Weekend Reading

12/14/25

Weekend Reading - Week of December 8–12, 2025

Macro: Fed Cut Three, Messaging Hawkish

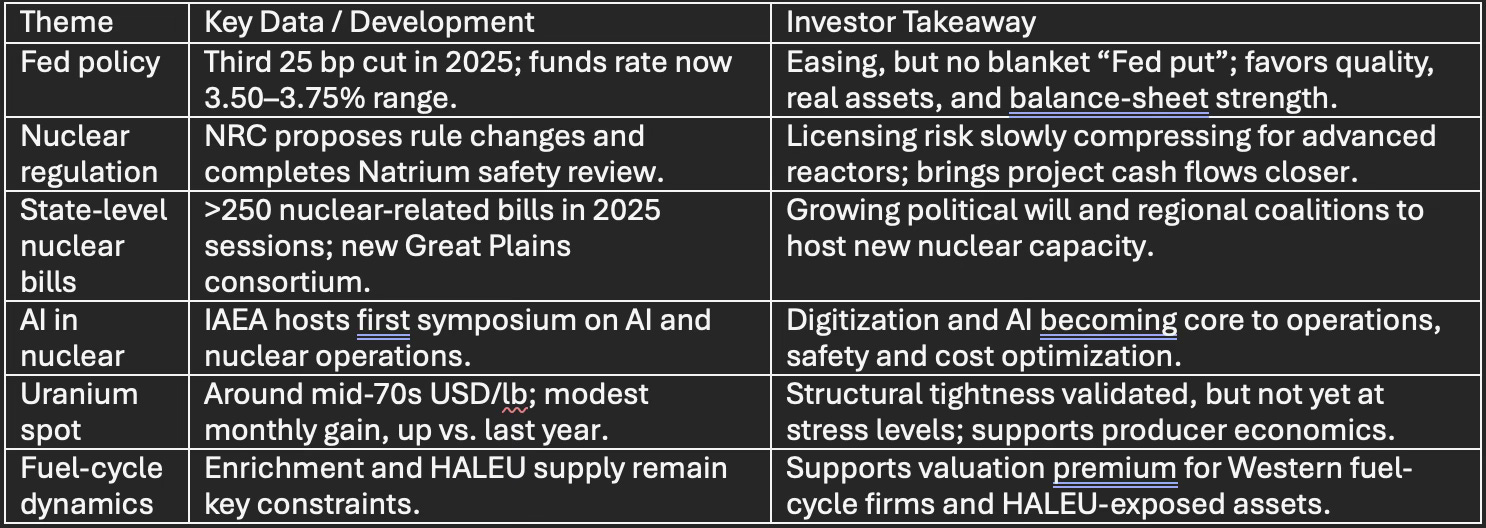

The Federal Reserve delivered its third consecutive 25 bp rate cut this year, taking the federal funds target range down to 3.50–3.75%. The statement characterized activity as expanding at a “moderate” pace amid slower job gains and a slightly higher unemployment rate, but Chair Powell explicitly pushed back on market hopes for a rapid, linear cutting cycle.

Markets are now debating whether this move marks the end of the “front-loaded” phase of the easing cycle, with Fed communication stressing data dependence and uncertainty around additional cuts in 2026. Rate futures still lean toward at least one further cut over the next 12 months, but the bar is rising, which keeps term premium and equity risk premia in play as key variables into year‑end.

For equity investors, the near-term read is incrementally supportive: policy is easing at the margin, financial conditions are no longer tightening, and the Fed is not trying to re‑ignite a “Powell put” regime. The nuance is that this is a mid‑cycle‑style adjustment with real yields still restrictive, which favors quality balance sheets, positive free cash flow and real‑asset exposure over the highest-duration, story‑only growth.

Nuclear Policy: Regulation, AI and State-Level Momentum

Policy momentum for nuclear continued to accelerate at both the federal and state levels, with a noticeable shift toward clearing regulatory underbrush and enabling advanced reactors. The U.S. Nuclear Regulatory Commission (NRC) proposed rule changes this month to sunset or modify obsolete regulations in response to a recent executive order, signaling an effort to streamline portions of the licensing framework for new technologies.

At the same time, NRC staff completed the final safety review for TerraPower’s Natrium small modular reactor in Kemmerer, Wyoming, putting the construction permit decision ahead of the original schedule and reinforcing that first‑of‑a‑kind projects are crossing from concept into executable assets. State legislatures are also active: over 250 nuclear‑related bills were introduced in the 2025 session, including measures on advanced reactors, spent fuel, and deployment incentives, with new initiatives such as the Great Plains New Nuclear Consortium in Nebraska and Oklahoma aimed at siting next‑generation capacity.

Internationally, the IAEA hosted its first dedicated symposium on AI and nuclear energy in early December, highlighting how analytics and automation are moving from the periphery to the core of plant operations, safety monitoring and fuel‑cycle optimization. For the SEQH nuclear complex, reactor OEMs, SMR developers, enrichment and isotopes, and nuclear‑levered utilities, this combination of regulatory streamlining, state‑level siting support and digitalization is steadily de‑risking timelines and expanding the addressable project pipeline.

Uranium & Fuel Cycle: Quiet Grind Higher

Uranium prices continued their slow grind higher, reinforcing the view that the market is in a structurally tight but not yet “panic” phase. Trading Economics data show uranium at roughly 77.90 USD/lb as of December 12, up about 0.45% on the day and modestly higher over the past month, with prices now roughly 1.7% above year‑ago levels. Alternative indicators and broker indices point to spot U3O8 oscillating in the mid‑70s per pound during early December, reflecting a relatively narrow trading band and stable utility buying.

On a longer lens, monthly IMF‑based data still show a step‑change versus the pre‑cycle phase: uranium spot averaged about 62.88 USD/lb in September, up more than 6% from August and materially above 2023 levels, even before the Q4 tightening that pushed prices into the 70s. The key is that these levels are increasingly “normal” rather than exceptional, which improves project economics across the curve, from established producers like Cameco to higher‑cost greenfield developers and physical vehicles, while still leaving room for upside if secondary supply and underfeeding prove insufficient.

For fuel‑cycle and enrichment names in the SEQH universe, the message is constructive: the commodity is no longer the bottleneck in isolation; conversion and enrichment remain the real constraints, especially for HALEU and Western‑aligned supply. That dynamic continues to support premium valuations for integrated players and specialized enrichers, and it increases the importance of contract optionality, jurisdictional risk management and proximity to U.S. and allied reactor build‑outs in underwriting individual equities.

Nuclear & Macro Snapshot Table

What to Watch Next Week

Into next week, markets will recalibrate around the Fed’s “cut but not capitulate” stance as new data print against a lower policy rate baseline. For macro, focus centers on inflation prints, labor indicators and any early sign that financial conditions are easing faster than the Fed is comfortable with, either via a renewed equity melt‑up or rapid declines in longer‑dated yields.

On the nuclear side, further NRC communication on rulemaking and any movement on key SMR licensing dockets, including TerraPower follow‑through, will be important for timeline risk across the reactor developer universe. Uranium investors should watch for incremental contracting updates from utilities and producers, as well as any evidence of restocking or supply disruption that could push spot out of the current mid‑70s equilibrium.