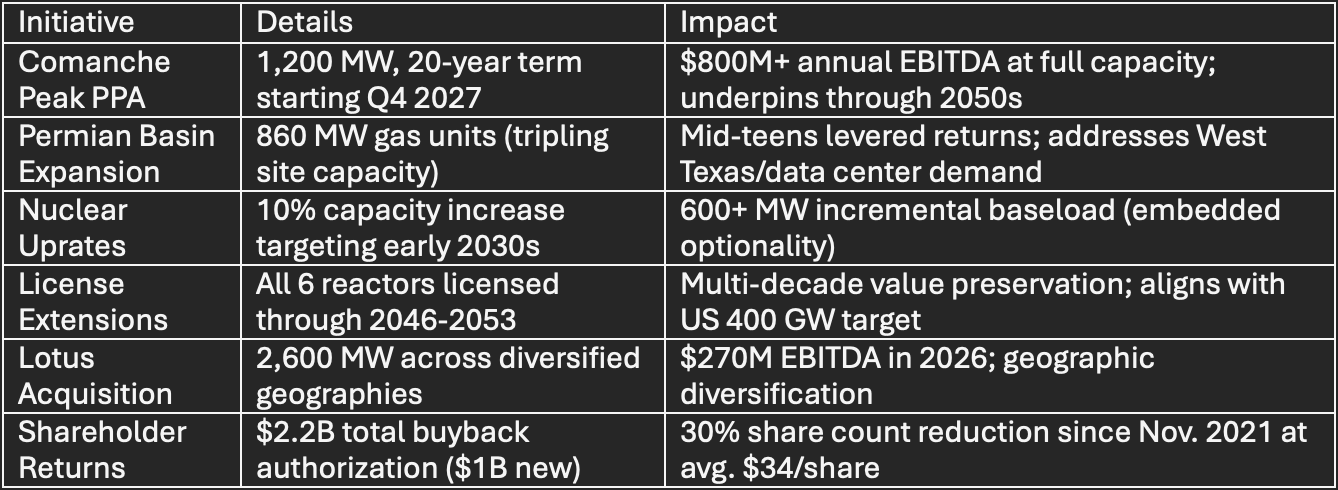

Core Investment Thesis: Management’s reaffirmed 2026 guidance projects +24% adj. EBITDA growth and +27% FCF expansion while maintaining 70% production hedges. At the midpoint, this implies ~$7.2B EBITDA and $4.33B FCF, metrics supported by: (1) Comanche Peak 20-year nuclear PPA commencing Q4 2027, (2) Permian Basin 860 MW gas expansion, (3) Lotus Infrastructure acquisition ($270M EBITDA contribution), and (4) unprecedented customer engagement for long-term power contracts with hyperscalers and data center operators.

Financial Performance & Forward Guidance

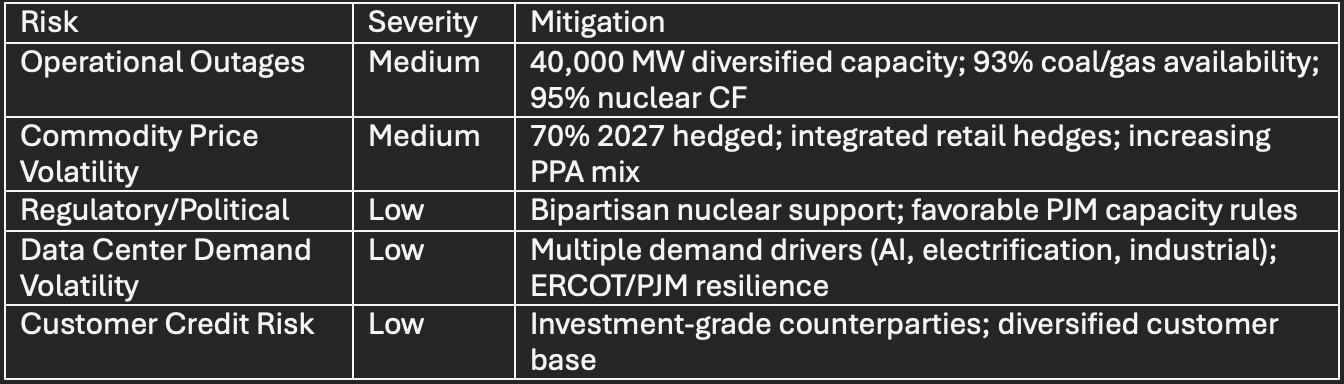

Q3 2025 Context: Revenue declined 10.1% YoY and adj. EBITDA fell 52.9%, primarily reflecting three transitory factors: (1) Martin Lake Unit 1 extended outage (~150 MW offline for 30 days), (2) seasonal retail supply cost dynamics, and (3) challenging prior-year comparables from favorable weather in Q3 2024. Generation EBITDA of $1.544B demonstrated resilience with realized prices $10/MWh higher than Q3 2024 due to disciplined hedging. Coal/gas commercial availability remained strong at 93% despite outages, with nuclear achieving industry-leading 95% capacity factor.

2026 Growth Drivers Quantified:

Lotus Infrastructure ($270M EBITDA, 2,600 MW capacity across PJM/NE/NY/CA)

Comanche Peak PPA ramp from Q4 2027 commencement

Permian Basin 860 MW capacity online early-to-mid 2028

Capacity market recovery (PJM auctions tracking toward price caps)

Structural Market Tailwinds

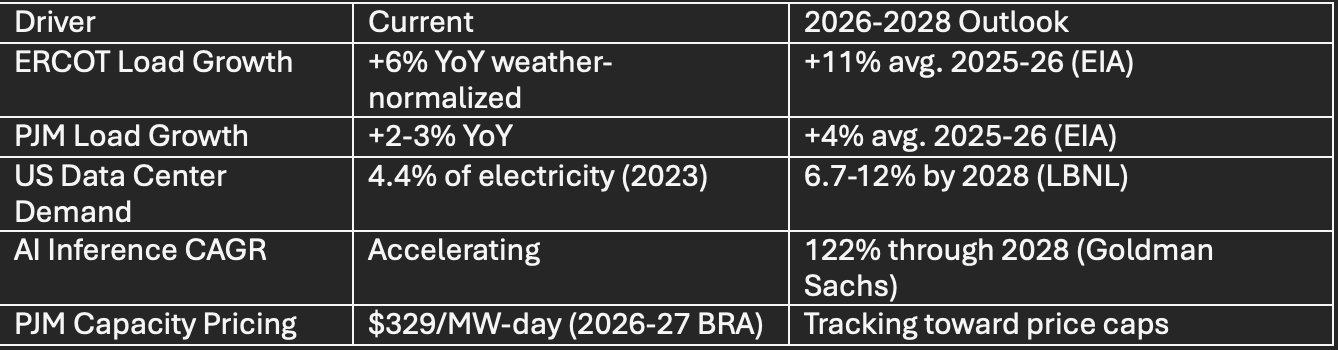

Electricity Demand Inflection

Why Vistra Benefits: The company captures outsized exposure to high-growth ISOs while nuclear baseload generates premium economics as customers prioritize 24/7 carbon-free power. Management disclosed data center market penetration at 8% with target of 20% by 2027, implying 2,000-3,000 MW of new customer demand and $400-600M incremental annual EBITDA. Current engagement levels represent “the highest in company history,” per management commentary.

Strategic Initiatives & Value Drivers

Investment Grade Pathway: Management targets IG ratings within 12-18 months via leverage declining to ~2.3x from current 2.6x. Achievement unlocks $200-400B+ investor base expansion and reduces borrowing costs by 100-150 bps.

Valuation & Price Targets

FCF Yield Analysis (Base Case)

2026 FCF Midpoint: $4.33B ($13.50-14.25/share on 348M diluted shares)

Current FCF Yield: 7.3-8.1% (vs. S&P 500 avg. 2.5%)

Normalized Utility/Infrastructure Yield (4.0%): Implies $356/share equity value

Current Valuation: Trading at 250-300 bps FCF yield premium (valuation expansion opportunity)

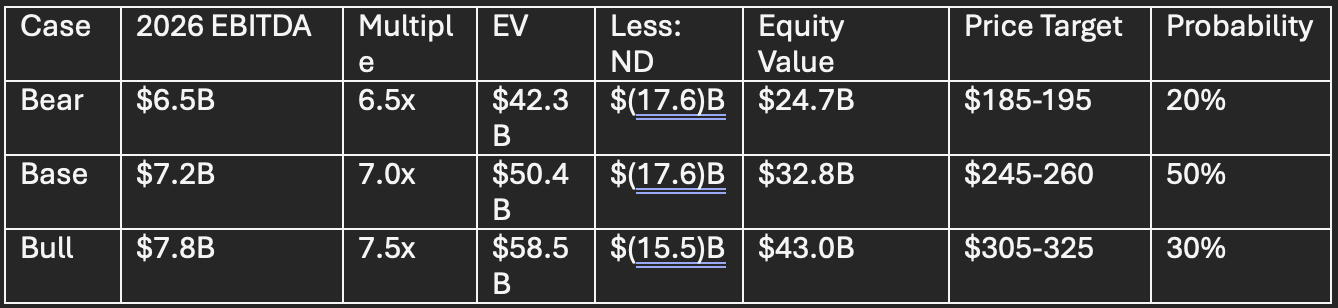

Scenario Analysis

Base Case Rationale: Conservative 7.0x EV/EBITDA (below 7.5x peer average) reflects risks offset by: (1) nuclear asset quality and operational excellence, (2) data center customer diversification and multi-decade contract visibility, (3) investment-grade rating pathway, and (4) 50% FCF per share growth trajectory through 2026.

Risk Summary & Mitigants

Downside Scenario: Even assuming 15-20% haircut to announced data center projects, ERCOT and PJM load growth remain robust at 8%+ annually, supporting $6.5-7.0B EBITDA floor by 2026.

Investment Decision Framework

For Growth/Infrastructure Investors:

Vistra represents the purest domestic play on the nuclear renaissance + AI data center energy inflection. Current prices following Q3 miss provide entry levels with embedded margin of safety. Multi-year earnings ramp (24% EBITDA growth to 2026) coupled with 7.3% FCF yield and $10B deployable capital creates asymmetric risk-reward.

For Value Investors:

The company’s 50% FCF per share growth trajectory through 2026, combined with disciplined capital allocation and buyback ROIC of 443% (avg. $34 repurchase price vs. $184.62 current), offers compelling risk-adjusted returns. Increasing PPA visibility and IG ratings target suggest downside protection.

One-Year Return Scenarios:

Bear case: $185-195 (-6% to +6%)

Base case: $245-260 (+33% to +41%)

Bull case: $305-325 (+65% to +76%)

Key Catalysts (12-Month Horizon)

Q4 2025 Earnings (Jan 2026): Validate full-year 2025 guidance convergence; early 2026 visibility

Q2 2026 Results: Lotus integration progress; updated 2026 guidance confidence

Q4 2026/Q1 2027: Potential investment-grade rating achievement; 2027 capacity market results

Ongoing: PPA announcements with hyperscalers/data center operators; Permian project confirmations

SEQH Capital Idea

RatingPrice TargetTimeframeRisk RatingBUY$245-26012 monthsMedium

Vistra stands at an inflection point where secular electricity demand growth intersects with unmatched operational positioning and management discipline. The Q3 miss provides a tactical entry point for investors with conviction in the nuclear renaissance and data center-driven energy transition. Management’s 2026 guidance (+24% EBITDA, +27% FCF) combined with 70% production hedges and $10B deployable capital through 2027 establishes a multi-year earnings ramp deserving of institutional accumulation. The company’s transformation from cyclical merchant generator to contracted infrastructure platform underwrites sustainable value creation through the decade.

Target Portfolio Allocation: 3-5% diversified energy/infrastructure; 5-8% focused nuclear/clean energy thematic fund.

Access Full Report: