Weekly Global Macro Trends Analysis Report

11/8/25

Global Macro Trends Tear Sheet

Week of Nov 1–7, 2025 | Year-End Outlook

Executive Summary

First major market correction in months; Nasdaq -3.0%, S&P 500 -1.6% driven by tech/AI valuation reset and unprecedented U.S. government shutdown.

Federal Reserve cut rates to 3.75–4.00% in October, with December cut probabilities receding due to data blackout and persistent 3.0% inflation.

U.S.–China trade détente lowered tariff risk for the next year, but tech rivalry and geopolitical flashpoints, especially Ukraine, remain unresolved.

Macro & Market Analysis

Equity Markets

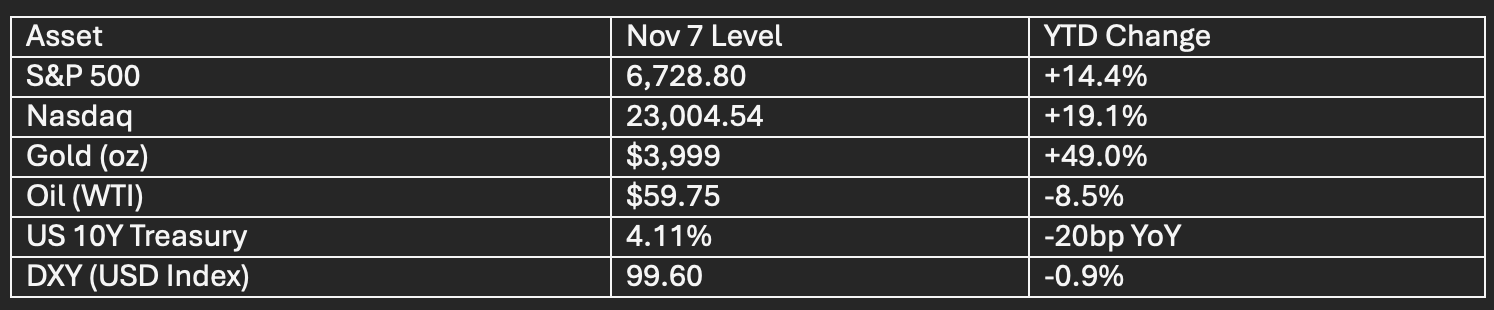

S&P 500: -1.6% WTD, +14.4% YTD

Nasdaq: -3.0% WTD, +19.1% YTD

Tech correction led by AI; Palantir at 700x Fwd PE, Nvidia above 50x PE.

Sector Trends

Rotation from growth (tech/AI) to defensives (financials, healthcare).

13.1% blended S&P 500 earnings growth, but cautious Q4 guidance (42 negative, 31 positive).

Fixed Income / Credit

Treasury yields: 2yr 3.55%, 10yr 4.11% (moderate steepening).

IG and HY credit stable, pockets of stress in lower grades.

Commodities

Oil: Weak, WTI $59.75/barrel, oversupply risks.

Gold: Strong, $3,999/oz, +49.0% YTD; supported by central bank buying, inflation hedge.

Copper/metals face China demand softening.

Currencies

DXY ~99.60, consolidating after H1 drop.

EUR/USD 1.14 range, supported by ECB stability.

Macro Fundamentals

Consumer spending resilient (NRF holiday forecast: $1.01T+).

Housing market turnover at 30-year low (28/1,000 homes), price growth slowing, mortgage rate 6.22%.

Geopolitical Risks & Scenarios

US–China Trade: Truce on rare earths and tariffs, 12-month window.

Ukraine: Attritional conflict continues. Energy assets, funding needs high.

Middle East: Israel–Lebanon, US–Iran tensions remain elevated; risk of oil spike.

Outlook:

Base Case (65%): Volatility persists, selective sector leadership (financials, healthcare, energy), government shutdown resolves before year-end; year-end S&P 500 target: 6,950.

Bull Case (20%): Rapid gov’t resolution, AI monetization, S&P 500 >7,150, broader rally.

Bear Case (15%): Extended shutdown, tech/AI bubble burst, S&P 500 <6,400, defensive outperformance.

Actionable Themes

Overweight: Financials (steeper curve), Healthcare (defensive), Energy (stable crude), Profitable Tech post-correction.

Neutral: Consumer Discretionary (holiday spending), Industrials, Communication Services.

Underweight: Real Estate (CRE & office), Utilities (yield risk), Unprofitable Tech (valuation reset).

Risk Highlights

Extended shutdown (high impact); AI/tech valuation compression; inflation resurgence; geopolitical flare-up.

Portfolio: Defensive allocation (cash, gold, treasuries) advised while tactical re-entry on resolution.

Data Snapshots

Full Report Access

Access the full 22-page SEQH Capital Research Macro Trends Report below: